Quick Overview

Imagine buying a ₹5 lakh health insurance policy at 25 because you’re healthy and the premiums look affordable. Years later, you realize the coverage is not enough. A treatment costing ₹10-₹15 lakh can leave you paying a part of the hospital bill yourself, even after having a policy for years.

This is exactly what happens when health insurance is chosen for short-term convenience instead of long-term value.

In this article, we will cover common mistakes to avoid while buying health insurance, health insurance tips for beginners, and how to make smarter long-term choices.

Not Understanding Your Health Insurance Needs Properly

Choosing Insufficient Sum Insured

Not Considering Comprehensive Coverage

Buying Plans Based Only on Price

Ignoring Family Medical History

Bottom Line:

- Consider at least ₹15 - ₹25 lakh as the base cover.

- Buy insurance early and opt for higher coverage.

- Evaluate whether a family floater plan or separate policies make more sense.

Overlooking Important Policy Terms and Conditions

Waiting Periods and Exclusions

Slow-growing illnesses, such as cataract surgery, have a waiting period of 1–2 years, while pre-existing conditions have waiting periods of up to 3 years. Policies also list permanent exclusions like cosmetic surgeries, which are not covered at all.

Room Rent Restrictions

Room rent limits affect the entire hospital bill, not just the room charges. If your policy allows a room up to ₹5,000 per day but you choose a ₹10,000 room, the insurer applies proportionate deductions to the entire bill, including expenses like surgery and doctor fees.

Non-Disclosure Consequences

People often assume that past illnesses don’t need to be disclosed. However, insurers review medical records when processing claims, and undisclosed conditions such as childhood asthma or fractures can lead to claim rejection.

Key Insights

Common Health Insurance Mistakes During Policy Comparison

1) Not Checking Network Hospitals

If your preferred hospital is not in the insurer’s network, you may need to pay upfront and claim reimbursement later. Remember, cashless does not always mean zero payment. You may still pay for non-medical items and for exclusions under the policy.

2) Ignoring Claim Settlement Ratio

If the insurer is inconsistent in claims, you may experience approval delays. The ideal solution is to use the claim settlement ratio as a starting point, and also check the incurred claim ratio and the volume of claims or disputes reported.

3) Choosing Unnecessary Add-ons

Adding riders like maternity or OPD coverage may look like better coverage, but can increase your premium. So, start with a solid base policy first and only pick add-ons that improve your coverage, like consumables and bonus add-ons.

4) Not Checking Restoration Benefits

Restoration refills your sum insured after it is used for a claim, helping you stay covered for multiple hospitalizations in the same policy year. This is useful in family floater plans, where coverage can get exhausted quickly.

Financial Mistakes That Increase Long-Term Costs

Skipping Renewals

A lapsed policy means losing waiting periods and accumulated bonuses. Restarting coverage involves higher premiums due to age and fresh underwriting.

Not Considering Medical Inflation

With medical inflation rising around 10%-12% every 2-3 years, treatment costs can double within a decade. Hence, choose higher coverage and supplement your base policy with a super top-up plan to account for rising healthcare costs.

Delaying the Purchase of Personal Health Insurance

Relying on corporate coverage and postponing a personal policy may look convenient. But buying insurance later usually means higher premiums and stricter underwriting.

Paying Through Installment Options

Some insurers offer EMI options, but these may include processing fees or higher total premiums due to interest. Paying annually or going for a multi-year policy is usually more cost-efficient.

Buying Without Comparing Prices and Discounts

Insurers offer different prices, discounts, and benefits across platforms. Taking time to compare health insurance plans can help you avoid paying more for similar coverage.

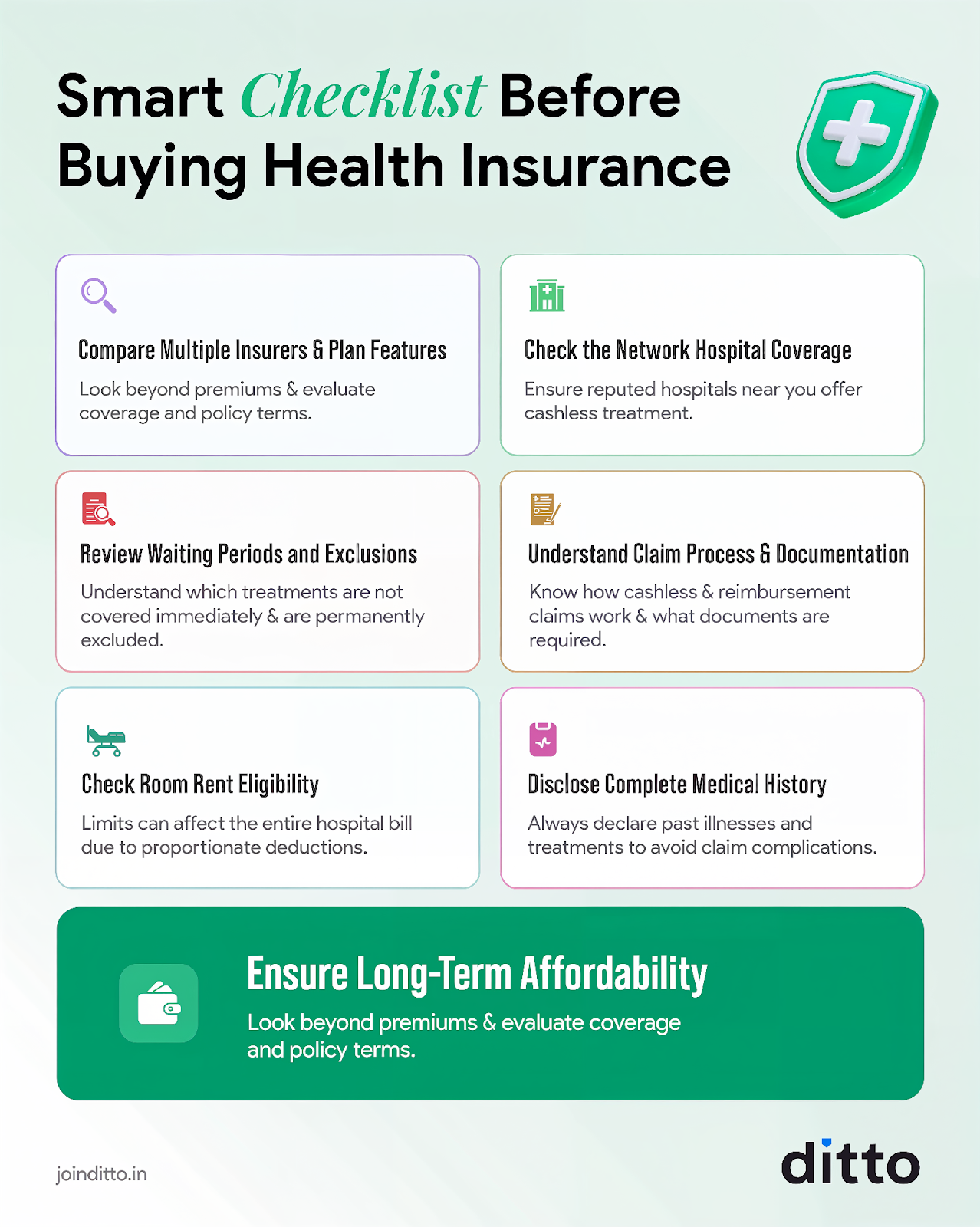

Smart Checklist Before Buying Health Insurance

You can refer to the infographic below to know the things to check before buying health insurance:

Bonus Tip: Consider taking guidance from a reliable insurance aggregator/agent who is well-versed in insurer operations and claim settlement practices. You can reach out to Ditto for personalized health/term insurance advice.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation with us. Slots are filling up quickly, so be sure to book a call now or chat with us on WhatsApp!

Conclusion

Buying health insurance is one of the most important financial decisions you will make for your family. However, many common health insurance mistakes occur simply because buyers rush the process rather than understanding the policy.

Review the things to check before buying health insurance, such as sub-limits, waiting periods, disclosing all medical details, and ensuring the plan fits your long-term healthcare needs. If you’re unsure which policy is right for you, you can start by checking the best health insurance plans to help you make a confident decision.

Frequently Asked Questions

Last updated on: