Once upon a time, life insurance in India meant just two things: LIC’s familiar jingle playing on television and an agent who somehow always knew when you’d just received your salary. Choices were limited, paperwork was endless, and most people bought policies without really knowing what they were signing up for.

Those days are behind us. Today, India’s insurance market is crowded with digital-first insurers, dozens of policy variants, and smarter, more transparent products. In the middle of all this choice sits one important question that almost every buyer eventually faces: term insurance vs life insurance.

This guide breaks down life insurance vs term insurance in practical terms, how they work, what they cost, what they pay out, and who they truly make sense for.

What is Term Insurance?

Key features of term insurance include:

- High Cover at Low Premiums: Often the cheapest way to get ₹50 lakh–₹5 crore of protection. Calculate your ideal term insurance coverage here.

- Fixed Tenure: Typically 20–40 years or cover till age 60–80 (sometimes 99).

- No Investment Element: Premiums only pay for risk coverage.

- Clear Claim Triggers: Death and, in some plans, terminal illness.

- Tax Benefits: Premiums may qualify under Section 80C (old regime) and death benefits are tax-free under Section 10(10D).

How Does Term Insurance Work?

A term plan follows a simple structure:

- You choose the sum assured, policy term, and premium payment mode.

- The insurer evaluates your age, income, and health through underwriting.

- You pay regular premiums to keep the policy active.

- If death occurs during the policy term, the nominee receives the payout.

- If you survive the term, the policy ends with no payout (unless you chose a return-of-premium plan).

This simplicity is why term insurance is often called the purest form of life cover in the term plan vs life insurance comparison.

Types of Term Insurance Plans in India

Indian insurers offer several variants of term plans to suit different needs:

- Level Term Insurance: Fixed cover throughout the policy term. Ideal for income replacement and family security. Examples include ICICI Prudential iProtect Smart Plus and Bajaj Life eTouch II.

- Increasing Term Insurance: Cover increases periodically to offset inflation and rising responsibilities. HDFC Life Click2Protect Supreme Plus is an excellent example here.

- Decreasing Term Insurance: Cover reduces over time, usually aligned with loans like home loans. The best example of a decreasing term plan is the HDFC Life Click2Protect Supreme Plus (Life Goal variant).

- Return of Premium Term Insurance (TROP): Refunds the base premiums on survival, but costs 50–100% more than regular plans. All major life insurers offer the return of premium option as a variant of their flagship term plans (e.g., Axis Max Life and Tata AIA).

- Whole Life Term Insurance: Coverage till age 99 or 100, useful for legacy planning. Tata AIA Maha Raksha Supreme Select is an excellent example of a whole life term insurance plan.

- Group Term Insurance: Employer or bank-provided cover with limited flexibility and lower sums assured.

- Joint Term Insurance: One policy covering both spouses, usually structured as a first-death payout, but variants exist (e.g., Aditya Birla DigiShield).

- Zero-Cost (Special Exit) Plans: Allow exit at a fixed age with a premium refund. Offered by select insurers only.

- Term Insurance for Housewives: Cover linked to spouse’s income or policy, usually capped at ₹1–2 crore.

Note

Who Should Buy Term Insurance?

Term insurance is suitable for:

- Salaried and self-employed individuals

- People with home or personal loans

- Parents with young children

- Business owners

- Anyone whose family depends on their income

If someone would struggle financially in your absence, a term plan is usually the smartest choice in the term vs life insurance decision.

Advantages and Disadvantages of Term Insurance

Talk to an expert

today and

find

the right

insurance for you.

What is Life Insurance?

In India, life insurance products fall into two broad groups:

- Pure Protection Plans, such as term insurance, which only cover the risk of death.

- Protection‑Plus‑Savings Plans, such as endowment, money‑back, ULIPs, and whole‑life policies, which combine life cover with returns or investments.

This structural difference is at the heart of the life insurance vs term insurance debate. Life insurance policies are built around a few core elements:

- Life Assured: The person whose life is insured

- Policyholder: The person who buys the policy and pays the premiums

- Nominee: The person who receives the benefit on death (usually spouse, children, or parents)

- Sum assured: The guaranteed payout amount

- Policy Term: Duration of coverage

- Premium: Amount paid to keep the policy active

- Death Benefit: Payout if death occurs during the term

- Maturity Benefit: Payout on survival (if applicable)

- Surrender / Paid‑up value: Amount received or reduced cover if premiums are discontinued in savings‑based plans

Recent IRDAI rules on Guaranteed Surrender Value (GSV) and Special Surrender Value (SSV) have made exits from traditional life insurance plans more transparent and predictable.

How Do Life Insurance Policies Work?

Life insurance follows a longer‑term structure compared to term plans:

- You choose a policy type (endowment, ULIP, whole life, etc.), sum assured, and policy term.

- You pay premiums for a fixed period (premium payment term)or for life.

- A portion of your premium goes toward life cover, and the rest may go into savings or investments (depending on the plan).

- If death occurs during the policy term, the nominee receives the death benefit.

- If you survive, you may receive a maturity amount, bonuses, or fund value.

Unlike term plans, many life insurance policies also build cash value, which allows partial withdrawals, loans, or surrender, an important distinction in the term plan vs life insurance comparison.

Types of Life Insurance Plans Explained

Here are the most common types of life insurance policies in India:

Whole Life Insurance Plan

Whole life insurance plans provides coverage for your entire lifetime (usually up to age 99 or 100). You can choose regular‑pay, limited‑pay, or single‑premium options, and select participating or non‑participating variants. While it offers lifelong protection and stable returns, premiums are significantly higher than term insurance.

Endowment Assurance Plan

Endowment assurance plans combine insurance with savings. You receive a lump sum on maturity if you survive, or the death benefit if you don’t. These plans offer safety but usually provide lower coverage, limited flexibility, and modest long‑term returns.

Money‑Back Plan

Pays periodic amounts during the policy term and the remaining sum assured at maturity. The full death benefit is still paid even if some payouts have already been received. However, money-back plans tend to deliver low returns and fragmented protection.

Child Insurance Plans

Designed to fund a child’s education. Child insurance plans are available as ULIPs, endowment, or money‑back variants. Payouts are timed around key education milestones such as age 18 or college years.

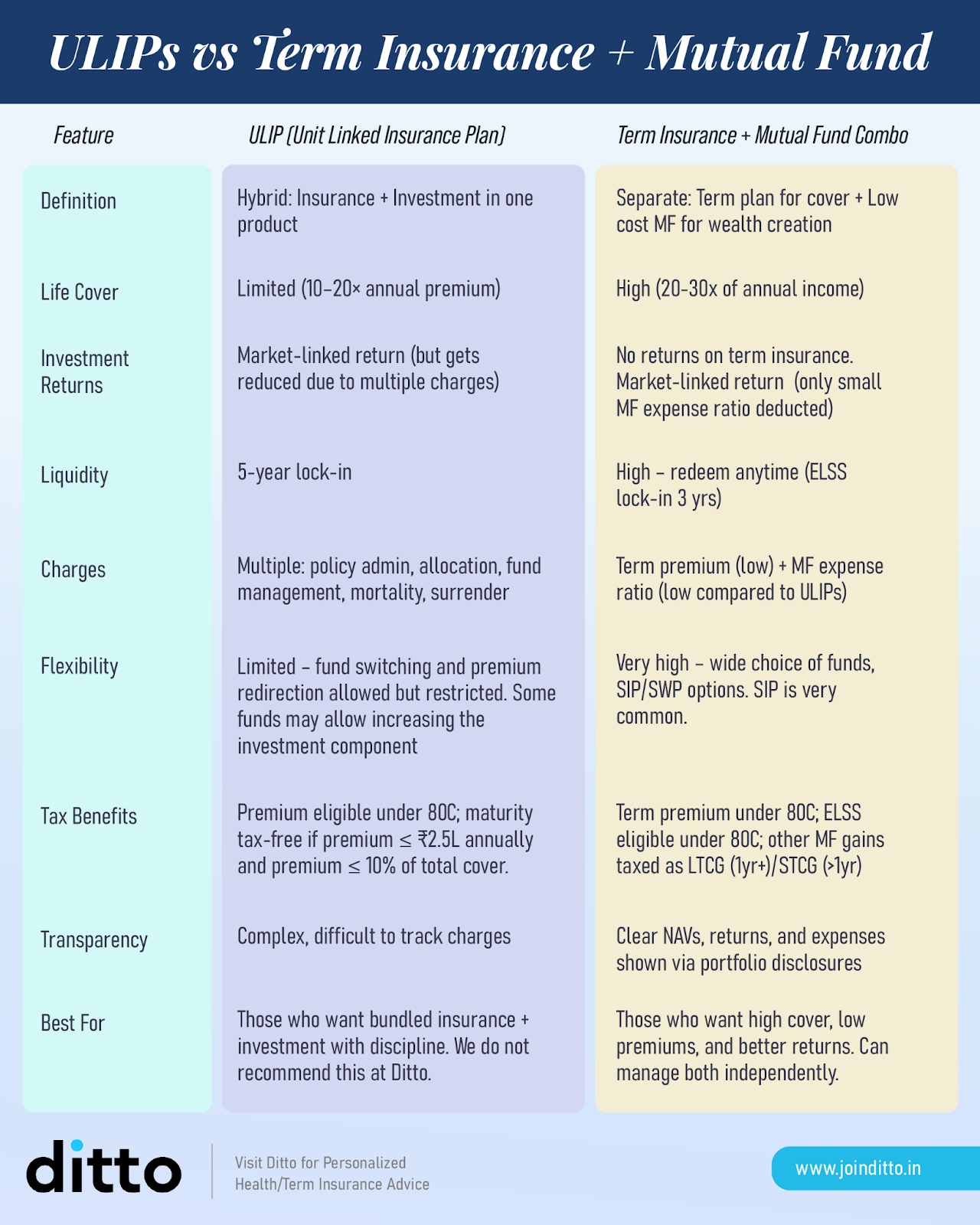

Unit‑Linked Insurance Plans (ULIPs)

Split your premium between life cover and market investments (equity/debt funds). While ULIPs offer tax benefits and fund‑switching, multiple charges, market risk, and a 5‑year lock‑in often reduce net returns. Many investors find a term insurance + mutual fund combination more efficient. Let’s take a quick look at how it functions:

Who Should Consider Life Insurance?

Life insurance plans may be suitable for:

- People who want forced long‑term savings

- Conservative investors seeking guaranteed or stable returns

- Individuals uncomfortable managing investments themselves

- Those who want lifelong coverage or estate‑planning tools

- Individuals not eligible for term plans due to medical or financial eligibility reasons.

However, for most working professionals whose primary goal is income protection, term insurance remains the more efficient choice in the term vs life insurance decision.

Many financial planners, therefore, recommend buying term insurance for protection and investing separately for wealth creation. This approach offers higher coverage, lower costs, and better long‑term flexibility than bundling both into a single life insurance product.

Difference Between Term Insurance and Life Insurance

Ditto’s Recommended Term Plans (2026)

Before we discuss the list, here’s how we decide what plans to feature.

At Ditto, every term plan goes through our six-point evaluation framework. It doesn’t mean these are the only good plans, but that they stand out after being scored across all six pillars.

You can learn more about how we evaluate term insurance plans here.

If you want to know about the best term insurance plans in India in 2026 in detail, refer to the linked article.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or WhatsApp us now!

Ditto’s Take: Term vs Life Insurance

At Ditto, we usually recommend pure term insurance as the most efficient way to protect your family when comparing term insurance vs life insurance. It gives you a large cover at a very low premium because it does not mix insurance with investment.

Traditional plans like endowment, money-back, or ULIPs offer limited cover and modest returns, which rarely justify their higher costs or long lock-ins in the life insurance vs term insurance debate.

When you keep protection and investment separate, you make better decisions. Use term insurance for safety. Use mutual funds, PPF, or FDs for growth. This approach offers more flexibility, better returns, and clearer outcomes than a bundled product in the term plan vs life insurance comparison. For most Indians with dependents or loans, term insurance remains the cleanest and most transparent protection option in the broader term vs life insurance choice.

Final Thoughts

IRDAI’s classifications have made it easier to understand how term insurance vs life insurance plans work. Term insurance is always non-linked and non-participating, offering pure life cover.

Savings and endowment plans are non-linked and may be par (participating in insurer’s profits) or non-par, providing protection plus returns. ULIPs are always linked (to the markets) and non-participating, combining life cover with market investments. Knowing these basics helps you choose the right plan for your needs.

Still unsure between a life and term plan? Book a free call with us and let our experts guide you to make an informed decision.

Quick Note

Frequently Asked Questions

Customer Reviews

Last updated on: