Home insurance protects your home structure and its belongings against unexpected losses like fires, natural disasters, and theft. Policies can cover the building structure, household contents, or both. Established insurers like HDFC ERGO and ICICI Lombard offer comprehensive home insurance. Key benefits may include repair or reconstruction costs, replacement of damaged belongings, temporary accommodation expenses, and personal liability protection.

Common exclusions include normal wear and tear, intentional damage, prolonged vacancy, mechanical breakdowns, and undeclared valuables. Claims are typically settled based on reinstatement value, agreed value, or indemnity value, depending on policy terms. This guide is ideal for people exploring home insurance in India.

As per Moneycontrol, more than 3.6 lakh houses were reportedly damaged across India in 2024–25 due to natural disasters. When a single flood or storm can erase years of savings, home insurance helps protect not just your property, but the financial security built around it.

In the next few minutes, this guide will walk you through home insurance in India, its coverages, the difference between home and home loan insurance, and how to purchase the right policy.

Confused about which insurance to purchase first, home, health, or term? Book a free call or chat on WhatsApp with a Ditto advisor, and let us help you out.

What Is Home Insurance?

Home insurance is a general insurance policy that helps you safeguard years of savings by reducing the financial burden of repairing, rebuilding, or replacing valuable assets after an unexpected event.

Note: In case you live in a gated society, your society insurance often covers only the building’s common structure. Your flat’s interiors, valuables, and alternate accommodation may remain uninsured. Always review the society policy before assuming you are fully protected.

Popular Home Insurance Policies

ICICI Lombard Complete Home Protect Policy: The policy offers an automatic 10% annual increase in sum insured, alternate accommodation, and loss-of-rent cover. Complete Home Protect policy offers policy tenure options of up to 5 years for uninterrupted protection.

HDFC ERGO Home Shield Insurance: Choose from benefits such as loss of rent, hotel stay, emergency purchases, and relocation expenses. Home Shield Insurance lets you insure the building, contents, or both, with coverage available for up to 5 years on an all-risk basis.

SBI General Griha Raksha Plus: The plan includes a dedicated home contents cover and an automatic annual increase in the sum insured to help keep pace with rising replacement and reconstruction costs. SBI General Griha Raksha Plus offers a policy tenure of up to 20 years.

Did You Know?

Under IRDAI’s standard Bharat Griha Raksha policy, if you opt for both home building and contents cover together, the policy automatically protects your general household contents at 20% of the building sum insured. This feature is capped at ₹10 lakh and doesn't require you to list each item.

CTA

What Does Home Insurance Cover in India?

Home Building: Protects the physical structure of the house, including walls, roof, flooring, permanent fixtures, garages, water tanks, and solar panels.

Home Contents: Covers household belongings such as furniture, appliances, electronics, clothing, and other personal items against covered risks.

Valuable Contents: Protects high-value possessions such as jewelry, paintings, silverware, and collectibles, which are usually subject to separate declaration and valuation.

Natural Calamity: Provides coverage against events such as floods, lightning, and other insured natural disasters. Global insured losses are projected to reach nearly USD 145 billion (₹13.78 lakh crore) in 2025, highlighting the growing financial impact of natural disasters and the importance of adequate home insurance coverage.

Take Note: Home insurance does not cover war, nuclear risks, intentional damage, normal wear and tear, or gradual deterioration. Claims arising from negligence, pre-existing structural defects, or undeclared valuables may also be rejected. It’s worth noting that home insurance protects the structure, not the value of the land it stands on.

Modern Home Insurance Add-Ons

Appliance & Electrical Breakdown Cover: Protects household appliances and electrical equipment against accidental breakdowns.

Domestic Worker Liability Cover: Offers protection if a domestic worker suffers an injury at your home and you become legally liable.

Keys & Locks Replacement Cover: Pays to replace lost keys or change locks after theft or loss.

Wallet & ATM Robbery Cover: Covers financial loss arising from wallet theft or ATM-related robbery incidents.

Pet Cover: Some insurers offer benefits for the accidental death of a pet dog, subject to policy terms and conditions.

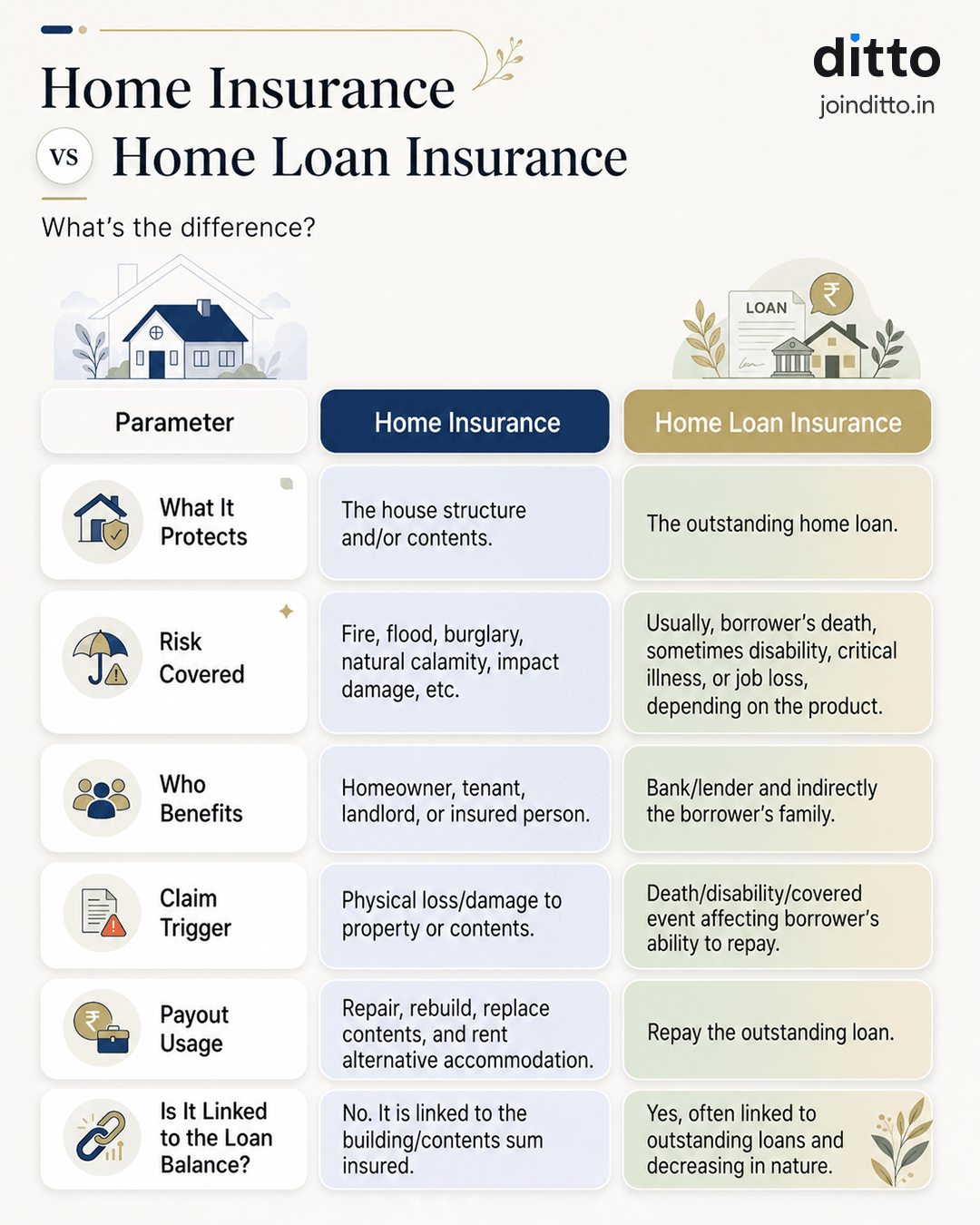

Home Insurance vs Home Loan Insurance: What's the Difference?

Many homeowners confuse home insurance with home loan insurance, but they serve very different purposes. Home insurance protects the house and its contents against risks like fire or theft.

Home loan insurance protects the lender by helping repay the outstanding loan if the borrower dies during the loan tenure.

Take a look at the infographic for a better understanding.

Note: At Ditto, we recommend considering a term insurance for home loan liability. Term insurance offers a higher sum assured at a significantly lower cost than a dedicated home loan protection plan. Another advantage is that the life cover typically remains constant throughout the policy term, whereas home loan insurance often comes with a reducing cover that declines as the loan balance falls. Even after the loan is repaid, the remaining term cover can continue to protect your family's future financial goals and income needs.

How Much Does Home Insurance Cost?

There is no standard premium for home insurance. The cost varies based on factors such as the sum insured, property location, construction type, age, and the house's condition. Your premiums also depend on selected add-ons, policy tenure, and the insurer’s pricing model.

Let’s take the example of home insurance for home-building cover, with a premium rate of ₹0.243 per ₹1000 of the sum insured.

Sample Premiums

Home Description

Sum Insured

Premium

A flat of carpet area 50 sq.m (concrete structure)

₹10,00,000

₹243

Bungalow of area 200 sq.m

₹60,00,000

₹1,458

Note: The illustrative figures are sourced from the SBI General Griha Raksha Plus policy document. Final premiums will depend on factors that define the risk profile of home building and contents. You may use a home insurance premium calculator for rough estimates.

How to Choose the Right Home Insurance Policy?

01

Identify What Needs Protection

Choose coverage based on your situation. Homeowners may need building and contents cover, tenants usually need contents cover, while landlords may benefit from building and loss-of-rent protection.

02

Calculate the Right Sum Insured

Insure the structure based on reconstruction cost, not market value, property price, or loan amount. A higher rebuilding cost requires adequate cover.

03

Include Contents and Valuables

Furniture, appliances, electronics, clothing, and household items can be expensive to replace. High-value items such as jewelry and artwork often require a separate declaration.

04

Check Disaster Coverage

Ensure protection against fire, flood, earthquake, cyclone, storm, landslide, terrorism, and water damage from overflowing tanks or pipes.

05

Look for Additional Benefits

Features such as alternate accommodation and loss-of-rent coverage can be valuable if the property becomes uninhabitable after an insured event.

06

Review Claims and Exclusions

Compare claim processes, digital support, turnaround time, coverage limits, and exclusions before choosing a policy. A smooth claims experience often matters more than a lower premium.

Home insurance varies from city to city. For example, the risks that matter in Chennai are completely different from those in Delhi or Uttarakhand. Here’s a simple guide:

City or Region

Primary Risk

Must-Have Cover

Mumbai, Chennai, or Assam

Flood or inundation

Enhanced flood cover

Delhi, Uttarakhand, or the Northeast areas

Earthquake (Seismic Zones IV–V)

Earthquake add-on

Bengaluru or Pune

Relatively lower natural risk

Fire + theft + contents is sufficient for most people

Coastal Andhra Pradesh, Odisha, or Tamil Nadu

Cyclone or storm

Storm or cyclone cover

How to File a Home Insurance Claim?

Step 1: Inform your insurer immediately and share basic details, including policy number, incident details, and photographs.

Step 2: Contact the relevant authority based on the event, such as the police for theft or the fire brigade for fire-related losses.

Step 3: Complete and submit the claim form as early as possible, along with the required details.

Step 4: Keep photographs, bills, repair estimates, First Information Reports (FIRs), proof of ownership, and other relevant records ready.

Step 5: Allow inspection of the property and provide accurate information about the loss.

Step 6: Carry out only urgent repairs before approval and preserve all bills and evidence.

Step 7: Track the claim status and request explanations for any deductions or exclusions applied to the final payout.

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 24,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or chat on WhatsApp.

Conclusion

Home insurance is not mandatory in India, but rebuilding a damaged home is far more expensive than the premium you save by avoiding it. For homeowners, it can be a valuable layer of financial protection against unexpected losses.

After securing adequate health and life insurance, the next step is protecting the assets you've worked hard to build. A well-chosen home insurance policy can help safeguard your home, belongings, and finances against unexpected events that could otherwise cause significant losses.

While Ditto's advisory services are limited to health insurance and term life insurance, understanding home insurance remains an important part of overall financial planning.

Frequently Asked Questions

Is home insurance mandatory in India or optional?

A home insurance policy is completely optional in India. No law requires homeowners or tenants to buy it, and banks do not make it mandatory for home loan approval. However, that does not mean it lacks value. A single mishap, like theft, can lead to substantial financial losses. Many homeowners assume such events are unlikely until they face a costly repair or replacement bill. Home insurance acts as a financial safety net and helps protect one of your largest assets. Popular home insurance plans include ICICI Lombard Complete Home Protect and HDFC ERGO Home Shield Insurance.

What does home insurance cover in India?

Home insurance generally protects both the structure of your home and the belongings inside it. Structural coverage includes walls, roofs, flooring, fixtures, fittings, garages, and other permanent parts of the property. Contents coverage protects furniture, appliances, electronics, clothing, and household items against insured risks. Most policies cover events such as fire, theft, burglary, floods, storms, cyclones, earthquakes, and other natural calamities. Some plans also cover alternative accommodation expenses if the property becomes unfit to live in after an insured event. High-value items such as jewelry or artwork may require separate declaration and coverage.

Is home insurance the same as home loan insurance?

No, home insurance and home loan insurance serve very different purposes. Home insurance protects your property and household contents against physical damage caused by risks such as fire, theft, floods, earthquakes, and other insured events. Home loan insurance, often structured as a group term insurance plan linked to a housing loan, protects the outstanding loan amount if the borrower dies during the loan tenure. Home loan insurance is a credit life insurance product linked to your home loan. In simple terms, home insurance protects the house, while home loan insurance protects the lender's financial exposure.

What are the main exclusions in home insurance policies?

Home insurance policies do not cover every type of loss. Common exclusions include damage arising from war, invasion, civil unrest, nuclear risks, and intentional destruction by the insured. Normal wear and tear, aging, rust, corrosion, and gradual deterioration are also excluded. Most insurers do not cover pre-existing structural defects or damage caused by negligence. High-value items such as jewelry, artwork, or collectibles may not be covered unless specifically declared. It is important to read the policy wording carefully because exclusions often play a major role in claim approval and settlement outcomes.

What is the Bharat Griha Raksha policy, and who should buy it?

Bharat Griha Raksha is IRDAI's standard home insurance product, designed to provide simple, transparent protection for residential properties. Introduced in 2021, it is offered by general insurers across India with a largely uniform structure. If you insure the building under this policy, household contents automatically receive coverage equal to 20% of the building sum insured, subject to a maximum of ₹10 lakh, unless a higher amount is selected. The policy suits homeowners, apartment owners, landlords, and even tenants who need contents-only coverage. It is often considered a good starting point for home insurance buyers.

What documents do I need to file a home insurance claim?

The exact paperwork depends on the nature of the claim, but some documents are commonly required. These include the policy copy, claim form, photographs or videos of the damage, repair estimates, proof of identity, proof of address, and ownership documents. For theft or burglary claims, an FIR is usually required. Fire-related claims may require a fire brigade report. Insurers may also request invoices, purchase receipts, valuation certificates for valuables, or reports from engineers and surveyors. Maintaining proper records of household purchases and property documents can make the claim process faster and significantly smoother.

Can tenants buy home insurance for rented flats?

Yes, tenants can purchase home insurance and often benefit from contents-only coverage. While the building structure is usually the landlord's responsibility, tenants remain financially exposed to loss or damage involving furniture, electronics, appliances, clothing, and personal belongings. The Bharat Griha Raksha policy offers a contents-only option suitable for renters. Bharat Griha Raksha is often considered a good starting option for home insurance buyers. Before buying a policy, tenants should estimate the replacement value of their belongings and choose a coverage amount that accurately reflects that value.

Does home insurance cover natural disasters like floods and earthquakes?

Yes, most comprehensive home insurance policies cover natural disasters such as floods, earthquakes, cyclones, storms, lightning, landslides, and inundation. These events can cause severe structural damage and substantial losses to household contents. Coverage, however, depends on the policy wording and selected benefits. Some insurers may apply limits, conditions, or waiting periods for specific risks. Since natural calamities vary by region, it is important to check whether your policy adequately covers the hazards most relevant to your location. Reviewing the policy schedule carefully helps ensure there are no surprises when a claim arises.

What should I check when renewing my home insurance policy?

Home insurance is not a set-and-forget product. At every renewal, review whether your building sum insured still reflects current construction costs, since rebuilding expenses tend to rise over time. Reassess the value of your household contents and declare any new valuables such as jewelry, electronics, or expensive appliances. It is also a good time to check whether your existing add-ons remain relevant and whether new covers may be useful. Instead of automatically renewing the same policy each year, compare benefits, exclusions, claim support, and premiums across insurers to ensure you continue receiving adequate protection.

Does home insurance cover more than just fire and natural disasters?

Yes. Modern home insurance policies often provide much broader protection than many homeowners realize. Under the standard Bharat Griha Raksha policy, benefits may include expenses for alternative accommodation if the home becomes uninhabitable, debris removal costs, architect fees, and automatic increases in the sum insured on eligible multi-year policies. Many comprehensive householder plans also offer optional covers for electrical and appliance breakdown, domestic worker liability, loss of keys, lock replacement, wallet loss, ATM robbery, and even pet-related coverage. The exact benefits vary by insurer, making it important to review the policy wording carefully before purchase.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.