Quick Overview

LIC New Jeevan Amar is designed for those seeking straightforward financial protection for their family, without the complexity of multiple features. While it keeps things simple compared to modern term plans, many customers still prefer plans offered by LIC for its long-standing reliability and sense of financial security.

This guide walks you through the LIC New Jeevan Amar Plan review, covering its features, benefits, drawbacks, and whether it suits your financial protection needs.

LIC: Performance Metrics

Note: The above values reflect the overall performance of the LIC life insurance portfolio and are not limited to its term products.

Eligibility Criteria of LIC New Jeevan Amar

Key Features of LIC New Jeevan Amar Plan

- Sum Assured: The minimum basic sum assured starts at ₹25 lakh, with no fixed upper limit. The maximum cover is determined based on eligibility and underwriting as per the insurer’s policy guidelines.

- Death Benefit Options: You can choose between a level or an increasing sum assured. Under the increasing option, the cover stays constant for the first 5 years, increases gradually until year 15, and then stabilizes at twice the base cover.

- Rider Option: You can enhance the policy by adding an accident benefit rider under regular or limited pay, subject to applicable conditions.

- High Sum Assured Rebate: The policy offers a discount for opting for higher sum assured levels. As the coverage amount increases, the insurer provides a rebate on premiums, making larger life cover relatively more cost-efficient for policyholders. For instance, under the level sum assured option, if a 30-year-old chooses a ₹1 crore cover, they get a premium discount of up to 25%, making higher coverage more cost-effective.

Premiums for LIC New Jeevan Amar Plan

Note: The sample illustrative premiums for the two plan variants are based on a basic sum assured of ₹50 lakh for a non-smoker male with a policy term of 20 years. The figures are extracted from the LIC New Jeevan Amar Plan Brochure.

Drawbacks of LIC New Jeevan Amar Plan

- Limited Features: The plan mainly focuses on providing basic term life cover without many built-in benefits. Compared to modern term plans, it lacks additional features like enhanced payout structures, flexible benefits, or comprehensive add-ons that improve overall protection.

- Minimal Rider Options: It offers only one add-on. This means you cannot fully customize the policy with important protections like critical illness cover or disability benefit that are commonly available with private insurers.

- Higher Premiums: The premium for this plan may be higher when compared to similar term insurance products offered by private insurers. Despite offering basic coverage, the cost efficiency is lower, especially for younger buyers who may find better value alternatives in the market.

- Offline Purchase Only: The policy is primarily distributed through offline channels, which can make the buying process slower and less convenient. It also limits quick digital access for purchase, policy management, or comparisons with other plans online.

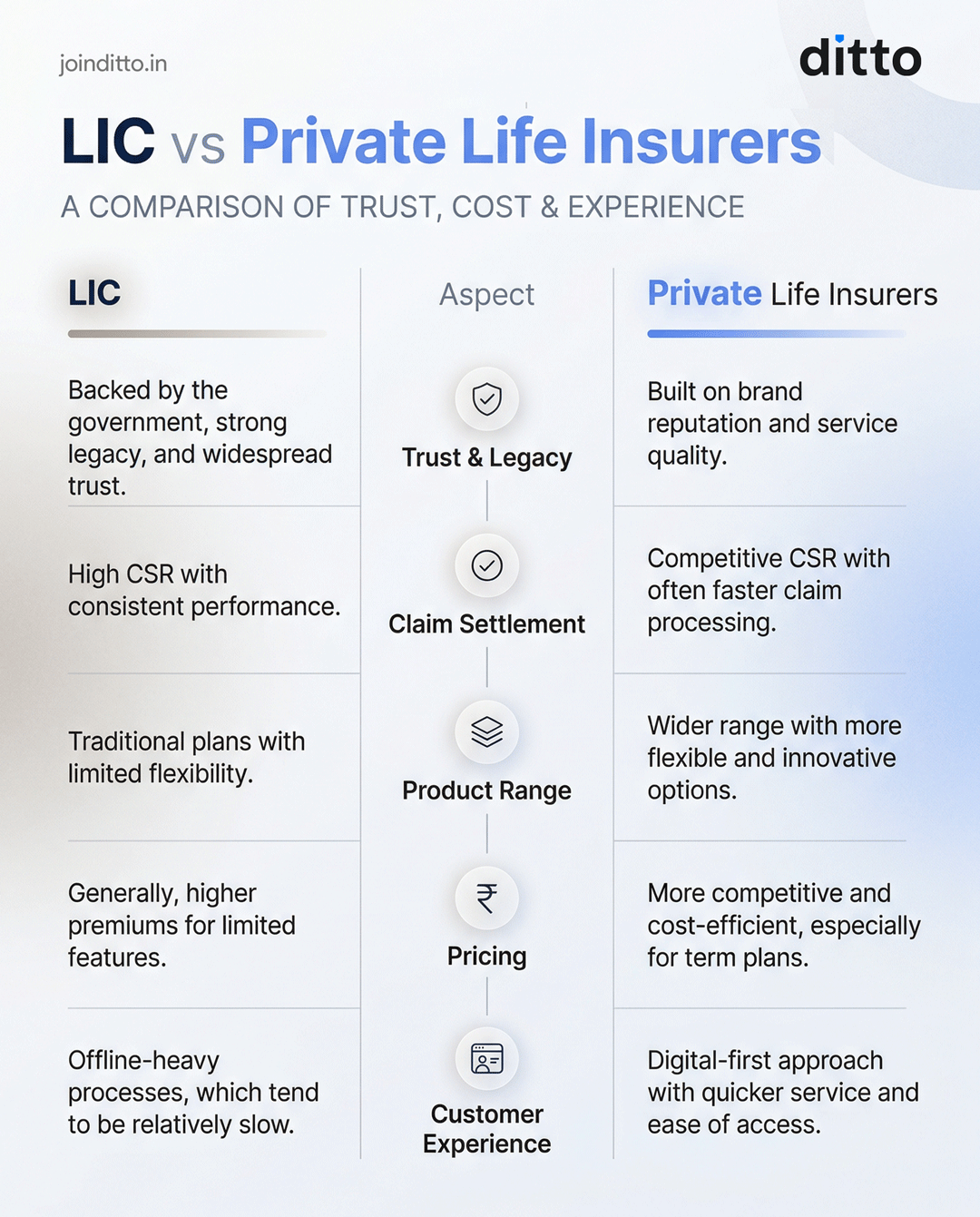

LIC vs Private Life Insurers: Which Is Better?

The difference between LIC and private life insurers lies in their approach to insurance. LIC generally offers more traditional products, whereas private insurers provide customized plans with competitive pricing and faster service.

Check out the infographic for a better understanding.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Conclusion

The LIC New Jeevan Amar Plan is suitable for individuals who prefer a simple life cover for their dependents and are comfortable paying higher premiums in exchange for trust and brand legacy. If you wish to purchase an LIC term plan, you can also consider the New Tech Term Plan as an online alternative.

However, these plans lack several advanced in-built features such as instant payouts on claim intimation and key riders like waiver of premium. If you are looking for a term plan from insurers with personal customization and affordable riders, we recommend the best term insurance plans, which align with your future goals.

Frequently Asked Questions

Last updated on: