Quick Overview

What happens to your loan if something happens to you tomorrow? For many families, the real risk is not just loss of income, but the burden of an unpaid loan. That is where credit life insurance steps in. It is a simple solution designed to clear your outstanding loan, so your family does not have to carry that financial stress.

This guide explains how credit life insurance works, who it suits, and whether it is the right choice compared to a regular term insurance plan.

What Is Credit Life Insurance?

Credit life insurance is a type of life cover where the insurer settles the dues directly with the lender, whether a bank or Non-Banking Financial Company (NBFC), up to the outstanding amount. If there is any excess, it is paid to the nominee.

In India, this service is usually offered as a Group Credit Life policy. The lender holds the master policy, and each borrower is added as a member under it. Credit life insurance is completely voluntary. Lenders cannot legally make it a mandatory condition for approving your loan.

Products like the HDFC Life Group Credit Protect Plus insurance plan offer life cover for multiple loan types along with flexible tenures and premiums.

Note: The Key Facts Statement (KFS) is required by the Reserve Bank of India (RBI), especially when a bank or NBFC collects the premium along with the loan. In such cases, the insurance cost should be clearly disclosed in the KFS, included in the Annual Percentage Rate (APR) where applicable, and cannot be added later without the borrower’s explicit consent.

How Does Credit Life Insurance Work?

Group Policy Setup

The lender takes a master group credit life policy from an insurer. When you take a loan, you are added as a member and receive a certificate of insurance. The lender is the primary beneficiary of the outstanding loan amount, while your nominee receives any excess amount.

Cover Structure at Inception

Your cover starts equal to the loan amount and reduces over time in line with your repayment schedule. It is designed to mirror your outstanding loan balance throughout the tenure.

What Triggers a Claim

A claim is triggered if the borrower passes away during the policy term. Some plans may include accidental death or optional riders like critical illness or disability, depending on what is offered.

Who Sets the Features

The lender decides the features, add-ons, and structure of the policy. You can only choose from the options they make available, which is why such offers differ across banks.

Premium Payment

Most plans like HDFC Life Group Credit offer single premium options, which are collected upfront and often added to your loan. This means you may end up paying interest on the premium over time. Some lenders offer limited pay options, which can be more efficient.

On a Valid Claim

The insurer pays the outstanding loan directly to the lender. If there is any surplus due to prepayment or lower balance, it is passed on to your nominee.

Take Note: Credit life insurance varies by cover structure and loan type. Most plans like LIC Digi Credit Life use reducing cover aligned to the loan, while some offer level or flexible cover during moratoriums. It is widely used across home, vehicle, and personal loans, with tenure and structure tailored to the specific loan.

Who is Credit Life Insurance Suited For?

Benefits and Limitations of Credit Life Insurance

Benefits of Credit Life Insurance

- Clears a Specific Loan: If you pass away, that exact loan gets closed without delay. Your family does not have to take a call on how to use insurance money or deal with lender pressure during an already difficult time.

- Cover Tracks the Loan Balance: The cover reduces in line with your loan, so it always matches what is actually owed. You are not over-insured for a liability that reduces every month, which makes the structure simple and aligned.

- Useful in Select Situations: It can help if your only concern is loan protection or if you cannot easily get a regular term plan due to medical or underwriting constraints. In such cases, it ensures that the debt does not become a burden.

Note: As per IRDAI rules, the coverage term at inception cannot exceed the outstanding loan tenure. For credit-linked insurance, the policy term is aligned with the loan duration, which can typically extend up to 30 to 40 years.

Limitations of Credit Life Insurance

- Payout Goes to the Lender: The biggest trade-off is the lack of flexibility. The insurer pays the bank first, so your family cannot decide how to use the money for other priorities like living expenses or future goals.

- Cover Reduces Over Time: As your loan comes down, so does the insurance cover. Over time, the policy becomes less meaningful since it is only designed to clear a shrinking liability.

- May Duplicate Existing Cover: If you already have a well-sized term plan, this can be redundant. Your existing cover can easily take care of the loan.

- Often Sold at the Wrong Moment: It is usually offered when you are taking a loan, which is not the best time to evaluate insurance decisions. Many borrowers accept it without comparing costs or considering better alternatives.

Did You Know?

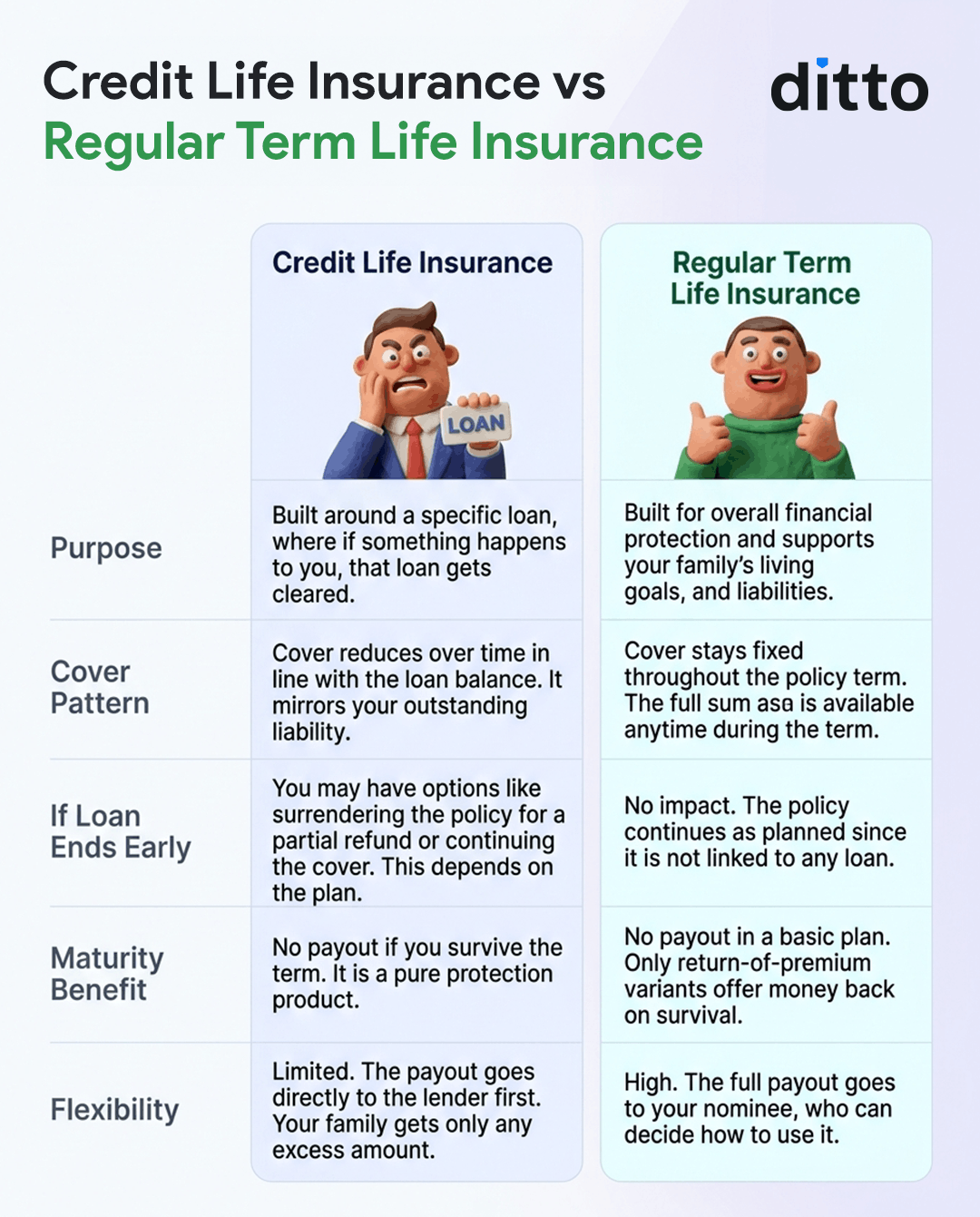

Credit Life Insurance vs. Term Life Insurance

Credit life insurance and term life insurance serve different purposes. For instance, if you are evaluating term insurance for a home loan, a regular term plan often offers more flexibility and broader protection than credit life insurance.

Take a quick look at the infographic for a better understanding.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Conclusion

Credit life insurance is a focused solution, but is limited in scope. Lenders often promote single premium policies that get added to your loan, so you end up paying interest on the premium. It is worth comparing this with a term insurance plan, as term plans provide a higher life cover at a lower premium.

If you are evaluating your options, review our guide on the best term insurance plans. It is important to build a strong term base first, then consider credit life only if you want additional loan-specific protection.

Frequently Asked Questions

Last updated on: