Overview

According to the Press Information Bureau (PIB), India's major ports handled 855 million tonnes of cargo in FY 2024–25, highlighting the country's expanding trade ecosystem. As cargo volumes continue to grow, marine insurance has become an essential safeguard for businesses against transit-related financial risks, which ensures goods remain protected from origin to destination.

In the next few minutes, you'll learn what marine insurance covers, how it works, who needs it, the different policy types, the claims process, and how to choose the right cover for your shipments.

What Is Marine Insurance?

Marine insurance is a contract under which an insurer compensates the insured for financial losses arising from risks during transit. Simply put, it acts as a financial safety net for businesses and individuals transporting goods or operating vessels, protecting them against losses from damage, theft, legal liabilities, and more during the journey.

Take Note: According to the IRDAI Annual Report 2024–25, India's marine insurance sector recorded a gross written premium of ₹5,504 crore, highlighting its vital role in safeguarding domestic and international trade.

Types of Marine Insurance: Cargo, Hull, Freight & Liability

Marine Cargo Insurance

Marine cargo insurance protects the goods being transported, not the ship carrying them. It compensates cargo owners, such as importers, exporters, traders, and manufacturers, if insured goods suffer loss or damage in transit. The cover extends across sea, air, road, rail, and multiple modes of transport, making it the most widely used type of marine insurance in India.

Hull & Machinery Insurance

Hull & Machinery (H&M) insurance protects the vessel itself, including its hull, engines, machinery, and onboard equipment. It serves as comprehensive insurance for ships, similar to comprehensive motor insurance for cars. This cover is essential for shipowners, fishing companies, vessel operators, charterers, and shipping lines that rely on commercial vessels.

Freight Insurance

Freight insurance protects the freight revenue that carriers, shipping companies, and freight forwarders expect to earn from transporting cargo. If goods are lost or damaged before delivery, the carrier can lose its freight charges. This policy helps safeguard business income, especially where freight is payable only upon successful delivery or is paid in advance.

Marine Liability Insurance

Marine Liability Insurance, commonly known as Protection and Indemnity (P&I) insurance, protects shipowners, charterers, and vessel operators against legal liabilities arising from vessel operations. It covers claims involving third-party injury, cargo damage, pollution, wreck removal, and property damage.

How Marine Insurance Works in India

Step 1: Assess Your Coverage Needs

Start by identifying what you need to insure. Consider the type of goods, mode of transport, shipping route, shipment frequency, and applicable Incoterms (a set of 11 internationally recognized rules that define the responsibilities of sellers and buyers). High-value or fragile cargo often requires broader protection, while businesses with regular shipments usually benefit from an open policy (one policy that covers multiple shipments over a defined period) rather than buying insurance for each consignment.

Step 2: Compare Quotes and Buy the Policy

You can purchase marine insurance directly from an insurer, through an IRDAI-registered insurance broker, or via a licensed bank offering trade finance. Compare coverage, exclusions, deductibles, and premiums before selecting a policy that matches your transit risks.

Step 3: Receive Policy Documents

After purchase, you receive the policy document or open cover certificate, a marine insurance certificate for each shipment (under open policies), and any endorsements for changes such as route modifications, additional cover, or higher insured value.

Step 4: Meet Your Policy Obligations

The insured must pack goods properly, accurately declare shipment details, and take reasonable steps to minimize losses during transit. Failure to follow these responsibilities can result in claim rejection.

Step 5: File a Claim if a Loss Occurs

Notify the insurer immediately after discovering the loss, arrange a survey, preserve evidence, and protect recovery rights against carriers or other liable parties. Submit all required documents, such as the survey report and claim form. Once the insurer verifies that the loss is covered under the policy, the claim is settled according to the policy terms.

Note: Most marine insurance policies require you to notify the insurer within 7 days of delivery if you discover loss or damage. Always verify the exact reporting timeline in your policy document, as delayed intimation can result in your claim being rejected.

Did You Know?

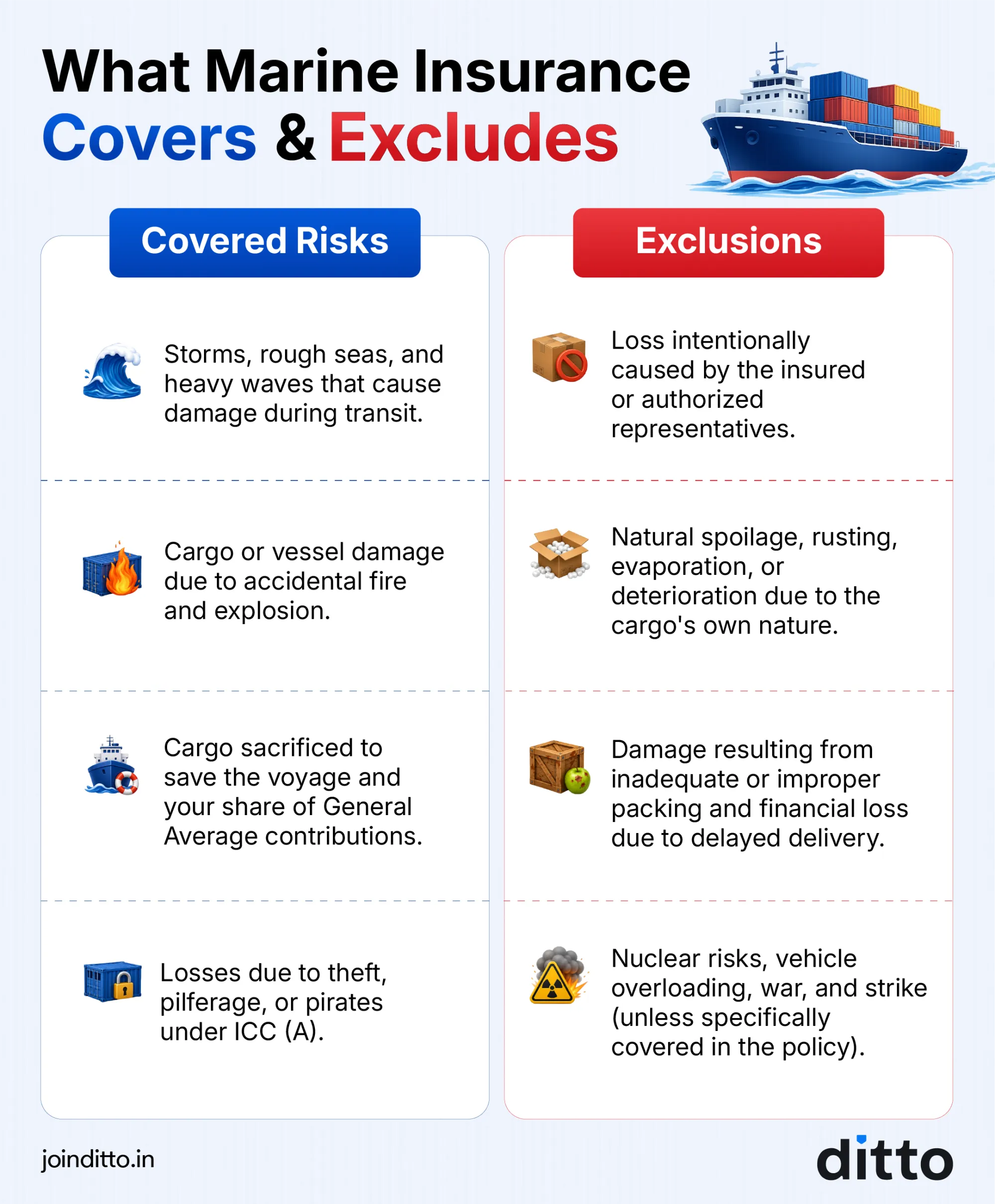

What Marine Insurance Covers and Excludes

ICC (A) is often marketed as "all-risk" cover, but it actually covers all risks except specific exclusions. Delay, poor packaging, inherent vice (a natural problem or weakness within the item itself that can cause it to be damaged without any external accident), war, and nuclear risks remain outside its scope. See the infographic below to understand exactly what is covered and what is not.

Popular Marine Insurance Providers in India

- The New India Assurance Company Limited: India's largest general insurer, offers cargo, hull, voyage, open, turnover, and duty insurance with ICC (A), (B), and (C) options.

- ICICI Lombard General Insurance: A leading private insurer known for digital-first marine solutions. ICICI Lombard offers cargo, hull, inland transit, open cover, and annual turnover policies with online policy issuance, digital certificates, and AI-enabled claims tracking.

- TATA AIG General Insurance: Well-suited for exporters and large commercial shipments. TATA AIG marine insurance provides cargo, hull, freight, transit, and marine liability coverage with strong expertise in international trade and Incoterms-backed transactions.

- Bajaj General Insurance: Bajaj General offers flexible marine cargo, hull, container, and annual turnover policies.

- HDFC ERGO General Insurance: Popular among Small and Medium-Sized Enterprises (SMEs) and import-export businesses. Provides cargo, export cargo, inland transit, and hull insurance, seamlessly integrated with trade finance and banking services.

- United India Insurance Company Limited: A trusted public-sector insurer with a strong presence in the Public Sector Unit (PSU), government, fisheries, and port-related marine business. Offers cargo and hull insurance backed by a wide survey and claims support network.

Take Note: After tariff deregulation (marine insurance pricing is no longer fixed, different insurers can charge different premiums based on risk, cargo type, route, claim history, etc.), don't compare only on the basis of prices. Assess claims settlement record, surveyor network, certificate issuance speed for Letters of Credit (LC) backed trade, digital capabilities, and solvency. For high-value or complex shipments, consider using an IRDAI-licensed marine insurance broker.

How to Buy a Marine Insurance Policy?

- Identify the right policy based on your shipping pattern. Next, choose an open policy or annual turnover policy for frequent shipments, a specific voyage policy for one-time consignments, an inland transit policy for domestic transport, and hull & machinery insurance if you own the vessel.

- Select the appropriate coverage based on your actual needs. For example, ICC (A) is suitable for high-value or fragile cargo, while ICC (B) or ICC (C) may be sufficient for bulk or lower-risk goods. You may add war and strikes coverage when shipments pass through high-risk regions.

- Calculate the correct sum insured. Ideally, insure the Cost, Insurance, and Freight (CIF) value plus 10% to cover expected profit and incidental expenses.

- Keep shipment details ready, including cargo description, packaging, value, transport mode, origin, destination, shipment frequency, and vessel details where applicable.

- Compare insurers based on coverage, claims support, and pricing. Standard cargo policies can usually be purchased online, while high-value, complex, or international shipments are often better handled offline through an IRDAI-licensed broker.

Goods and Services Tax (GST) Implications for Marine Insurance

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 25,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat over WhatsApp with our advisors.

Conclusion

Marine insurance is not just for large shipping companies. It is an essential safeguard for any business that moves goods by sea, air, road, or rail. A well-chosen policy protects against financial shocks, keeps supply chains resilient, and ensures business continuity. As India's trade ecosystem expands, the right marine insurance is more than just a compliance requirement. It is a smart business decision.

Note: Ditto offers personalized guidance and purchase assistance only for health insurance and term life insurance. We do not advise or facilitate the purchase of marine insurance or other general insurance products. Please consult a licensed general insurance intermediary or insurer for product-specific advice.

Frequently Asked Questions

Last updated on: