Quick Overview

What is term insurance, exactly? It is a contract between you and an insurance company. You pay a fixed premium every year for a chosen number of years (the policy term). If you pass away during that term, the insurer pays a lump sum to your nominee. If you survive the term, the policy ends; you receive nothing back.

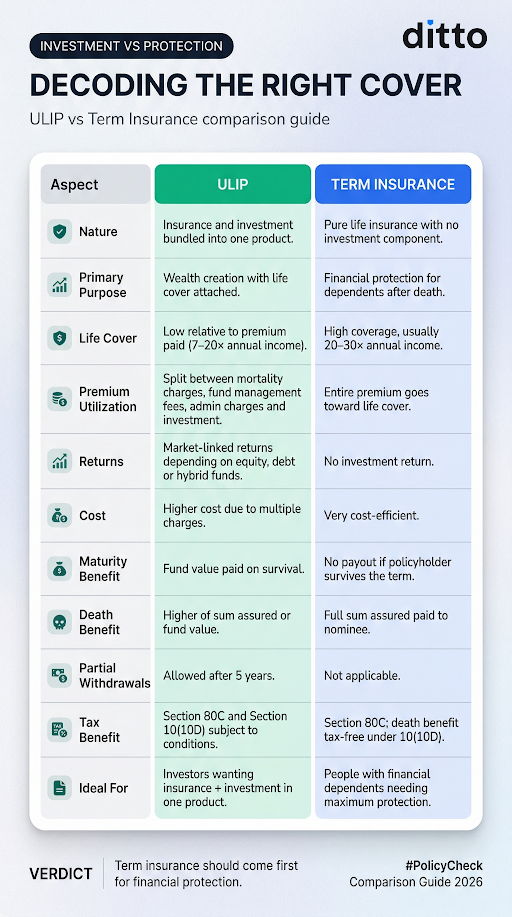

This is the defining feature that separates term insurance from other life insurance products like ULIPs or endowment plans, which bundle investment with insurance. A term plan keeps things simple: you are paying purely for life cover.

How Term Insurance Works

The paragraphs above already paint quite a clear picture of how term insurance works. If you want a more in-depth look at it, you can refer to our how term insurance works guide.

Key Features and Benefits of a Term Insurance Plan

- Low Premiums, High Cover: A healthy 25-year-old can get ₹1 crore of life cover for roughly ₹9,000–₹10,000 per year. The same cover purchased at age 40 can cost two to three times more, which is why buying early matters.

- Fixed Premium for the Entire Term: Your premium is locked in at the time of purchase. It does not increase as you age or if your health changes over the policy tenure.

- Large, Tax-Free Death Benefit: The sum assured paid to your nominee is fully tax-free under Section 10(10D) of the Income Tax Act. Premiums paid are also eligible for deductions under Section 80C (Old Regime).

- Flexible Policy Term: You can choose a term ranging from 10 to 40 years, or even up to age 85 or 99 (whole life term plans). Ditto recommends covering yourself until at least age 60–70 based on your dependents' age and liability periods.

- Add-On Riders for Extra Protection: You can enhance your base term plan with riders such as critical illness cover, waiver of premium, and disability income, for a small additional premium.

- No Survival Benefit: This is actually a feature, not a drawback. Because there is no maturity payout, the insurer can offer much higher cover at lower premiums. If you want your premiums back, look at a Return of Premium (ROP) variant, though this comes at a higher cost (60-100% higher).

Who Should Buy Term Insurance & How Much Cover Do You Need?

Not everyone buys term insurance when they should, and many who do buy it end up with the wrong cover amount. Getting both of these right is what makes the difference between a policy that genuinely protects your family and one that just ticks a box.

Who Needs Term Insurance?

The short answer: anyone who has financial dependents. This includes:

- Salaried professionals whose income supports their family

- Self-employed individuals and business owners

- If you are young and healthy, you need it even more because premiums are at their lowest

- Parents with young children or dependent parents

- Anyone with a home loan, car loan, or significant financial liability

How Much Cover Do You Need?

A commonly used rule of thumb is 10x to 20x your annual income. For instance, if you earn ₹8 lakh per year, an ₹80 lakh to ₹1.6 crore cover is a reasonable starting range.

A more precise method is the Human Life Value (HLV) approach, which estimates the present value of your future earnings, factoring in your age, income, expenses, liabilities, and existing savings.

If you want a simple way to figure out your ideal cover, use our term insurance cover calculator.

Sample Premiums of A Few Term Insurance Plans

Profile Considered: Annual premiums are based on a ₹1 crore sum assured, with coverage up to age 70, for a non-smoking male, residing in Delhi, with no added riders or 1st year or online discounts. The above-mentioned premiums are illustrative in nature and can vary based on medical history and insurer underwriting.

Term Insurance vs Other Products

Here’s an example:

How to Choose the Right Term Insurance Plan in India

Think in two layers: insurer quality and policy features. At the insurer level, look for a 3-year average CSR above 97%, a strong ASR (to gauge how well large claims are paid), a solvency ratio comfortably above 1.5x, and low complaint volumes as a sign of smoother claim experience.

At the policy level, choose a sum assured of 10–25× your annual income (adjusted for loans and dependents), a tenure up to 65–70, and add riders like WOP, critical illness, or disability only if relevant. Also look for useful features such as terminal illness benefits, life-stage cover increases, and zero-cost exit options. Check out this term insurance purchase checklist for more details. One more thing: buy early. Buying early isn’t just cheaper; it locks in your insurability.

For a detailed breakdown of every factor, including insurer comparisons and rider-by-rider analysis, read the things to consider before buying a term insurance plan.

To make things even simpler for you, we have meticulously examined and listed the best term insurance plans in India in 2026.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Conclusion

Term insurance is not a complex product, and that is exactly why it is the most important one. It is a financial safety net that ensures your family does not have to compromise on their future if you are no longer there to provide for them.

But it’s also something more powerful than most people realise.

Term insurance is arguably the highest-leverage financial instrument available to an individual. For instance, a 30-year-old paying around ₹13,000 a year for a ₹1 crore cover is effectively creating a 769:1 protection ratio in the very first year. Even over 30–35 years, the total premiums paid are a fraction of the coverage, making it one of the most efficient ways to secure your family’s financial future.

The best time to buy term insurance was yesterday. The next best time is today. Compare plans, choose the right cover amount, and lock in your premium while you are young and healthy.

Frequently Asked Questions

Last updated on: