Overview

If you're exploring an SBI Life ₹5 crore term insurance plan, the two key options are Smart Shield Plus and Smart Shield Premier.

Both plans support high sum assureds, subject to underwriting. But are they worth it, or should you consider other insurers?

In this article, we'll explain SBI Life's ₹5 crore term insurance options, compare Smart Shield Plus and Smart Shield Premier, review premiums and eligibility, discuss key features and riders, analyze SBI Life's claim metrics, and help you decide whether it's the right insurer for your needs.

What Is SBI Life ₹5 Crore Term Insurance?

An SBI Life ₹5 crore term insurance plan is a pure protection policy that pays ₹5 crore to your nominee if the policyholder passes away during the policy term. It does not provide a maturity benefit if the policyholder survives the policy term.

A ₹5 crore cover is usually considered by:

- High-income earners (insurers generally allow maximum coverage of up to 20–30 times annual income, so a ₹5 crore cover typically requires an annual income of at least ₹17–₹25 lakh).

- Individuals looking to replace their income for dependents.

- Young parents are seeking long-term financial protection for their children.

- Individuals with large financial liabilities.

However, ₹5 crore may not be the right cover amount for everyone. Before choosing a sum assured, use Ditto's term insurance cover calculator to estimate your coverage needs based on your expenses, liabilities, future goals, and dependents. This can help avoid both underinsurance and overinsurance.

SBI Life Plans That Offer ₹5 Crore Cover

Key Takeaway: Choose SBI Life Smart Shield Plus if you want flexibility through optional increasing cover, life-event-based cover increases, or whole life coverage. Choose SBI Life Smart Shield Premier if you need a large cover amount immediately and prefer a plan specifically designed for high-sum-assured requirements.

Key Features, Riders, and Add-Ons

- Flexible Claim Payout Options: Both plans offer claim payouts as a lump sum, monthly income, or a combination of both. We generally prefer the lump sum option, as it provides greater flexibility to repay liabilities, invest, or meet future financial needs.

- Better Half Benefit (Available Under SBI Life Smart Shield Plus): If the life assured passes away during the policy term, a separate life cover is activated for the spouse. The spouse's cover is limited to ₹25 lakh or 50% of the base sum assured, whichever is lower. While useful as an add-on benefit, those requiring substantial protection for their spouse will be better served by purchasing a separate term insurance policy.

- Future Proofing Benefit (Available Under SBI Life Smart Shield Plus): This feature allows you to increase your life cover without fresh medical underwriting following specified life events, subject to policy conditions. The cover can be increased by 50% of the original sum assured on marriage, 25% on the birth/adoption of the first child, 25% on the birth/adoption of the second child, and 50% on the purchase of a house. The increase attracts an additional premium and must be requested within 6 months of the event.

- Accident Benefit Riders: SBI Life primarily offers accident-related riders with these plans. The Accidental Death Benefit Rider provides an additional payout if death occurs due to an accident, while the Accidental Partial Permanent Disability Rider pays a specified percentage of the rider's sum assured for covered accidental disabilities. The accidental death rider is available up to ₹2 crore and the disability rider up to ₹1.5 crore, subject to underwriting approval.

Eligibility and Premium Illustration

SBI Life ₹5 Crore Plan Eligibility

Note: For a ₹5 crore cover, SBI Life may conduct additional underwriting and assess factors such as your annual income, financial stability, existing life insurance coverage, medical history, tobacco usage, and occupational risk before approving the policy.

SBI Term Insurance ₹5 Crore Premium

Note: Indicative annual premiums for healthy, non-smoking males with a ₹5 crore cover up to age 65 (pincode 110011). Actual premiums may vary based on underwriting, medical history, occupation, policy options, and rider selection.

One important point is that premiums do not increase in proportion to coverage. A ₹5 crore term plan will not cost five times as much as a ₹1 crore plan. Most insurers, including SBI Life, offer pricing efficiencies at higher coverage amounts, effectively providing a bulk discount on larger sum assured. As a result, the cost per crore of coverage decreases as the sum assured increases.

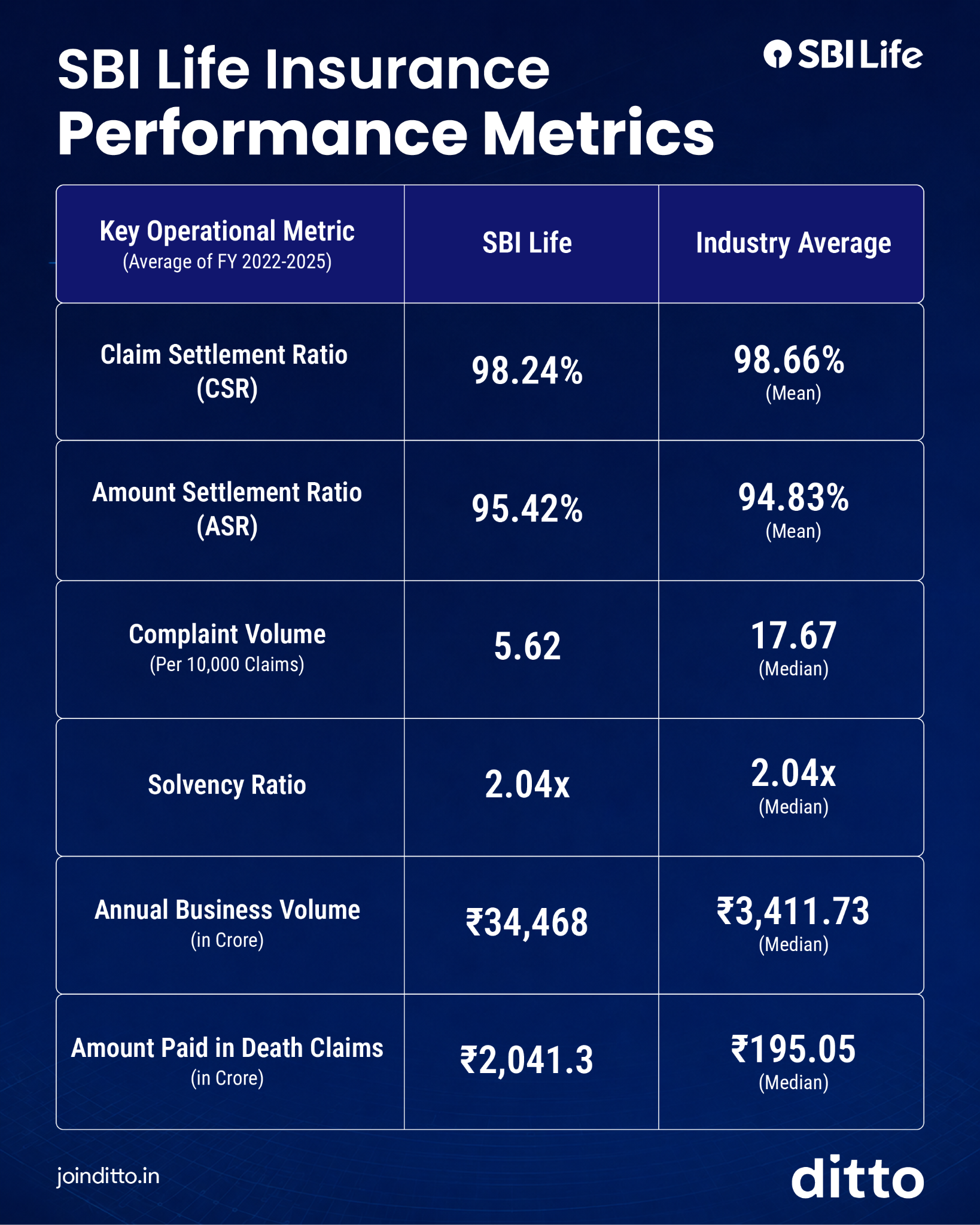

SBI Life as an Insurer: Claim Settlement and Key Metrics

Key Insights

- SBI Life's claim settlement ratio is strong and has improved consistently over recent years.

- Its Amount Settlement Ratio (ASR) is above the industry average, indicating fair claim payouts across ticket sizes.

- Complaint volumes are lower than the industry median, suggesting a relatively smooth customer experience.

- The solvency ratio remains well above the IRDAI-mandated 1.5x level, reflecting strong financial health.

- SBI Life's business scale is significantly larger than the industry median, highlighting its market presence.

Note: These metrics reflect SBI Life's overall performance and are not specific to Smart Shield Plus, Smart Shield Premier, or any individual product. At Ditto, we use 3-year averages for key operational metrics to reduce the impact of short-term fluctuations.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat over WhatsApp with our advisors.

Ditto’s Take: Who Should Choose SBI Life for a ₹5 Crore Term Cover?

SBI Life is India's second-largest life insurer after LIC and offers two relevant options for a ₹5 crore cover: Smart Shield Plus and Smart Shield Premier. Of the two, Smart Shield Premier is generally better suited for high-income individuals seeking larger coverage, as it is designed for high sum assured requirements and can be more cost-effective at higher coverage levels.

However, SBI Life's term plans are not the most feature-rich in the market. They do not offer features such as premium break options, health management services, or instant claim payouts. Rider options are also limited, with no critical illness rider or waiver of premium rider available.

If you prioritize insurer size, brand reputation, and a straightforward term plan, SBI Life is a strong option. If you want broader features and rider choices, compare it with HDFC Life, Axis Max Life, ICICI Prudential Life, and Bajaj Life before buying, or check out our detailed guide comparing the best life insurance companies in India.

Frequently Asked Questions

Last updated on: