Home loan insurance, also known as a home loan protection plan, is a loan-linked insurance policy that helps repay the outstanding housing loan if the borrower dies or experiences a covered event such as permanent disability or a specified critical illness. The insurer settles the eligible loan balance directly with the lender.

Coverage can be structured as reducing cover term, level cover, or hybrid cover, depending on the policy design. These plans should not be confused with home insurance, which protects the physical structure against risks such as fire, theft, or natural disasters.

However, an individual pure term plan offers better value, as most home loan insurance policies in India are group plans. This guide is perfect for those who wish to explore how home loan insurance works in India.

As per the National Housing Bank’s latest monthly credit-flow data, the outstanding amount for individual housing loans reached over ₹39 lakh crore as of 30 April 2026. With home loan balances running into lakhs and crores for most families, one unexpected event can leave loved ones struggling with EMIs. This is exactly where home loan insurance comes in to protect your family from inheriting your outstanding debt if you pass away during the loan tenure.

This guide breaks down how home loan insurance works, its costs, benefits, and whether a term insurance plan may be a smarter alternative for your family.

Unsure about whether to purchase a term plan or home loan insurance? Book a free call or chat on WhatsApp with a Ditto advisor, and let us help you out.

How Home Loan Insurance Works

You take a home loan from a bank, housing finance company, life insurance company or Non-Banking Financial Company (NBFC).

The lender may offer a home loan insurance plan alongside the loan.

If the borrower passes away during the loan tenure, the insurer pays the eligible outstanding loan amount directly to the lender.

The loan gets settled without placing the repayment burden on surviving family members.

As a result, the family can continue owning the property without worrying about future EMIs or the risk of losing the home.

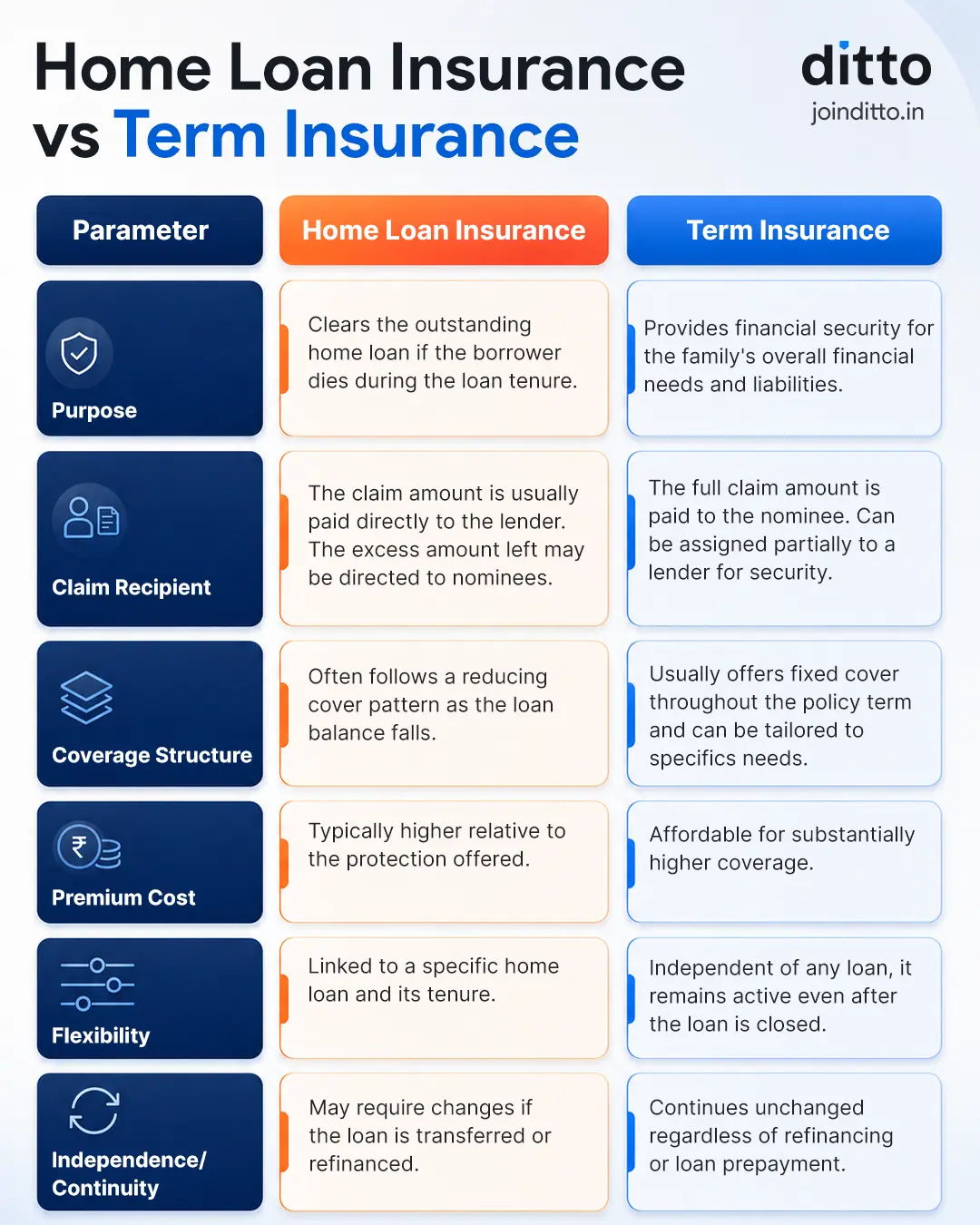

Home Loan Insurance vs Term Insurance

While home loan insurance is designed specifically to repay the outstanding home loan if the borrower dies, term insurance offers much broader protection and protects your family against any outstanding debts. Before choosing either route, it is important to understand where each one fits into your financial plan.

See the infographic below for a side-by-side comparison of Home Loan Insurance and Term Insurance.

CTA

Premium Calculation and Sample Costs

Scenario: Rohit, age 35, takes a ₹50 lakh home loan with a 20-year tenure and wants to protect his family from the risk of loan repayment.

Reducing Cover: Under a sample ICICI Pru Group Term Plus rate, the life cover stays fixed at ₹50 lakh throughout the policy term, and the total cost can be around ₹2.24 lakh over 20 years.

Claim Example: The cover does not remain ₹50 lakh throughout the policy term. Instead, it broadly reduces in line with the outstanding loan. If Rohit passes away in the 10th year, when the outstanding loan is around ₹37 lakh, the policy settles the remaining loan amount.

Note: If the cover is issued as a group lender-borrower home loan insurance policy through the insurer, bank, or NBFC, Goods and Services Tax (GST) will be charged separately at the applicable rate and could increase the overall cost of the policy. Always check whether GST is included in the quoted premium before purchasing. For further details on GST, explore our guide on zero GST on health & term insurance.

Types and What They Cover

01

Reducing Cover

The sum assured decreases gradually as the outstanding home loan balance reduces. This is the most common structure in home loan insurance and is designed to closely match the remaining loan liability.

02

Level Cover

The sum assured remains unchanged throughout the policy term, regardless of how much of the loan has been repaid. Any surplus claim amount after the loan settlement can benefit the nominee.

03

Hybrid Cover

The sum assured remains fixed for an initial period, then starts to reduce later in the policy term. It combines elements of both level cover and reducing cover structures.

Take Note: Loan protection insurance does not cover every situation. Common exclusions include suicide within the initial waiting period, fraud or material non-disclosure of health or personal details, and loan defaults without a covered insured event. Always review the policy wording carefully before relying on the cover.

Is Home Loan Insurance Worth Buying?

Home loan insurance may be worth considering only when a personal term plan is not readily available due to age, occupation, medical history, or underwriting restrictions. In such cases, group term plans and credit life insurance covers can sometimes be more accommodating from an underwriting perspective.

Choose it if you want a simple, loan-linked protection solution without having to calculate separate term insurance requirements.

Consider it when the premium is competitively priced and offers reasonable value.

Prefer it if the premium is paid separately rather than being added to the loan amount.

A term insurance is recommended because it protects more than just the home loan. The payout can help the family repay outstanding debts, replace lost income, fund children's education, and meet daily expenses. It also offers higher coverage at affordable prices, greater flexibility, and often better value for money.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 24,000+ happy customers

For most borrowers, a term insurance plan remains the most practical and cost-effective way to protect a home loan. A well-designed term plan can provide substantially higher coverage, greater flexibility, and protection that extends beyond a single loan. Many of the best term insurance plans, like HDFC Click 2 Protect Supreme Plus, also offer life-stage benefits, allowing you to increase your cover when major financial responsibilities, such as a home loan, arise.

If the lender requires protection against loan default due to death, you can often assign your term policy to the bank for the outstanding loan amount. Our takeaway is simple. Use term insurance as your primary protection tool and consider home loan insurance mainly when underwriting challenges, medical conditions, age, or occupation make individual term cover difficult to obtain.

Frequently Asked Questions

What is home loan insurance, and how does it work?

Home loan insurance, also called a Home Loan Protection Plan (HLPP), is a policy designed to repay the outstanding home loan if the borrower dies during the loan tenure. Instead of the family taking over the EMI burden, the insurer settles the eligible loan amount directly with the lender. This helps ensure that dependents can continue owning the property without financial stress. Since home loans in India are generally capped at 30 years, most insurance for home loan plans also stops at 30 years. In contrast, personal term plans can extend much longer, offering protection beyond the loan tenure and even into retirement if needed.

Is home loan insurance mandatory in India?

No. Home loan insurance policy is completely optional in India. Banks and housing finance companies may recommend it during the loan process, but they cannot legally require borrowers to purchase it or make loan approval contingent on purchasing a specific insurance policy. RBI guidelines discourage restrictive selling practices and support customer choice. Borrowers are free to compare plans from different insurers or even rely on an existing term insurance policy for loan protection. Before agreeing to any bundled cover, always ask whether it is mandatory, how much it costs, and whether better alternatives exist.

Should I buy home loan insurance or choose term insurance for home loan protection?

Protecting a home loan with life cover is highly recommended, but the method you choose can significantly affect the cost, flexibility, and financial outcome for your family. Home loan insurance is linked to a specific loan and primarily protects the lender by clearing the outstanding balance. In contrast, term insurance for home loan offers broader protection. It typically provides a much higher cover amount at a lower premium and allows your family to use the claim proceeds as needed, including loan repayment. For most borrowers, a term plan delivers better value, greater flexibility, and stronger long-term financial security than a bank-linked home loan protection plan.

What is the difference between home loan insurance and home insurance?

Home loan insurance and home insurance serve completely different purposes. Home loan insurance protects the loan by repaying the lender if the borrower dies during the policy term. Home insurance protects the physical property against risks such as fire, theft, floods, storms, earthquakes, and other covered damages. One safeguards the loan liability, while the other safeguards the property itself. Many homeowners mistakenly assume they are the same product. In reality, a home loan insurance policy will not cover structural damage to your property, and a home insurance policy will not repay your outstanding housing loan.

Can I assign my term insurance policy to a bank instead of buying separate loan protection insurance?

Yes. If your lender wants protection against loan default arising from the borrower's death, you can often assign your existing term insurance policy to the bank. It is important to understand the difference between nomination and assignment. Nomination specifies who should receive the policy proceeds after death, while assignment transfers policy rights, in whole or in part, to another party, such as a lender. In practice, if a term policy is assigned to a bank for a home loan, the lender may receive the outstanding loan amount first. Any remaining claim amount is typically paid to the nominee or legal beneficiary, subject to the assignment terms and policy conditions.

Can I assign my term insurance policy to cover my home loan?

Yes. A term insurance policy can be assigned to a lender as collateral security for a home loan. Under this arrangement, the lender receives the portion of the claim required to settle the outstanding loan balance, while the remaining amount goes to the nominee. This approach allows borrowers to avoid purchasing a separate home loan insurance plan while still providing protection to the bank. The assignment can be removed once the loan is repaid. For many borrowers, this creates a practical balance between adequate family protection and lender security without duplicating insurance coverage.

When should I actually buy home loan insurance instead of a term plan?

Home loan insurance may be worth considering when obtaining adequate term insurance is difficult due to age, health conditions, occupation-related risks, or underwriting restrictions. Group credit life policies often have more flexible underwriting requirements and may provide access to protection that would otherwise be unavailable. It can also suit borrowers who prefer a simple loan-linked solution without separately calculating insurance requirements. However, for most salaried and healthy borrowers who can qualify for a standard term plan, standalone term insurance typically provides higher coverage, greater flexibility, and better overall value than a dedicated home loan protection plan.

What is property insurance for a home loan, and is it the same as HLPP?

No. Property insurance for home loan and Home Loan Protection Plans (HLPPs) are entirely different products. Property insurance protects the physical structure of the house against risks such as fire, floods, storms, theft, and natural disasters. An HLPP protects the lender by repaying the outstanding loan if the borrower dies during the loan tenure. One covers damage to the asset, while the other covers the financing attached to the asset. Some lenders strongly recommend property insurance because it protects their collateral, but it should never be confused with home loan insurance, which focuses on loan repayment risk.

Is financing home loan insurance through the loan a good idea?

Not always. Many lenders offer a single-premium home loan insurance policy and add the cost to the loan amount for convenience. However, this means you also pay home loan interest on the insurance premium for the entire tenure. For example, if a ₹2 lakh insurance premium is financed into a 20-year home loan at 9%, the EMI increases by roughly ₹1,799 per month, and the total repayment on that premium alone can exceed ₹4.3 lakh. While premiums may qualify for tax deductions under applicable tax provisions and claim payouts are tax-free, borrowers should compare the overall cost with that of a standalone term insurance plan before deciding.

How should life insurance work for a joint home loan?

For a joint home loan, insurance should reflect the actual loan liability and each borrower's financial contribution. If both spouses earn and both are responsible for EMI payments, relying on life cover for only one borrower may create a gap. If the uninsured co-borrower passes away, the surviving borrower may still struggle to manage the remaining loan and household expenses. When using a personal term insurance approach, each earning borrower should ideally maintain coverage sufficient to repay their share of the outstanding loan, while also providing income replacement and financial security for the family. This creates a more balanced and comprehensive protection strategy.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.