Quick Overview

SBI term insurance plan with return of premium (RoP) is designed for people who want life insurance coverage along with the reassurance of getting their premiums back if they survive the policy term. Unlike regular, pure term insurance, where no money is returned at maturity, RoP plans refund 100% of the total premiums paid (excluding taxes and rider charges) if the policyholder outlives the term.

SBI Life Insurance, backed by the trust of the State Bank of India and BNP Paribas Cardif, offers multiple term insurance plans with a return-of-premium feature across different coverage levels and policy terms. These plans are usually chosen by individuals who find the “no maturity benefit” aspect of regular term insurance psychologically difficult to accept, even though it is more cost-effective.

That said, while the concept sounds attractive, return-of-premium plans come with higher premiums and trade-offs that need careful evaluation before buying.

Features of the SBI Term Insurance Plan With Return of Premium

An SBI term insurance plan with return of premium typically includes the following features:

- Life cover throughout the policy term, ensuring financial protection for your family in case of death

- 100% refund of total premiums paid on survival till maturity (excluding GST, rider charges, and extra premiums, if any)

- Flexible policy terms, usually ranging from 10 to 30 years, depending on the plan

- Multiple premium payment options, such as regular pay or limited pay

- Optional accidental benefit riders are available in most plans

Note: RoP plans are not savings or investment products. The refunded amount does not include any interest or inflation-adjusted growth; it is simply the sum of premiums paid over the years.

SBI Term Insurance With Return of Premium Plans

Eligibility Criteria for SBI Term Insurance With Return of Premium Plans

Eligibility varies slightly by product, but broadly:

- Entry Age: Starts from 18 years

- Maximum Entry Age: Ranges between 50 and 60 years, depending on the plan

- Maximum Maturity Age: Usually capped at 65–75 years

- Policy Term: Typically between 10 and 30 years

Medical underwriting may apply based on age, sum assured, and health disclosures.

SBI Life’s Operational Metrics

SBI Term Insurance With Return of Premium – Premium Details

To put the cost difference into perspective, here’s a comparison with a regular term plan from SBI Life for the same profile.

Note: The above illustrations are based on a 30-year-old, healthy, non-smoking male who opts for regular (yearly) premium payments and a 30-year policy term for a ₹1 crore cover.

For the same 30-year-old, non-smoking male with a ₹1 crore cover over 30 years, the Return of Premium option costs about 2.35 times more than a regular term plan. This translates to roughly ₹15,206 extra per year (around 135% higher) and about ₹4.56 lakh more in total premiums over 30 years.

Since the maturity benefit only refunds the premiums paid, without any interest or growth, the real value of this “return” is largely eroded by inflation and the missed opportunity to invest the premium difference.

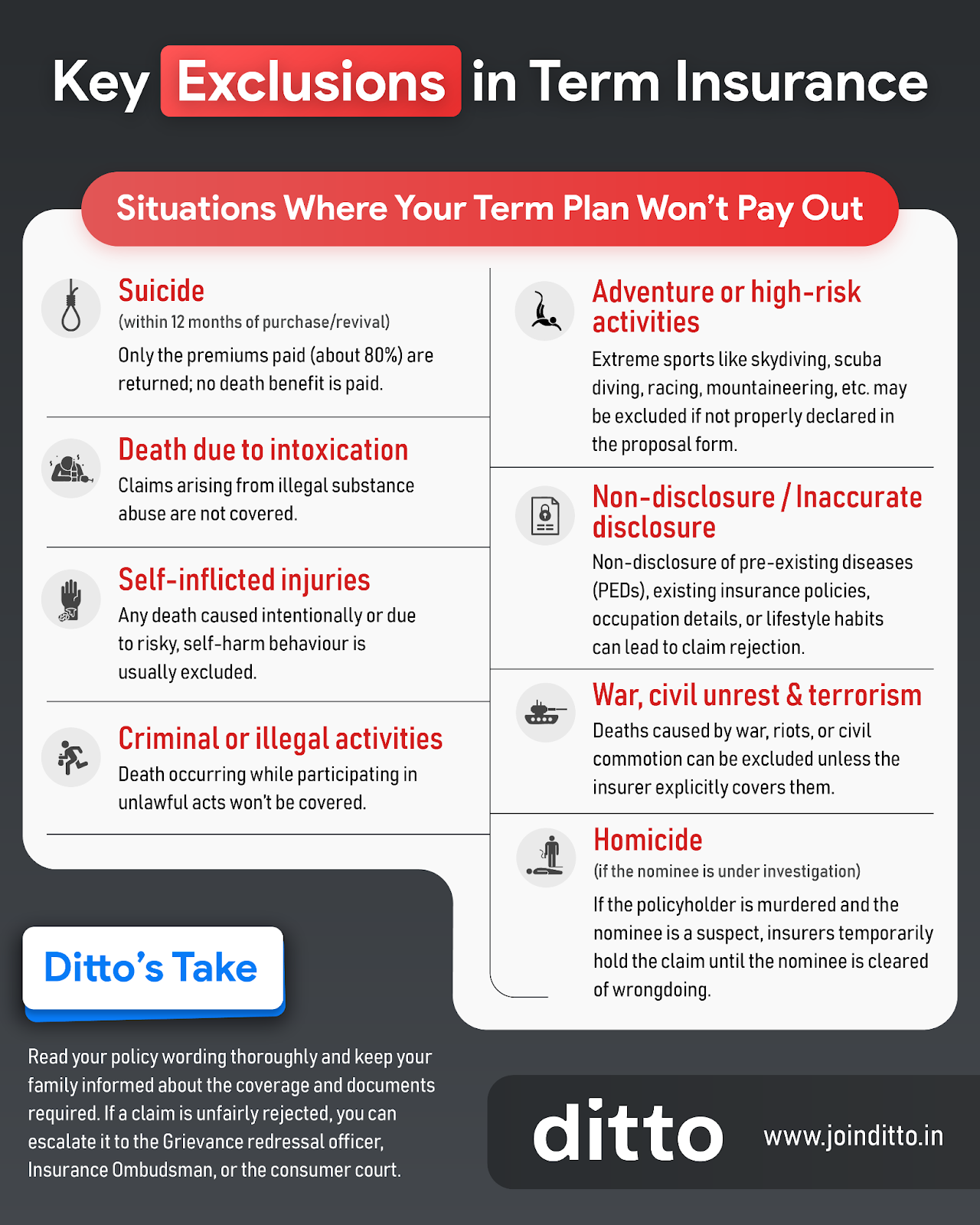

What Is Covered and Not Covered Under the SBI Term Insurance Plan With RoP?

What Is Covered: Term insurance plans cover death due to natural causes (for example, cardiac arrest), death resulting from terminal or critical illness, death caused by natural disasters or pandemics, and accidental death. It is recommended to check the specific policy wordings for exact inclusions.

What Is Not Covered: The key exclusions are highlighted in the infographic below and are generally applicable across term insurance products.

SBI Term Insurance With Return of Premium vs Regular Term Insurance

Pros and Cons of SBI Term Insurance With Return of Premium

Pros

- Offers psychological comfort by refunding premiums if the policyholder survives the policy term.

- Has a simple and easy-to-understand structure with a clearly defined maturity benefit.

- Backed by SBI Life, a well-established insurer with strong brand trust and a wide distribution network.

Cons

- Premiums are significantly higher compared to regular term insurance plans offering similar coverage.

- The refunded amount does not earn any interest and loses value over time due to inflation.

- Provides limited rider options and fewer modern features compared to many newer term plans in the market.

- Delivers lower overall value for money when the goal is long-term, cost-effective life insurance protection.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Venkatesh below love us:

- No Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Ditto’s Take

At Ditto, we generally recommend separating insurance and investments. While an SBI term insurance plan with return of premium may offer emotional comfort, the higher premiums, lack of inflation-adjusted returns, and relatively low sum assured options in many SBI RoP plans make them less efficient for most buyers.

SBI Life is a trusted insurer with strong claim metrics and a wide RoP portfolio, but these plans are structurally expensive and miss several modern features. For most people, a regular term plan with higher coverage, paired with disciplined investing through mutual funds or SIPs, offers better overall value. Always check current plan availability before deciding.

Note: SBI is not a partner insurer of Ditto. The information outlined in this article is sourced directly from the insurer’s website and other publicly available sources.

Frequently Asked Questions

Last updated on: