Quick Overview

When it comes to term insurance in India, brand trust matters, and few brands carry as much legacy as LIC, the Life Insurance Corporation of India. Established in 1956, LIC has operated at a massive scale and achieved an annual business volume of ₹2,27,169 crore (FY 22-25).

Building on this long-standing reputation, LIC has adapted to the evolving needs of modern policyholders. As more customers prefer purchasing financial products online, the insurer introduced the LIC New Tech Term Plan as its digital-first term insurance offering.

If you’re considering buying the New Tech Term Plan LIC, this article breaks down its features, eligibility, pros and cons, and how it compares to other term insurance plans in the market.

Key Features of LIC New Tech Term Plan

Eligibility Criteria

- Entry Age: 18 to 65 years

- Maximum Maturity Age: 80 years

- Sum Assured: ₹50 lakh to no limit (as per underwriting)

- Policy Term: 10 to 40 years (depending on variant selected)

Two Death Benefit Options

The LIC New Tech Term Plan 954 offers two variants: Option 1 (Level Sum Assured) and Option 2 (Increasing Sum Assured).

In the first option, the sum assured remains constant throughout the policy term. However, in the second option, your sum assured increases accordingly:

- Years 1-5: Basic Sum Assured (X)

- Year 6 onward: Increases by 10% of X annually

- By Year 15: Becomes 2X

This structure is designed to combat inflation, though the increase stops after the 15th year.

Option to Take Death Benefit in Installments

The plan allows you to receive the death benefits in installments over the chosen period of 5, 10, or 15 years instead of a lump sum amount.

Premium Payment Options

The LIC New Tech Term Plan offers regular pay, where you pay premiums throughout the policy term, and limited pay (policy term minus 5/10 years).

Premium Payment Modes

You get to choose between yearly and half-yearly payment modes. Monthly payments are not available.

Premium Rates

Smokers pay higher rates under this plan, and non-smoker rates are subject to you passing the urinary cotinine test. Moreover, discounted premium rates are also available for women.

Accident Benefit Rider

By adding the accident benefit rider, you receive an additional payout on top of your base sum assured in case of accidental death. The maximum aggregate limit of the accident benefit cover (across all policies) cannot exceed ₹100 lakh. You can opt for it at any time during the premium-paying term of your base policy (provided the PPT is at least 5 years), but coverage ends at age 70.

LIC: Performance Metrics

For the Amount Settlement Ratio (ASR), we have considered the average of FY 21-24, as the latest FY 24-25 metrics haven’t been released yet.

Key Insights on LIC’s Operational Metrics

- The CSR indicates the percentage of the number of claims settled against the total number of claims received. Although LIC’s 98.35% CSR shows a strong record in honoring claims, some competitors, such as Axis Max Life (99.62% FY 22-25) and HDFC Life (99.55% FY 22-25), perform slightly better.

- The ASR shows how much of the total claim amount filed was actually paid. Since there is no partial settlement in term insurance, it’s still an important metric showing whether the insurer treats both high and low value claims fairly. LIC’s ASR of 95.5% is strong, but competitors like Axis Max Life (96.2% FY 22-25) perform better.

- The solvency ratio reflects an insurer’s ability to meet long-term obligations, and LIC’s 2.0x is well above IRDAI’s mandated 1.5x. However, competitors such as Bajaj Life offer higher solvency ratios (4.37x FY 22-25).

- LIC’s business volumes are the highest in the industry, indicating brand trust. In fact, as of December 2025, LIC contributed to maintaining approximately 57.7% market share for the year.

- LIC’s low complaint volume of 4.57 is commendable considering the insurer’s size and business.

The above metrics pertain to LIC's overall life insurance segment, which includes term insurance, savings plans, ULIPs, and other products. While these metrics are not disclosed separately for the LIC New Tech Term Plan, they are still relevant.

Benefits and Drawbacks of LIC New Tech Term Plan

Benefits

- Strong backing by a government-owned insurer.

- High claim settlement credibility due to strong CSR and ASR.

- The plan offers a simple, straightforward structure, perfect for individuals seeking a no-frills policy.

Drawbacks

- Limited customization, as there is no option for critical illness or waiver-of-premium riders, and it omits various in-built features, such as a terminal illness benefit.

- Doesn’t provide the Life Stage Benefit option to increase cover automatically upon major life events such as marriage, childbirth, etc., due to a missing Life Stage Benefit.

- Higher premiums when compared to similar, more feature-rich, and affordable term plans offered by private insurers.

Premiums of LIC New Tech Term Plan

For this example, we’ve considered healthy, non-smoking, salaried individuals living in a tier-1 city like Delhi, covered until the age of 65, with a sum assured of ₹2 crore.

Note: The premiums shown in the table above are indicative only and may vary based on factors such as your age, occupation, medical history, income, underwriting decisions, etc.

You can estimate premiums using the LIC New Tech Term Plan Calculator available on LIC’s official website.

How to Buy the LIC New Tech Term Plan?

1) Go to the LIC website.

2) Scroll down and click on “Term Insurance Plans.”

