Overview

Life insurance is no longer a niche product. In fact, according to the IRDAI annual report for FY 2024-25, India is the 10th-largest insurance market globally by premium volume, with life insurers collecting ₹8.86 lakh crore in premium income. But here is the gap: India’s life insurance penetration is still only 2.7%, lower than the global average of 3.0%.

This means many families either lack life cover or have insufficient coverage.

The core idea is simple. Life insurance helps replace your income if you are no longer around. It can help your family manage daily expenses, repay loans, protect long-term goals, and avoid making difficult money decisions during an already stressful time.

This guide discusses what life insurance is, how it works, the types of life insurance plans in India, what is covered and what is not, how much cover you may need, how claims work, and the tax benefits.

What Is Life Insurance and How Does It Work?

Life insurance works on a straightforward principle: you pay premiums, and the insurance company provides financial protection for your family.

Here's how the process typically works:

(1) You purchase a life insurance policy and choose a coverage amount (sum assured).

(2) You nominate one or more beneficiaries (nominees) who will receive the payout.

(3) You pay premiums monthly, quarterly, or annually through the insurer's payment options.

(4) If you pass away during the policy term, the insurance company pays the death benefit to your nominee after the claim is approved.

(5) Depending on the type of policy, there may also be maturity benefits, survival benefits, or investment-linked returns.

For example, suppose a person purchases a ₹2 crore term insurance policy. If they die during the policy term, their nominee receives ₹2 crore to help cover expenses such as household costs, loan repayments, children's education, and future financial needs.

Note: The policyholder is the person who buys and owns the policy. The life assured is the person whose life is covered. In many cases, both are the same person.

The nominee is the person who receives the payout if the life assured dies during the policy term.

Core Concepts in Life Insurance

Why Do You Need Life Insurance in India?

You need life insurance if someone depends on your income, unpaid work, or financial support.

That includes your spouse, children, parents, siblings, or anyone who would struggle financially if you were no longer around. Even if you are not the only earning member, your absence can still create a major financial gap.

Here is where life insurance helps:

Income Replacement

For most families, the biggest financial risk is the loss of the primary earning member. Life insurance helps replace that lost income and provides your dependents with financial support for years to come.

Protection Against Outstanding Loans

Many individuals have home, personal, education, or vehicle loans. If something happens to you, these liabilities don't disappear. Life insurance can ensure your family isn't burdened with repaying those debts.

Financial Security for Your Family

A life insurance payout can help your loved ones manage daily expenses, maintain their standard of living, and meet future financial commitments without compromising their goals.

Funding Long-Term Goals

Life insurance proceeds can support important milestones such as higher education, marriage expenses, a spouse's retirement planning, or care for aging parents.

Types of Life Insurance Plans in India

Understanding the different types of life insurance plans can help you choose a policy that aligns with your financial goals.

Term Insurance

Term insurance is the simplest and most affordable type of life insurance policy. It provides a death benefit if the policyholder passes away during the policy term. Since there is no savings or investment component, premiums remain relatively low while coverage remains high. For example, Axis Max Life Smart Term Plan Plus and HDFC Life Click2Protect Supreme Plus both make it to the list of the best term insurance plans in India.

Unit Linked Insurance Plans (ULIPs)

ULIPs combine life insurance and market-linked investments. A portion of your premium goes towards life cover, while the remaining amount is invested in equity, debt, or balanced funds. ULIPs can work for disciplined long-term investors, but they are not simple products. You must understand charges, fund options, sum assured limits, lock-in period, switching rules, and market risk before buying. Plan example: HDFC Sampoorn Nivesh Plus.

Endowment Plans

Endowment plans combine life insurance with guaranteed savings. If the life assured dies during the policy term, the nominee gets the death benefit. If the life assured survives the term, the policyholder receives a maturity benefit. The issue is that life cover is often much lower than a family actually needs, and the returns may be modest compared to those of an FD. Plan example: LIC Single Premium Endowment Plan.

Money-Back Plans

Money-back plans periodically pay a percentage of the sum assured plus bonuses during the policy term while continuing to provide life coverage. These plans appeal to individuals who prefer regular payouts rather than a lump-sum maturity benefit. However, the insurance coverage is still inadequate compared to that of a term plan. Plan example: LIC New Money Back Plan 20 Years.

Whole Life Insurance

Whole life insurance is a duration type, and all the above-mentioned plans can be sold as a whole-life option. It provides coverage for your entire lifetime, often up to age 99 or 100. In addition to the life cover, these plans may build a surrender value or provide bonuses over time. However, they tend to be significantly more expensive than term insurance. Plan example: ICICI Pru iProtect Smart Plus (Whole Life Option).

Child Plans

Child plans are designed around future expenses such as higher education. Many of these plans include a waiver of premium feature, in which future premiums may be waived if the parent dies, allowing the policy to continue toward the child’s goal. Plan example: SBI Life Smart Scholar. You can also check out our detailed guide on SBI Life child plans.

Annuity/Pension Plans

These plans help individuals build a retirement corpus and, in some cases, offer life insurance benefits. They are designed primarily to generate income during retirement rather than provide substantial life cover. Plan example: LIC Jeevan Akshay VII.

Key Takeaway: In addition to the above-mentioned plan types, there are group life insurance and credit life plans. However, for most working professionals, term insurance should come first. Once you have sufficient protection, you can plan investments separately through products designed for wealth creation, such as low-cost mutual funds, the Public Provident Fund (PPF), or Fixed Deposits (FDs).

Term Insurance Premiums

For this illustration, we’ve considered sample profiles of healthy, salaried, non-smoking individuals living in a tier-1 city such as Delhi (pincode: 110010) and covered them for a sum assured of ₹2 crore until age 65 (without first-year discounts). These premiums are indicative and can vary based on sum assured, age, health conditions, lifestyle choices, and underwriting decisions.

Talk to an expert

today and

find

the right

insurance for you.

What Does Life Insurance Cover?

A standard life insurance policy covers death from natural causes, illness, natural calamities, and accidents, subject to policy terms and claim assessment. In simple terms, if the life assured dies during the policy term and the claim is valid, the nominee receives the sum assured.

Note: Some term plans include a terminal illness benefit. This means the insurer pays the sum assured early if the life assured is diagnosed with a terminal illness, as defined in the policy wording.

If you’ve added additional riders to your policy, then the following are also covered:

Critical Illness Rider

A critical illness rider pays a fixed amount if the life assured is diagnosed with one of the listed critical illnesses to cover income loss, recovery expenses, and non-medical charges. But this does not mean every illness is covered. The illness must be listed in the policy document, meet the insurer’s definition, and satisfy conditions such as waiting period and survival period, wherever applicable. For example, if a plan covers specific types and stages of cancer, a very early-stage diagnosis may not always qualify. Always check the rider wording.

Accidental Total and Permanent Disability Rider

This rider helps if the life assured suffers a serious accident that leads to total and permanent disability. Depending on the rider, the insurer may pay a lump sum, waive future premiums, or provide another defined benefit. But again, the disability must match the policy definition. A temporary injury or partial disability may not qualify unless the rider specifically covers it.

Waiver of Premium Rider

A waiver of premium rider waives future premiums if a specified event occurs, such as disability, critical illness, or death of the premium-paying parent in a child plan. This helps the policy continue even when the family cannot pay future premiums.

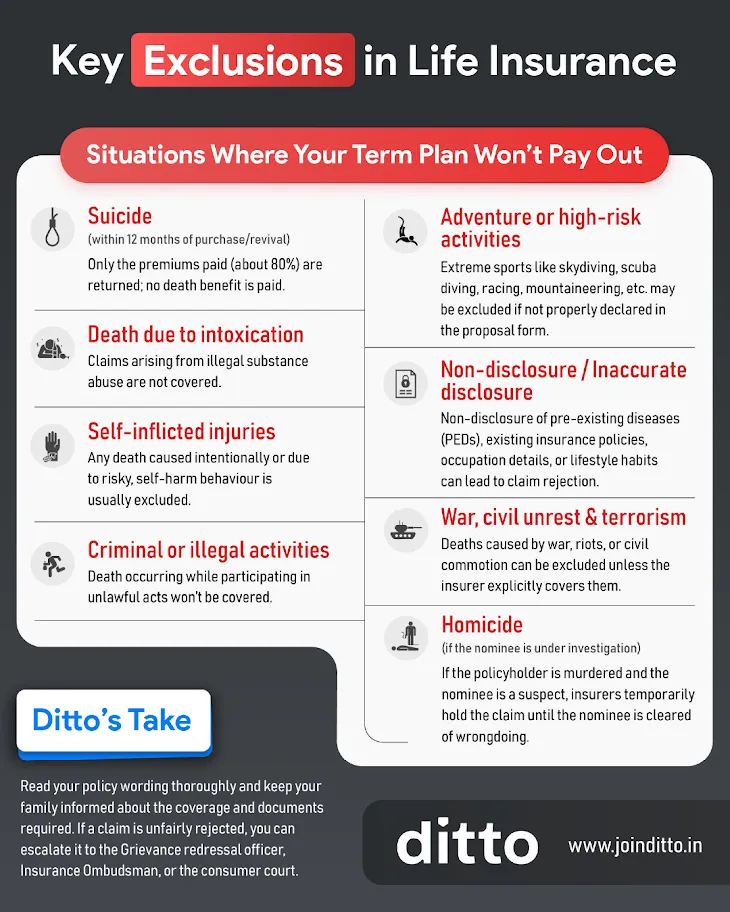

What Is Not Covered in a Life Insurance Policy?

Since exclusions can vary across insurers and profiles, reviewing the policy wording carefully is always recommended.

How Much Life Insurance Cover Do You Need?

At Ditto, we recommend that people account for

- Family’s monthly expenses

- Existing loans and liabilities

- Future goals, such as children’s education

- Inflation

For example, if you are 25, your family needs ₹50,000 a month, you have a ₹60 lakh home loan, and you want to set aside money for your child’s education, a ₹1 crore policy may seem large, but it may not be enough. Once you add future expenses and inflation, you’ll need something around ₹3 crore.

This is why, instead of relying solely on generic rules, you can use the term insurance cover calculator available on Ditto’s website to provide a more personalized estimate.

How to File a Life Insurance Claim?

Step 1: Inform the Insurer

The nominee should inform the insurance company as soon as possible after the life assured’s death.

Step 2: Submit Required Documents

The documents required for term insurance include a claim form, a death certificate, proof of identity for the nominee (Aadhar, PAN, etc.), the policy document, and KYC details.

Step 3: Claim Assessment

The insurer reviews the documents, the policy status, the disclosures made at the time of purchase, and the cause of death. According to IRDAI guidelines, insurers should take a maximum of 15 days for non-investigative and 45 days for claims needing investigation.

Step 4: Payout

If the claim is approved, the death benefit is paid to the nominee’s registered bank account.

As per the IRDAI report, in FY 2024-25, individual life insurance death claims had a paid ratio of 97.82% by number of policies. This does not mean every claim is guaranteed, but it does show that valid claims are regularly paid when documentation and disclosures are in order.

If you bought your policy through Ditto Insurance, you can reach out to us for claims assistance.

Things to Keep in Mind Before Buying Life Insurance

Buy Early

Premiums increase with age, so purchasing coverage earlier can help lock in lower rates while you’re still healthy.

Disclose Everything Honestly

Mention smoking, alcohol use, medical history (self + family), occupation, income, and existing insurance accurately. Honest disclosure is one of the strongest ways to protect your family’s future claim.

Choose Adequate Coverage

A low premium can look attractive, but a low cover defeats the purpose of life insurance. The goal is not to buy the cheapest policy, but to buy enough cover at a fair price.

Do Not Mix Every Goal Into One Product

Insurance and investment are different needs. A term plan protects your family. Investments help you grow wealth. Combining both may work in some cases, but it can also make the product expensive and harder to understand.

Check the Insurer’s Metrics

Look at claim settlement ratio, amount settlement ratio, solvency ratio, complaint numbers, and business scale. Do not choose only based on the premium. Some insurers on the list of the best term insurance companies in India include Axis Max Life, HDFC Life, and ICICI Prudential.

Read the Policy Documents

Before buying, check the policy wording, benefit illustration, Customer Information Sheet (CIS), exclusions, rider terms, premium payment terms, and surrender rules.

Key Terms to Understand Before Buying Life Insurance

- Free Look Period

Life insurance policies come with a 30-day free-look period from the date you receive the policy document. During this time, you can review the policy terms and cancel it if it does not meet your expectations, subject to applicable deductions.

- Grace Period for Premium Payments

If you miss a premium payment, insurers provide a grace period before the policy lapses. Monthly premium policies have a 15-day grace period, while policies with quarterly, half-yearly, or annual premium modes receive a 30-day grace period.

- Protection Under Section 45

A life insurance policy cannot be challenged by the insurer after three years from the relevant policy date, except under specific conditions, such as intentional fraud, as permitted by the 3-Year Clause in term insurance under Section 45 of the Insurance Act.

- Customer Information Sheet (CIS)

Insurers are required to provide a CIS that explains the policy's key features in simple and easy-to-understand language. It includes details about benefits, exclusions, policy terms, and the grievance redressal process to help customers make informed decisions.

Term Insurance vs Other Life Insurance Products: Which One to Buy First?

For most individuals, term insurance should be the first life insurance product they purchase.

Here's why:

- It provides the highest coverage at the lowest cost.

- It focuses entirely on income replacement.

- It allows you to keep insurance and investments separate.

- It is easier to understand than savings or market-linked plans.

- It protects your family without requiring a large financial commitment.

Once adequate term insurance is in place, you can consider other financial products based on your savings, investment, retirement, or wealth-creation goals. But do not start with an endowment plan or ULIP if your core need is family protection. In most cases, you will end up paying more premiums for much lower life cover.

Tax Benefits Under Life Insurance in India

The tax benefits in India include:

Section 80C (Now Renamed to Section 123)

You can claim deductions up to ₹1.5 lakh per financial year on premiums paid for yourself, your spouse, and your children (under the old regime). For policies issued after April 1, 2012, the premium must not exceed 10% of the sum assured (or 20% for policies issued before this date).

Section 80D (Now Renamed to Section 126)

If your life insurance policy includes health or critical illness-based riders, the premium paid for these riders can be deducted up to ₹25,000 (or ₹50,000 for senior citizens) under the old regime.

Section 10(10D) (Now Renamed to Section 11 [Schedule II])

The amount paid to the nominee upon the policyholder’s death is 100% tax-free. The payouts received at the end of the policy term are also tax-exempt, provided that the premium doesn’t exceed 10% of the sum assured in any of the policy years.

Note: For life insurance policies (excluding ULIPs) issued after April 1, 2023, if the aggregate annual premium exceeds ₹5 lakh, the maturity proceeds are fully taxable. For ULIPs issued on or after February 1, 2021, the maturity or surrender proceeds are tax-exempt only if the aggregate annual premium doesn’t exceed ₹2.5 lakh across all ULIPs in any of the previous years.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 24,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

Life insurance is one of the most important financial products you can buy if your family depends on you. But the type of life insurance you choose matters.

If your main goal is income replacement, start with term insurance. It is simple and cost-effective, providing your family with the highest level of protection for the premium paid. Once that protection is in place, you can plan investments, savings, retirement, or legacy goals separately.

The best life insurance policy is not the one with the fanciest benefits. It is the one that gives you peace of mind and your family enough money, at the right time, without unnecessary complexity.

Frequently Asked Questions

Customer Reviews

Last updated on: