Quick Overview

The core promise of the ICICI Pru Signature Assure Plan is “Get life cover, grow your wealth, and secure your family, all in one plan.” On paper, it sounds compelling. But here’s the real question most buyers don’t ask upfront: Does combining insurance and investment actually work in your favor?

In this guide, we break down how the plan works, what you really get, the costs involved, and whether it truly delivers on its promise.

What Is the ICICI Pru Signature Assure Plan?

The Signature Assure Plan is a long-term ULIP designed to help you build wealth while offering life cover. You pay premiums for a fixed period, a portion of which provides life cover so that the nominee receives the sum assured if the policyholder dies during the term. The remaining amount is invested in market-linked funds (equity/debt), with returns depending on market performance.

Key Plan Details

Important Benefits

1) The Smart Benefit is activated on the policyholder’s death:

- Future Secure Benefit: The insurer waives and funds all remaining premiums until the end of the premium payment term

- Family Income Benefit: The nominee receives an annual income of up to 10% of the sum assured on every policy anniversary till maturity.

2) Maturity Protect: If the policyholder survives to maturity and makes no partial withdrawals during the policy term, the insurer adds extra units, if needed. This is done to ensure that the maturity value does not fall below the annualized premium multiplied by the premium payment term.

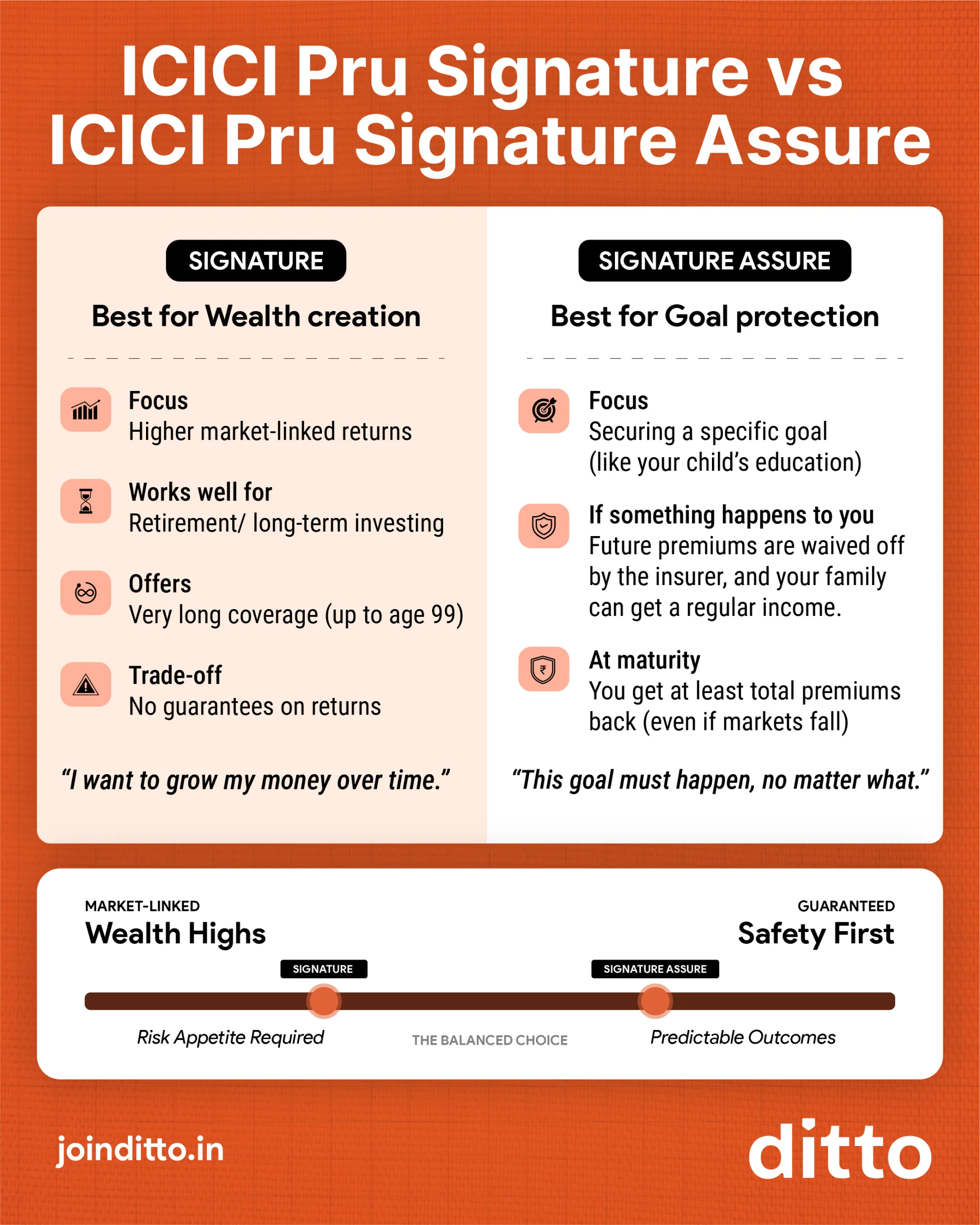

ICICI Pru Signature vs ICICI Pru Signature Assure

For more details, you can also check out our guide on ICICI Pru Signature.

Fund Options, Portfolio Strategies, & Wealth Boosters

ICICI Pru Signature Assure Plan gives you the flexibility to decide how much risk you want to take and how actively you want to manage your money.

Fund Options

You can invest in equity, debt, and balanced funds. The plan offers a large range of 20+ fund choices, including large-cap, mid-cap, small-cap, and sector-based options, so you can match your investment to your risk appetite. For more information, you can read pages 9-10 of the official Signature Assure policy brochure.

Portfolio Strategies

You can choose how your money is managed:

- Fixed Strategy: You decide where your money goes and in what proportion. You can also switch between funds freely.

- Lifecycle Strategy: This strategy automatically reduces equity exposure as you age and moves more money into debt funds.

- Trigger Strategy: Here, the plan shifts money between funds when the market moves by a set trigger point.

- Target Allocation Strategy: This keeps your chosen fund mix balanced by periodically rebalancing it.

Wealth Boosters

The plan also comes with features that are designed to support long-term wealth creation, but each comes with conditions you should be aware of:

Loyalty Additions

Extra units are added every 5 years, starting from the end of the 10th policy year. These are calculated as approximately 2.5% of your average fund value over recent quarters, so the actual benefit depends on how your investments have performed.

Top-Ups

You can invest additional funds at any time during the policy term (except the last 5 years). This helps if you want to increase your investment when markets are low, but each top-up also comes with a 5-year lock-in period.

SWP (Systematic Withdrawal Plan)

After the initial lock-in, you can withdraw a fixed amount or percentage regularly (monthly/quarterly/yearly). While this can provide a steady income, frequent withdrawals may reduce your final maturity value.

In short, these features add flexibility, but they don’t guarantee higher returns. Your actual gains still depend largely on market performance and how long you stay invested.

Charges, NAV, & Returns

Key Charges

- Policy Administration Charge: Around 0.525% of your annual premium, deducted monthly (capped at ₹500/month).

- Fund Management Charge (FMC): Charged for managing your investments, typically up to 1.35% per year, depending on the fund you choose.

- Mortality Charges: They are deducted monthly and depend on your age, sum assured, and risk profile. The older you get, the higher this charge tends to be.

- Discontinuance (Surrender) Charges: If you exit early (within the first 5 years), a penalty is charged. This can be a percentage of your premium or fund value, subject to caps.

Net Asset Value (NAV)

NAV is the value at which units in your ULIP fund are allocated or redeemed. In the ICICI Pru Signature Assure, NAV is declared daily on business days, and it can rise or fall depending on market performance. That means a higher or lower NAV does not guarantee anything on its own. What matters more is the fund’s objective, risk level, consistency, and the charges you pay over time.

Returns

Here’s an illustration from the policy brochure to help you understand what returns might look like for an annual premium of ₹1 lakh, a premium payment term of 10 years, and a policy term of 25.

Key Takeaway: The Insurance Regulatory and Development Authority of India (IRDAI) mandates that insurers present ULIP returns at 4% and 8%, but these are illustrations and not guaranteed returns. In reality, even though there’s no upfront premium allocation charge, ongoing costs like admin charges, FMC, and mortality charges quietly eat into your returns every year. That’s why ULIPs often deliver lower-than-expected returns, even when the market performs well.