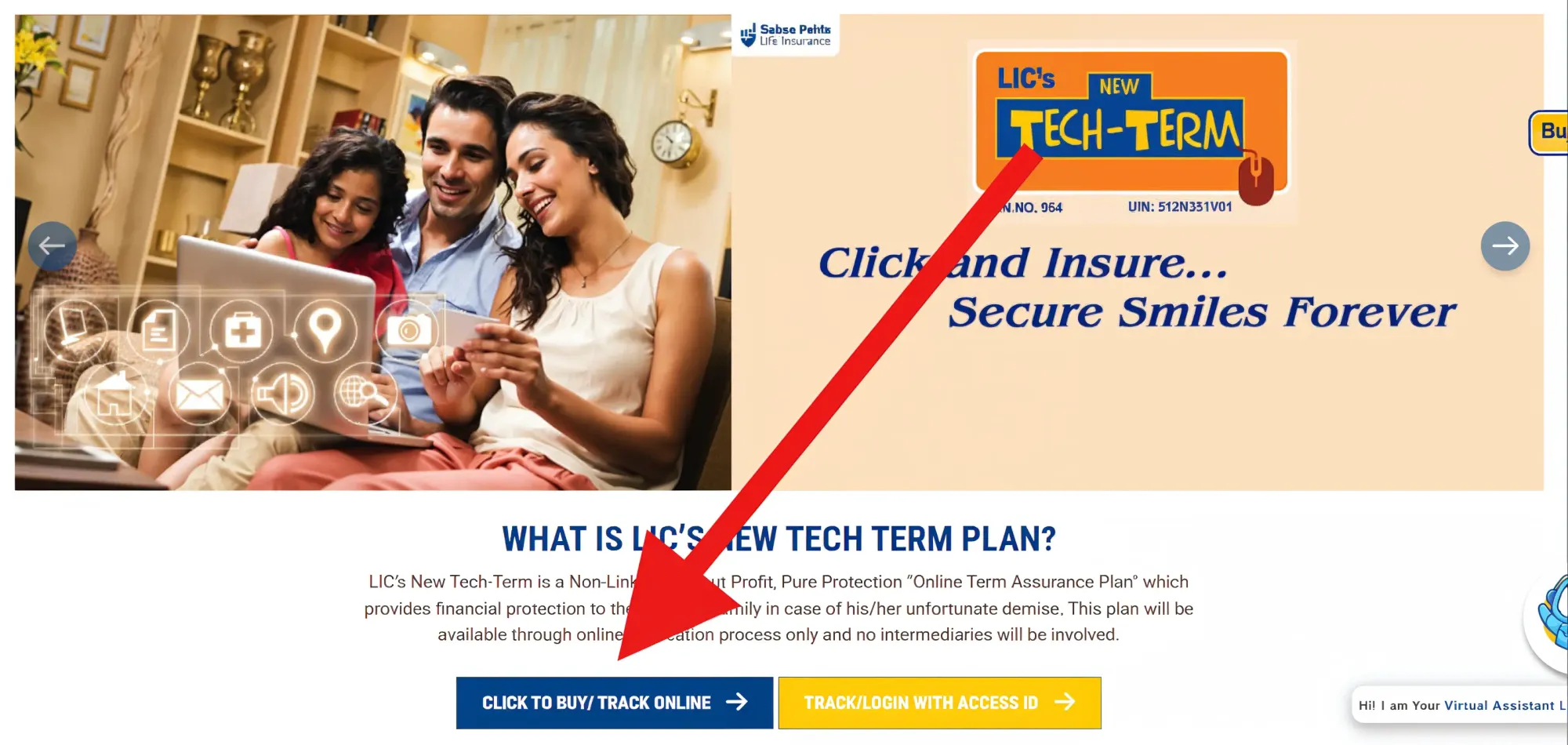

3) Once you select LIC’s New Tech Term Plan, you can click on learn more and you’ll be redirected to the New Tech Term Plan page.

4) Select “Click to Buy/Track Online.”

5) Fill in your details and requirements, complete the proposal form, submit the required documents, and wait for approval and underwriting decisions after medical tests.

Who Should Choose the LIC New Tech Term Plan?

Individuals Prioritizing Brand Trust Over Features

LIC has operated since 1956, and many buyers value its long-standing reputation and strong nationwide presence.

Individuals Wanting Government-Backed Coverage

Some buyers explicitly prefer a government-owned insurer to private companies, especially for long-term contracts such as term insurance. Since LIC is majority-owned by the Government of India, you can consider it.

Buyers Looking for a Simple, Online-Only Term Plan

If you want a clean structure, minimal decision fatigue, and direct online purchase without agent involvement, you can opt for it.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Ditto’s Take on LIC New Tech Term Plan

While LIC’s brand trust and operational stability are strong, the plan struggles to compete with leading private term insurance products in pricing, inbuilt features, rider flexibility, and customizations.

From a purely product standpoint, the LIC New Tech Term Plan is not a comprehensive option.

For someone who values simplicity and the LIC brand above all else, this plan works. But if you’re optimizing for features and cost-efficiency, you may find better alternatives in the private insurance space with insurers such as Axis Max Life and HDFC Life. For more details, you can check out our comprehensive guide on the best term insurance plans in India.

Full Disclosure

Frequently Asked Questions

Last updated on: