Axis Max Life Platinum Wealth Plan, offered by Axis Max Life Insurance, is a unit-linked non-participating individual life insurance plan (UIN: 104L133V01). It combines market-linked investing with life insurance protection and offers access to 26 investment funds across equity, debt, hybrid, and index categories.

The plan also provides two investment strategies: Systematic Transfer Plan (STP) and Dynamic Fund Allocation. It supports Single Pay, Limited Pay, and Regular Pay options, with premiums starting from ₹2.5 lakh for Single Pay and ₹2 lakh annually for Limited Pay and Regular Pay variants.

However, the plan does not guarantee returns, and the fund value may rise, fall, or remain unchanged depending on market performance. Additionally, ULIPs come with a mandatory 5-year lock-in period during which the policyholder cannot surrender the policy or make partial withdrawals.

Unit-linked insurance plans (ULIPs) are designed for investors who want market-linked wealth creation along with life insurance under a single product. The Axis Max Life Platinum Wealth Plan targets this segment through features such as Guaranteed Loyalty Additions, Guaranteed Wealth Boosters, unlimited free fund switches, premium redirection, and automated portfolio management options.

Here’s a detailed Axis Max Life Platinum Wealth Plan review covering the plan’s features, charges, sample returns, and who it may suit.

Key Features of Axis Max Life Platinum Wealth Plan

Feature

Details

Policy Term

10 years for Single Pay and 10 to 20 years for Limited Pay and Regular Pay.

Premium Payment Options

Single Pay, 5-Pay, and Regular Pay

Minimum Premium

Single Pay: ₹2,50,000, Limited Pay and Regular Pay: ₹2,00,000 per annum.

Fund Options

26 fund options across different risk categories

Investment Strategies

Systematic Transfer Plan (STP) and Dynamic Fund Allocation

Premium Redirection

Up to 6 premium redirections per policy year, free of charge

Partial Withdrawals

Up to 2 withdrawals per year after lock-in

Policy Administration Charges

Applicable for the first 5 policy years and nil from year 6 onward

Sum Assured on Death

Depends on age and premium payment term, ranging from 1.25 to 10x annual premiums.

Maturity Benefit

Fund Value as at maturity, provided the Settlement Option has not been exercised.

Death Benefit

In case of death during the policy term, the nominee receives the higher of Sum Assured, reduced by applicable partial withdrawals, or Fund Value, subject to a minimum of 105% of all premiums paid.

Benefits of the Axis Max Life Platinum Wealth Plan

1) Guaranteed Loyalty Additions & Wealth Boosters: The Axis Max Life Platinum Wealth Plan offers Guaranteed Loyalty Additions and Guaranteed Wealth Boosters through additional units credited to the policy fund at specified milestones, subject to all due premiums being paid.

For annual premiums below ₹5 lakh, Wealth Boosters of 2% are added at the end of policy years 10, 15, and 20. For premiums of ₹5 lakh and above, the booster increases to 2.5% at the same intervals. However, these additions do not guarantee returns. The final fund value still depends on market performance, policy charges, mortality deductions, and applicable taxes.

2) Flexible Investment Options: The plan provides 26 funds across different risk categories. These include equity, debt, balanced, index, and other fund options. Investors can choose funds based on their financial goals, time horizon, and risk appetite. The fund mix ranges from low-risk debt funds to medium-risk balanced funds and higher-risk equity funds. Fund value may rise, fall, or remain unchanged depending on market movement and fund performance.

3) Automated Investment Strategies: The plan offers two investment strategies:

Systematic Transfer Plan (STP): Under STP, the single or annual premium, net of applicable premium allocation charges, is initially allocated to the Secure Plus Fund and then automatically switched every month to the Growth Super Fund or Growth Super Fund II, as selected at policy inception. This strategy is available only for Single Pay policies or policies with an annual premium payment mode.

Dynamic Fund Allocation: Dynamic Fund Allocation automatically shifts the investment allocation from equity-oriented funds toward more conservative funds as the policy approaches maturity. This option can be chosen only at policy inception.

4) Premium Redirection and Partial Withdrawals: The plan allows up to 6 premium redirections per policy year at no additional charge. After the first 5 policy years, policyholders may take up to 2 partial withdrawals per policy year, subject to the policy terms and conditions.

5) Zero Policy Administration Charges After Year 5: The plan does not charge any policy administration fee after the fifth policy year, allowing more of the investment to remain allocated toward fund growth. However, policy administration charges apply during the first 5 policy years. For Single Pay, the charge is ₹330 per month during years 1 to 5. For Limited Pay and Regular Pay, it is 3.3% of annualized premium, capped at ₹6,000 per annum, during years 1 to 5.

6) Maturity Benefit: If the Settlement Option is chosen, the insurer continues to manage the funds for up to 5 years from the maturity date and makes periodic payments. During the settlement period, fund management charges continue to apply. The plan also provides risk cover equal to 105% of total premiums paid during the settlement period, and mortality charges are deducted based on the sum at risk.

7) Important Charge Caveat: For annualized premiums below ₹2 lakh, an additional allocation charge of 1% applies for the first five policy years. The plan also has Fund Management Charges (FMC), mortality charges, surrender or discontinuance charges, and rider charges, where applicable.

8) Death Benefit: In case of the life assured’s death during the policy term, the nominee receives the higher of the Sum Assured, reduced by applicable partial withdrawals, or the Fund Value as of the date of death. This is subject to a minimum of 105% of all premiums paid. The applicable Sum Assured depends on the premium payment option, entry age, and policy structure.

9) Tax Benefits: Premiums paid and benefits received under the Axis Max Life Platinum Wealth Plan may qualify for tax benefits under prevailing income tax laws, subject to applicable conditions. ULIPs generally offer deductions under Section 80C, while maturity proceeds may qualify for tax exemption under Section 10(10D). However, tax rules introduced in 2021 reduced some ULIP tax advantages, particularly for policies with annual premiums exceeding ₹2.5 lakh.

CTA

Sample Premiums

Age of Life Insured

Premium Payment Option

Annualized / Single Premium

Policy Term

Premium Payment Term

Fund Value at 4%

Fund Value at 8%

IRR at 8%

40

Regular Pay

₹2,00,000 p.a.

20 years

20 years

₹56,30,630

₹88,51,496

7.08%

35

Regular Pay

₹3,50,000 p.a.

20 years

20 years

₹99,08,504

₹1,55,91,947

7.13%

40

Limited Pay

₹5,00,000 p.a.

10 years

5 years

₹30,35,003

₹41,41,692

6.46%

35

Limited Pay

₹2,00,000 p.a.

10 years

5 years

₹11,82,866

₹16,11,518

6.10%

40

Single Pay

₹4,00,000

10 years

Single Pay

₹4,90,543

₹7,20,277

6.06%

35

Single Pay

₹7,50,000

10 years

Single Pay

₹9,56,835

₹14,00,464

6.44%

Note: The above figures are illustrative (sourced from the official Axis Max Life Platinum Wealth Plan brochure) and based on assumed returns of 4% and 8% after applicable charges. These returns are not guaranteed, and actual fund performance may vary depending on market conditions. Applicable taxes and levies will be deducted as per prevailing laws.

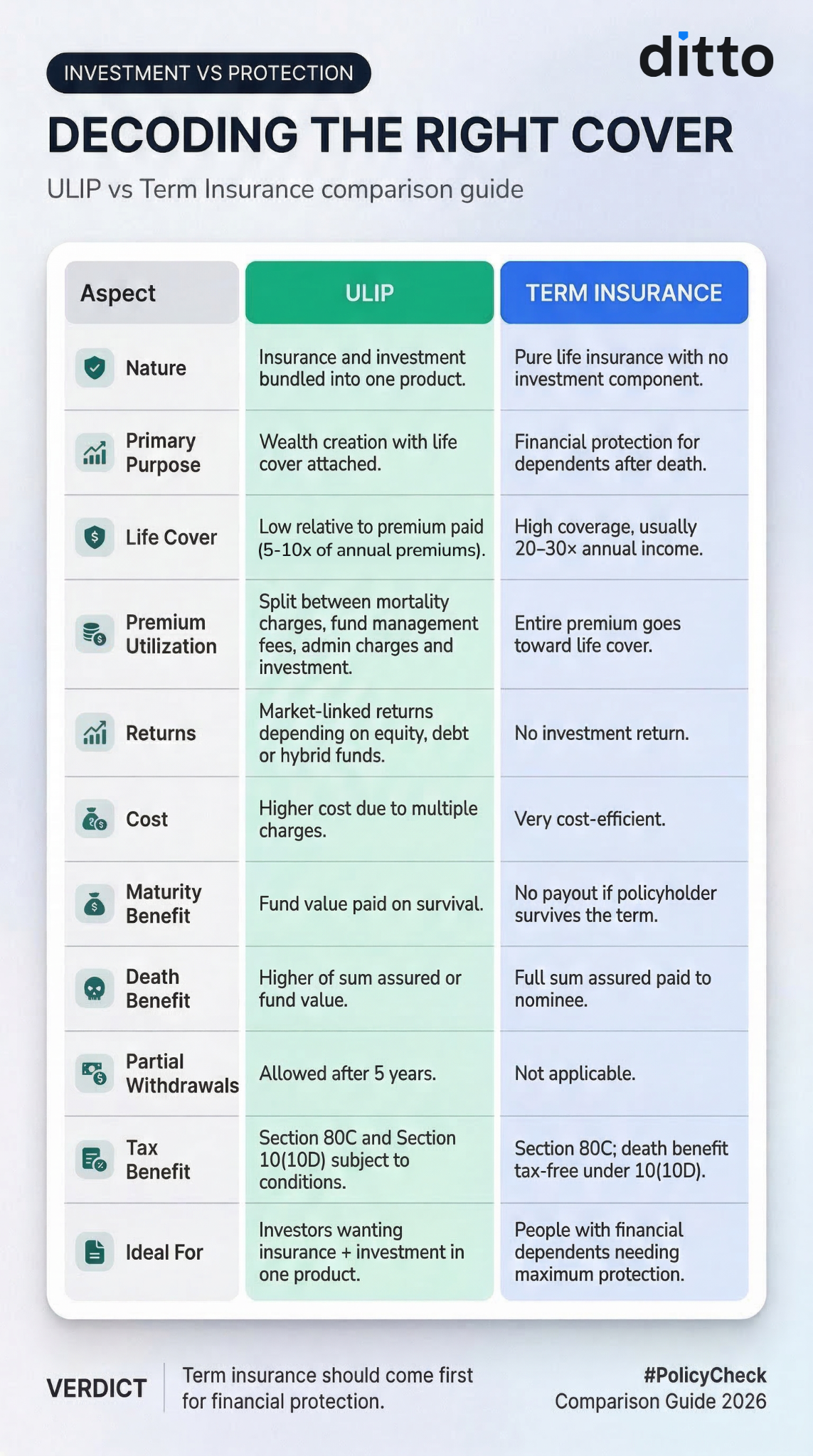

ULIP vs. Term Insurance: Which Is Better?

To understand how ULIPs compare with simpler alternatives, you can also read our detailed guide on ULIP vs term insurance.

This Plan May Suit You If:

You already have sufficient term insurance coverage

You are comfortable with market-linked returns

You can stay invested for the full 10 to 20 years

You value loyalty additions and wealth boosters

You understand the charges and lock-in conditions

This Plan May Not Be Ideal If:

You need high life coverage at a lower premium

You prefer guaranteed returns and do not want market-linked risk

You may need liquidity within the first 5 years

You want lower-cost investment alternatives

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

The Axis Max Life Platinum Wealth Plan is a feature-rich ULIP designed for long-term investors seeking market-linked wealth creation along with life insurance protection. However, this is still a ULIP. It combines insurance and investment into a single product. While this may suit investors looking for disciplined long-term investing, it may not be the most efficient option for pure financial protection.

If you are looking for pure protection, we recommend exploring comprehensive term insurance plans before considering ULIPs, such as the Axis Max Life Platinum Wealth Plan, as an additional investment option.

If you prefer Axis Max Life Insurance as the insurer, its flagship term plan, Smart Term Plan Plus (STPP), can be considered for pure protection needs, as it offers significantly higher life cover at a lower premium compared to ULIPs like the Axis Max Life Platinum Wealth Plan.

Frequently Asked Questions

What is the Axis Max Life Platinum Wealth Plan?

The Axis Max Life Platinum Wealth Plan is a unit-linked non-participating life insurance plan that combines market-linked investments with life insurance protection. It offers access to up to investment funds across equity, debt, hybrid, and index categories. The plan also includes features such as Guaranteed Loyalty Additions and Guaranteed Wealth Boosters, which add extra units to the policy value at specified milestones. Investors can choose between Single Pay, 5-Pay, and Regular Pay options depending on their financial goals and investment horizon. The plan comes with a mandatory 5-year lock-in period, as applicable to all ULIPs.

What is the minimum premium for the Axis Max Life Platinum Wealth Plan?

The minimum premium under the Axis Max Life Platinum Wealth Plan depends on the premium payment option selected. For the Single Pay variant, the minimum one-time premium is ₹2,50,000. For Limited Pay and Regular Pay variants, the minimum premium is ₹2,00,000 per annum. The plan is designed for investors seeking long-term market-linked wealth creation through a ULIP structure. Depending on the entry age and policy structure, the sum assured can go up to 10 times the annual premium. However, since the life cover may still be limited compared to a standalone term plan, additional term insurance may be required for adequate financial protection.

What are Guaranteed Loyalty Additions and Wealth Boosters?

Guaranteed Loyalty Additions and Guaranteed Wealth Boosters are additional units credited to the policyholder’s fund value at specified policy years. These are subject to all due premiums being paid. If the policy is revived, additions for previous years are based on the fund value at revival. If the policyholder reduces the premium after the 5-year lock-in period, future additions are calculated based on the revised premium. Wealth Boosters are credited every five years starting from the 10th policy year. The applicable rate depends on the annualized premium band.

What is the lock-in period in the Axis Max Life Platinum Wealth Plan?

Like all ULIPs regulated by IRDAI, the Axis Max Life Platinum Wealth Plan comes with a mandatory 5-year lock-in period. During this period, policyholders cannot make partial withdrawals or fully surrender the policy to access their invested amount. If the policy is discontinued within the first five years, the accumulated amount is transferred to a discontinued policy fund, where it earns a minimum guaranteed return as prescribed by regulations. After completing the lock-in period, policyholders can make up to two partial withdrawals per policy year, subject to policy terms and conditions.

How many fund options are available under the plan?

The Axis Max Life Platinum Wealth Plan offers 26 fund options across equity, debt, hybrid, ESG, thematic, and index-based categories. Some of the key funds include High Growth Fund II, Growth Super Fund, Growth Super Fund II, Diversified Equity Fund, Balanced Fund, Dynamic Bond Fund, Secure Fund, Nifty Alpha 50 Fund, Nifty 500 Momentum 50 Fund, Sustainable Equity Fund, and BSE 500 Value 50 Index Fund. The plan also offers premium redirection, unlimited free switches, and partial withdrawals after the 5-year lock-in period, subject to policy conditions.

What charges apply under the Axis Max Life Platinum Wealth Plan?

The plan includes charges such as Fund Management Charges (FMC), mortality charges, and applicable premium allocation charges depending on the variant selected. Fund Management Charges are deducted from the Net Asset Value (NAV) of the chosen funds, while mortality charges are deducted for providing life insurance coverage. One notable feature is that policy administration charges become zero after the fifth policy year. Although these charges are standard across ULIPs, they can impact long-term returns. Investors should carefully review the official Axis Max Life Platinum Wealth Plan brochure to understand the complete charge structure before investing.

Is the Axis Max Life Platinum Wealth Plan better than mutual funds plus term insurance?

For most investors, buying a standalone term insurance plan and investing separately through mutual funds may offer greater flexibility, lower costs, and higher insurance coverage. A term plan provides substantial life cover at relatively lower premiums, while mutual funds allow investors to choose investment products without insurance-linked charges. However, the Axis Max Life Platinum Wealth Plan may appeal to investors seeking a disciplined long-term investment product with built-in life insurance, automated investment strategies, loyalty additions, and wealth boosters. The suitability depends on an investor’s financial goals, risk appetite, liquidity needs, and existing insurance coverage.

What happens if I surrender the plan after the lock-in period?

If the policyholder surrenders the Axis Max Life Platinum Wealth Plan after completing the mandatory 5-year lock-in period, the surrender value payable will be at least equal to the prevailing fund value on the date of surrender. Since this is a market-linked ULIP, the final amount depends on factors such as fund performance, market movements, policy charges, and applicable deductions during the policy term. The plan does not provide guaranteed investment returns, and the fund value may increase or decrease based on market conditions. Policyholders should therefore evaluate their liquidity needs carefully before investing in this long-term product.

Who should consider buying the Axis Max Life Platinum Wealth Plan?

The plan may suit investors who already have adequate term insurance coverage and are looking for a long-term market-linked investment product with life insurance benefits. It is particularly suitable for individuals comfortable with equity market volatility and willing to remain invested for 10 to 20 years. Investors seeking features like automated investment strategies, loyalty additions, wealth boosters, premium redirection, and partial withdrawals after the lock-in period may also find the plan appealing. However, individuals looking primarily for affordable life insurance protection or short-term liquidity may find standalone term insurance and mutual funds more suitable alternatives.

What is the death benefit under the Axis Max Life Platinum Wealth Plan?

In case of the life assured’s death during the policy term, the nominee receives the highest of three amounts: the applicable Sum Assured, the Fund Value as on the date of death, or 105% of the total premiums paid. The Sum Assured may be reduced to the extent of applicable partial withdrawals made during the two years preceding death, as per policy conditions. The exact death benefit depends on the premium payment option, entry age, and chosen sum assured multiple. This structure ensures a minimum protection benefit even if market performance temporarily affects the policy’s fund value.

Last updated on:

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.