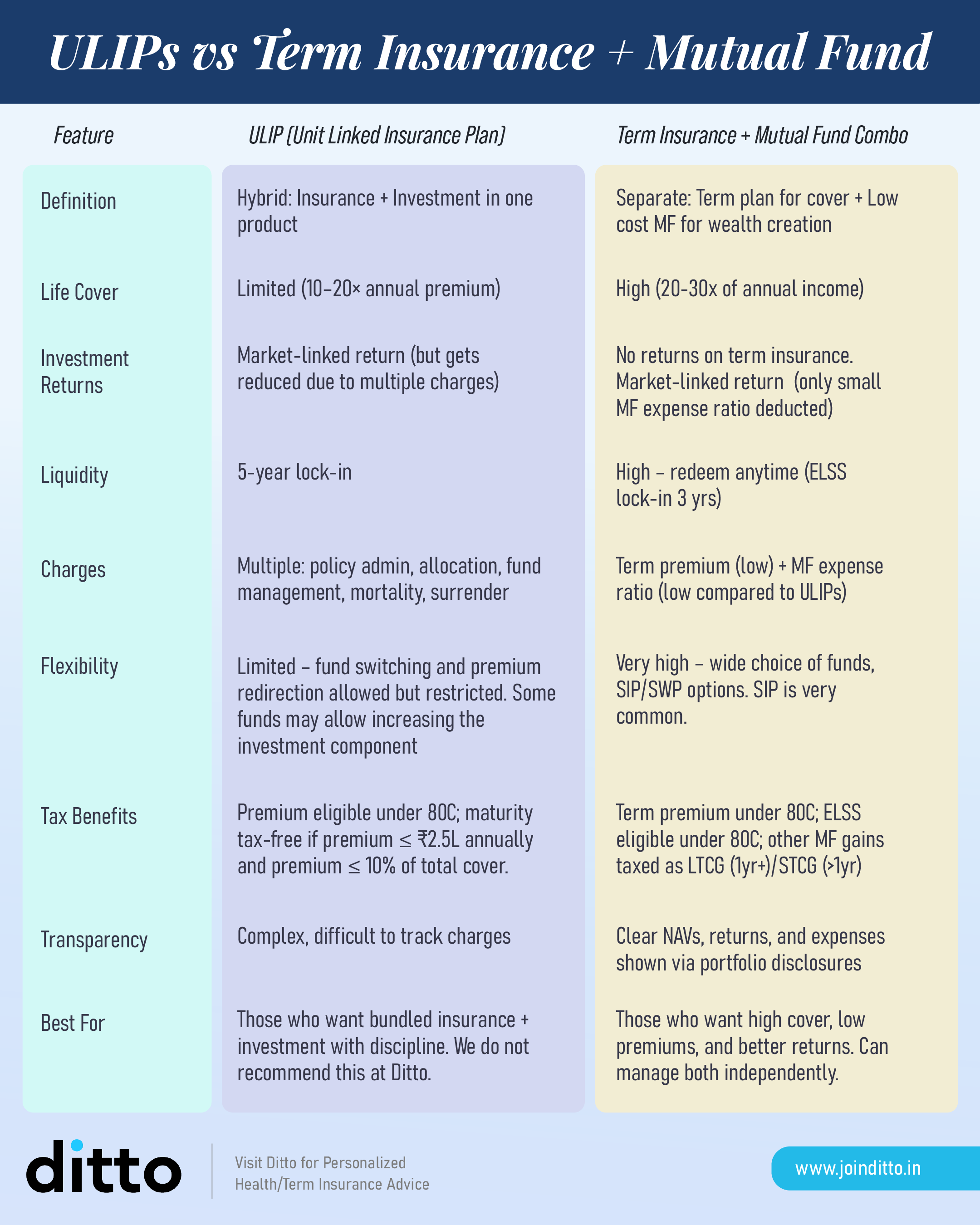

Pros, Cons & Should You Invest in ICICI Pru Signature Assure?

While this plan offers the dual benefit of insurance and investment, it may not be the most efficient option. For more details, you can refer to the infographic attached below:

Should You Choose the Signature Assure Plan?

You can choose Signature Assure if:

- You’re okay with market-linked returns.

- You want features like premium waiver and family income payouts.

- You don’t mind staying invested for longer terms (15-25 years).

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Ditto’s Take on ICICI Pru Signature Assure

If your primary goal is to secure your family's financial future, ULIPs like the ICICI Signature Assure Plan may not be the most efficient choice. For a premium of ₹1 lakh, the sum assured typically ranges between ₹7 lakh and ₹10 lakh.

On the other hand, a pure term insurance plan can offer significantly higher life cover at a much lower cost, ensuring your family is adequately protected. You can then invest separately in instruments that suit your financial goals, liquidity needs, and risk appetite.

If you prefer ICICI Prudential as your insurer, you may want to consider iProtect Smart Plus, which is designed purely for protection and offers much higher coverage for the same premium. Alternatively, you can explore our comprehensive guide to the best term insurance plans in India to find a policy that better aligns with your needs.

Frequently Asked Questions

ICICI Prudential Customer Reviews

Last updated on: