Overview

Business insurance is not just for large corporations. With over 7.86 crore Micro, Small, and Medium Enterprises (MSMEs) operating in India as of 2026, businesses of every size face risks that can threaten their financial stability. Whether it is a startup, manufacturing unit, or service business, unexpected events such as lawsuits, fire, employee injuries, or operational disruptions can lead to significant losses. This is where business insurance plays a critical role.

In the next few minutes, this guide explains the different types of business insurance, what they cover, how much they cost, and how to choose the right protection for your business.

What Is Business Insurance?

Business insurance is a broad category of policies designed to address the various risks a business faces throughout its lifecycle. After a loss, relying on personal savings or business cash flow helps transfer specific financial risks to an insurer. The coverage can be tailored to your industry, operational size, assets, employees, and legal obligations.

These policies are regulated by the Insurance Regulatory and Development Authority of India (IRDAI) and are offered by both public insurers like New India Assurance and Oriental Insurance and private insurers like TATA AIG and Bajaj General.

IRDAI introduced standardized fire and allied perils products, and for businesses, the two most relevant standard products are:

Types of Business Insurance Policies in India

- Fire & Property Insurance: Protects business premises, stock, machinery, furniture, and equipment against risks such as fire, floods, storms, and other insured events.

- Group Personal Accident Insurance (GPA): Provides fixed benefits for accidental death, permanent disability, or temporary disability suffered by employees. Often chosen for drivers, delivery personnel, security personnel, and site workers.

- Group Health Insurance: Covers employee hospitalization expenses and may include benefits such as maternity, wellness, and dependent coverage. Such policies help businesses improve employee welfare, retention, and overall workforce satisfaction. In India, group health policies are also offered by Standalone Health Insurance (SAHI) companies like Niva Bupa and Care.

- Public Liability Insurance: Protects against third-party injury or property damage claims arising from business operations. This type is particularly relevant for businesses with customer interactions or public-facing premises.

- Professional Indemnity Insurance: Protects professionals against claims involving negligence, errors, omissions, or poor professional advice. This kind is common among doctors, consultants, accountants, lawyers, and technology service providers.

Besides the above-listed types, there are employee compensation insurance, commercial general liability (CGL) business liability insurance, cyber insurance, marine cargo insurance, keyman insurance, and Directors & Officers (D&O) insurance.

Did You Know?

What Does Business Insurance Cover?

Property & Fire Insurance

Protects buildings, stock, machinery, furniture, fixtures, and other business assets against insured physical damage.

Business Interruption Insurance

Covers lost profits and ongoing expenses when operations are disrupted after an insured event.

Liability Protection

Includes product liability, professional indemnity, and directors & officers cover against legal and financial claims.

Cyber Insurance

Covers data breaches, ransomware attacks, cyber extortion, legal expenses, and business interruption losses.

Employee & Fraud Protection

Covers employee injury liabilities and losses arising from employee fraud, theft, or embezzlement.

Marine Cargo Insurance

Protects goods while they are transported by road, rail, air, sea, or courier.

Who Needs Business Insurance in India?

Any business with premises, inventory, employees, contracts, or legal liability should consider suitable insurance protection.

For example, factories and manufacturers face risks such as fire, machinery breakdown, worker injuries, and product defects. Warehouses and distributors deal with stock losses, theft, transit damage, floods, and fire. Restaurants, cafes, and cloud kitchens are exposed to fire risks, food liability claims, employee accidents, and equipment damage.

Take a look at the table to understand the insurance required by different types of businesses.

How Much Does Business Insurance Cost?

There is no standard price for business insurance. Premiums vary based on factors such as business size, industry, turnover, asset value, employee count, coverage limits, location, claims history, and selected add-ons.

Basic covers may cost less than ₹500 a year, while a comprehensive insurance portfolio for a growing business can cost several lakhs and crores annually. The right policy should be chosen based on risk exposure, not just the lowest premium.

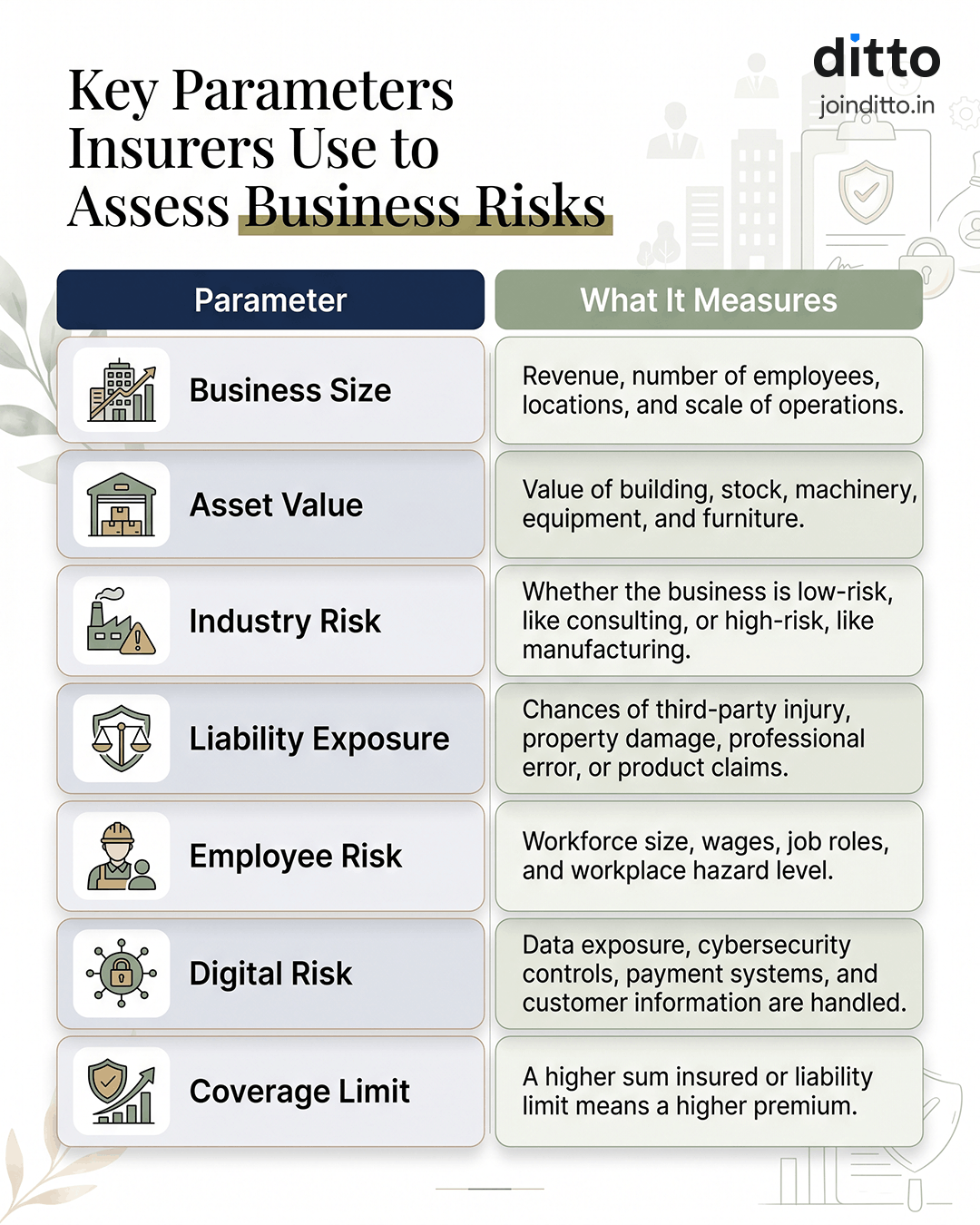

Business insurance is not priced randomly. Insurers usually assess a business across key risk parameters. Take a look at the infographic for a clear understanding of the parameters.

How to Choose the Right Business Insurance Policy?

- Assess Your Business Risks: Start with your business model, not the premium. A shop, factory, restaurant, clinic, SaaS company, or warehouse faces very different risks and insurance needs.

- Insure Assets Correctly: Cover buildings, machinery, equipment, and stock at realistic replacement values. Businesses with fluctuating inventory should consider floater or declaration-based stock cover.

- Consider Business Interruption: If a shutdown could affect profits, salaries, rent, EMIs, or customer commitments, add business interruption cover alongside property insurance.

- Do Not Ignore Liability: Public liability, product liability, professional indemnity, and cyber insurance can protect against costly legal claims.

- Review Exclusions Carefully: Check conditions related to disclosures, safety measures, stock storage, vacant premises, and claim reporting timelines.

Take Note: Businesses that employ physical labor should evaluate the need for Employee Compensation (Workmen's Compensation) and Group Personal Accident policies. If a business employs workers in scheduled occupations, such as factories or transport, it must provide compensation under the Employees’ Compensation Act, 1923. In this case, the workers’ compensation insurance shifts the legal liability to the insurer.

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 24,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

Business risks extend far beyond fire damage. A business can face losses from equipment breakdown, employee injuries, cyber incidents, theft, or prolonged operational disruptions. The right insurance strategy protects both your assets and your ability to continue operating in the event of unexpected events. Here’s a checklist before you purchase business insurance.

- Identify your top 3 business risks, including operational, financial, and liability exposures, before selecting any insurance cover.

- Confirm mandatory requirements, such as workers’ compensation, for scheduled occupations, and ensure the property is insured at reinstatement value, not market value.

- Review policy exclusions and business interruption cover carefully, then compare quotes from at least 3 IRDAI-licensed insurers or brokers before finalizing.

After securing adequate health cover among the best health insurance plans and life insurance from the best term insurance plans, you can consider other coverages. Business owners should also evaluate the protection needs of their premises, inventory, equipment, employees, and liabilities.

While Ditto's advisory services focus on health and term life insurance, business insurance remains an important pillar of long-term financial resilience.

Frequently Asked Questions

Last updated on: