![United India Health Insurance Premium Chart [2026]](https://stat.joinditto.in/images/2026/05/United-India-Health-Insurance-Premium-Chart@2x.webp)

Overview

Health insurance is supposed to give you peace of mind, yet most people feel lost the moment they see premium tables and rate charts. Why does the price jump at age 36 and then again at 41? Why isn’t the premium for a ₹20 lakh cover exactly double the premium for ₹10 lakh?

This is where the United India health insurance premium chart helps. This article explains how to calculate your premium online, download the United India health insurance premium chart PDF, and interpret the numbers.

What Is the United India Health Insurance Premium Chart?

The premium chart is an official document published by United India Insurance Company Limited (UIIC) that lists the base rates. There is a separate chart for each policy the company offers.

The premium chart is a pricing reference guide. It shows you, at a glance, how much you would pay per year based on your age, the coverage you want, whether you're buying just for yourself or your whole family, and what city you live in.

Note: The chart only shows base premiums. Your final premium may differ depending on optional add-ons, underwriting decisions, or any discounts applicable to your plan.

United India Health Insurance Premium Chart: Age-Wise Rates

Here are sample premiums from the United India Family Medicare policy for a ₹15 lakh sum insured across different profiles and zones.

Note: A stands for adult and C stands for child. Values are indicative and may vary based on age, location, and medical underwriting.

Premium Analysis: Zone A premiums are noticeably higher than those in Zone C. That's because healthcare costs in cities like Delhi and Mumbai are higher, and insurers price policies accordingly.

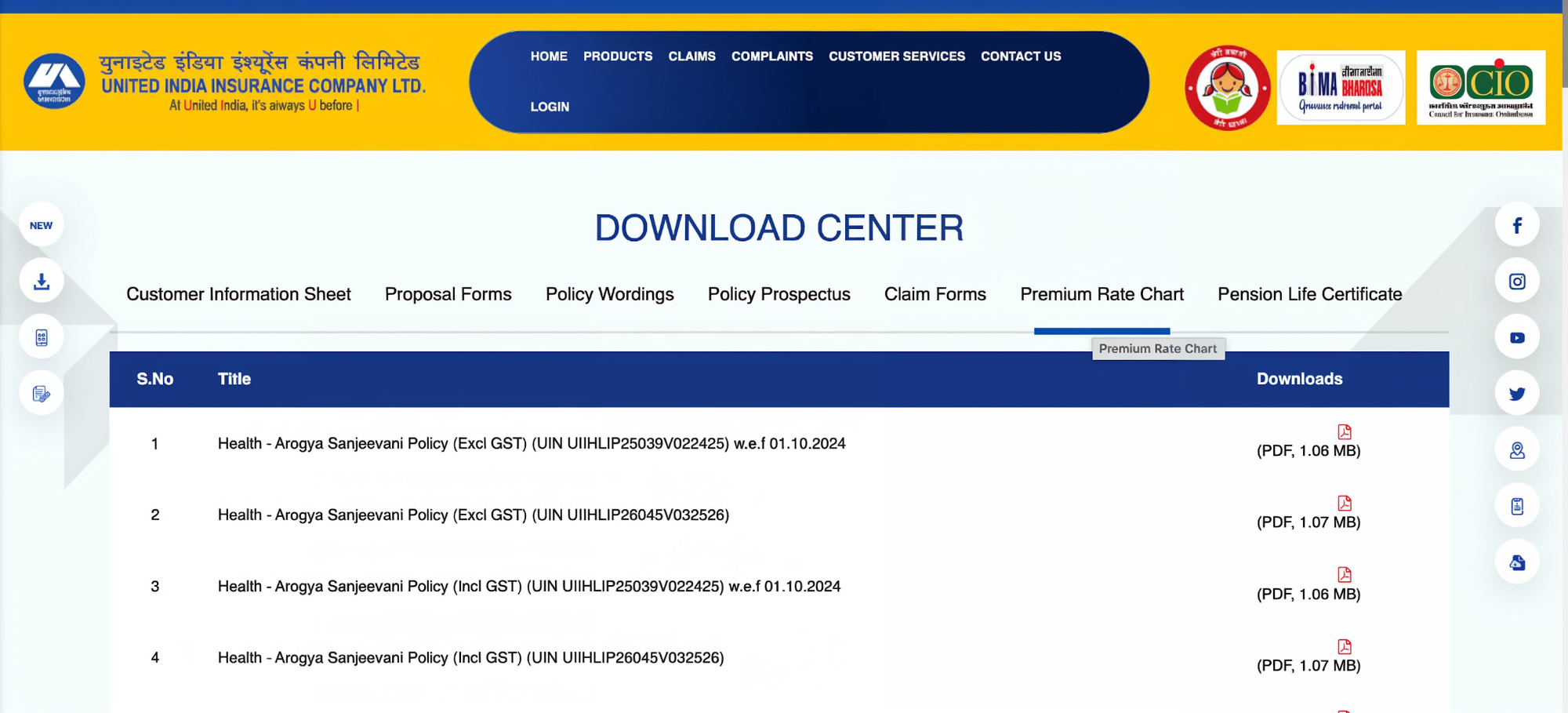

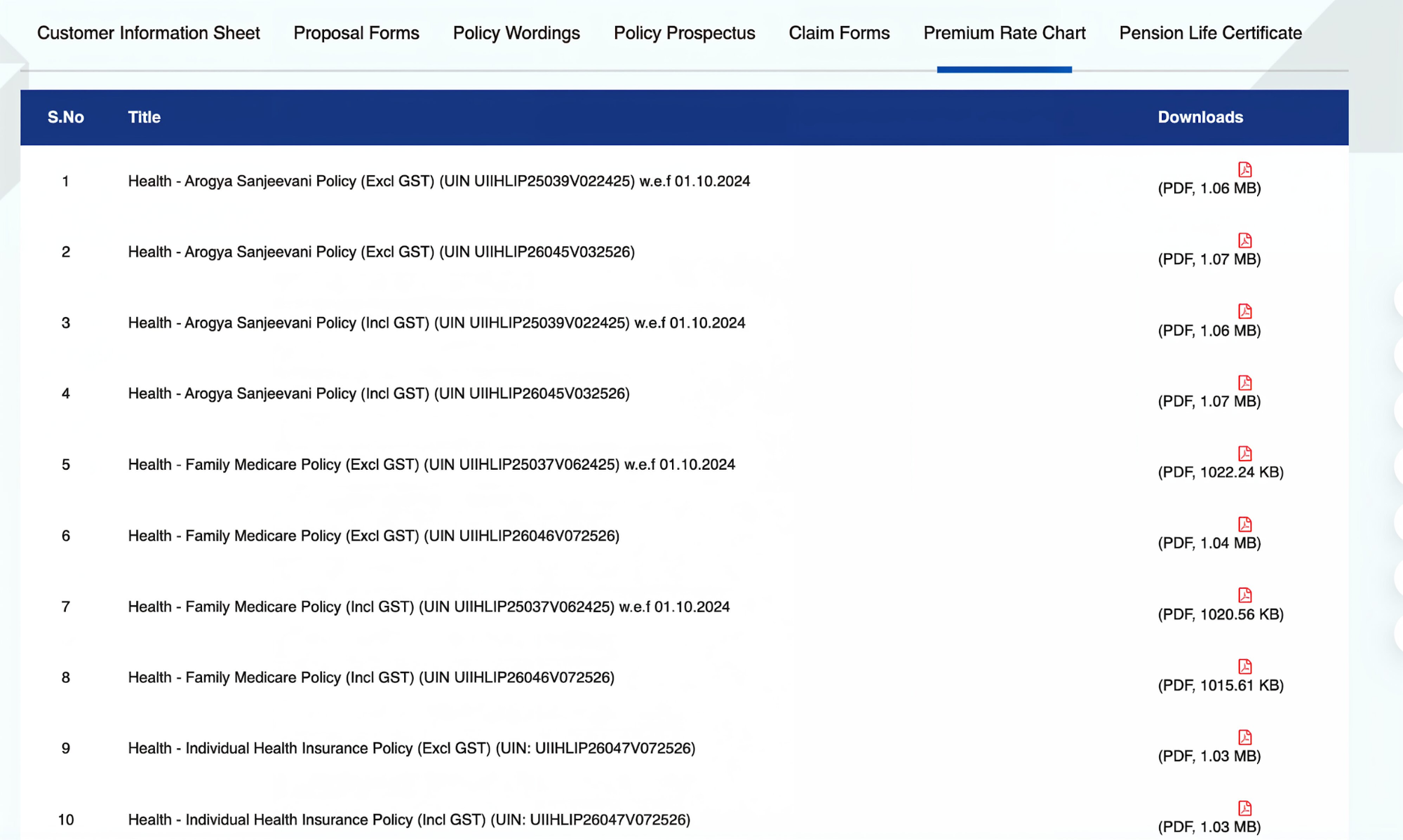

How to Download the United India Health Insurance Premium Chart PDF

- Go to United India health insurance’s official website and click on the download links section.

- Navigate to the premium chart tab under the download center tab.

- You’ll see a list of available United India health plans.

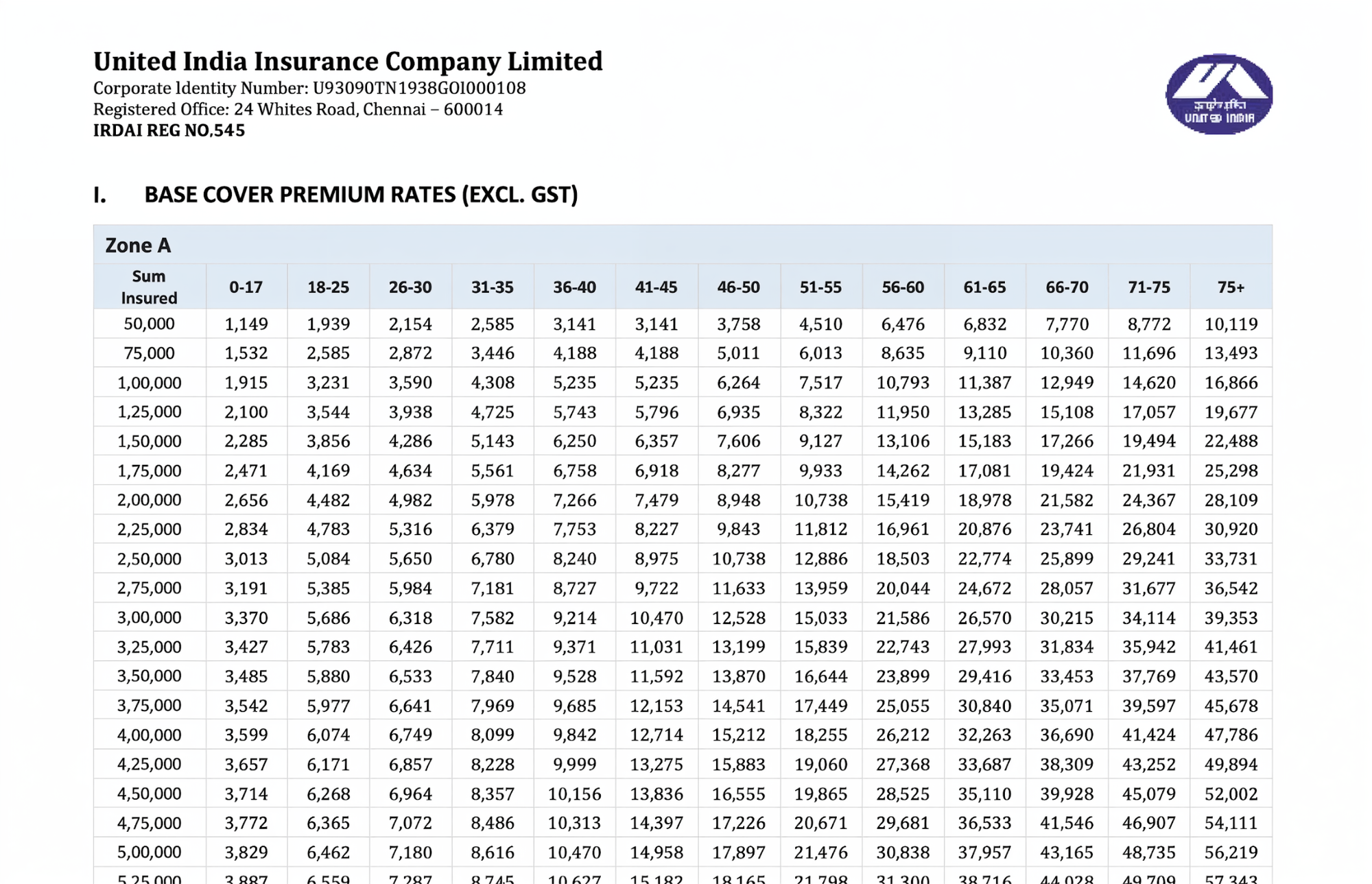

- Click on the plan name to open its premium chart. You can download the PDF or view it online. For reference, here’s what a typical United India health insurance premium chart PDF looks like:

Key Note: Always download the premium chart from the insurer’s official website, as third-party information can be outdated or inaccurate.

What Will You Find Inside the PDF?

How to Use the United India Health Insurance Premium Calculator

- Go to https://uiic.co.in/ and choose your preferred language.

- Navigate to the customer services tab on the home page and choose the health premium calculator option.

- Enter the required details, such as plan type, family members, sum insured, pincode/city, age, and mobile/email (if asked).

- View premium results and available plan options.

Factors That Affect United India Health Insurance Premiums

Age of Insured Members

Premiums increase with age because the likelihood of illness, hospitalization, and claims rises. Prices change by age bracket, which is why your cost can increase significantly when you reach 36 or 46.

Sum Insured (SI) Selected

Higher SI means greater financial protection, but it also increases premiums since the insurer’s potential payout is higher. However, the increase is not linear. A ₹20 lakh cover will cost comparatively more than a ₹10 lakh cover, but not exactly double.

Policy Type (Individual vs. Floater)

With individual plans, each person has their own sum insured and premium. But with a family floater, everyone shares one common sum insured, and the premium is calculated based on the age of the eldest member. For young families, floaters tend to be cost-effective.

Medical History and Add-Ons

If you have pre-existing conditions, the insurer may apply an additional loading on your premium after underwriting. Optional covers, such as restoration benefits or consumables coverage, also increase your total premium.

Location

In most plans, metro cities (Zone A) typically have higher premiums than tier-2/3 cities (Zones B/C).

Here’s a simplified zone classification for the Family Medicare policy for reference.

Please Note: For the complete zone division, please refer to the policy wording.

Popular United India Health Insurance Plans With Premium Charts

Note: For a clearer look at the insurer’s claim process, plan features, drawbacks, and overall suitability, you can check our comprehensive United India health insurance review.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or chat with our advisors on WhatsApp.

Conclusion

The United India health insurance premium chart is a useful starting point for comparing base rates across age bands, sum insured options, and zones. But the chart is only half of the equation, the plan itself is the other half, which matters just as much as the price.

At Ditto, Public Sector Undertaking (PSU)- backed insurers, such as United India, are usually not our first recommendation for most retail health insurance buyers. This is because the plans tend to be outdated, with room rent limits, disease-wise sub-limits, and restrictive policy features. More importantly, United India processes claims through third-party administrators (TPAs), which adds an extra layer to each claim, often leading to delays, more paperwork, and slower resolution when you need help most.

Our Recommendation: Before you compare premiums, we'd encourage you to check our list of the best health insurance companies in India, most of which offer better coverage, stronger claim support, and a smoother experience overall.

Frequently Asked Questions

Last updated on: