Quick Overview

At Ditto, many customers come to us asking, “Is ₹1 crore term insurance enough for my family's needs?” The better question is whether that amount can truly sustain your family’s lifestyle, liabilities, and fund future goals if you are not around tomorrow.

This guide helps you assess if your current cover is sufficient and how to arrive at a more accurate amount based on your financial needs and responsibilities.

What Does ₹1 Crore Term Insurance Actually Cover?

- Replaces Your Income and Clears Liabilities: The death payout is meant to step in for your earnings and take care of major debts like home or personal loans, so your family is not left with financial burdens.

- Supports Daily Living and Ongoing Expenses: Household costs like rent, school fees, groceries, and utilities continue, and the death payout helps your family maintain their lifestyle without disruption.

- Funds Future Goals: Long-term needs like children’s education and marriage are part of what an amount of ₹1 crore is expected to cover.

Why ₹1 Crore May Not Be Enough?

- Everyday Expenses Don’t Stop: Your family’s routine continues even in your absence. Rent, groceries, school fees, and bills still need to be paid. Over time, the payout gets used up, and what seemed sufficient at first can start to feel tight.

- Inflation Reduces the Death Benefit: Costs for education, healthcare, and daily living keep rising. A fixed ₹1 crore does not grow, so its real value keeps falling.

- Loans Reduce the Available Amount: Large liabilities like a home loan are usually cleared first. This can take up a big portion of the payout, leaving less money for other long-term needs.

A Real-life Case Worth Noting

How to Calculate the Right Term Insurance Coverage Amount?

While calculating the required term cover, Human Life Value (HLV) helps measure the financial gap your family would face if the main earner passes away.

In practice, there are 3 different methods to calculate the required term cover:

- Income Replacement (Present Value): Estimates how much your family would need today to replace your income until retirement, factoring in inflation. It is a top-down approach based on your earning potential.

- Need-Based Method: Calculates coverage by adding living expenses, liabilities like loans, and future goals such as education. It is a detailed bottom-up approach.

- Income Multiple: Uses a simple rule of 10 to 30 times annual income for a quick estimate. It is easy to apply, but less personalized.

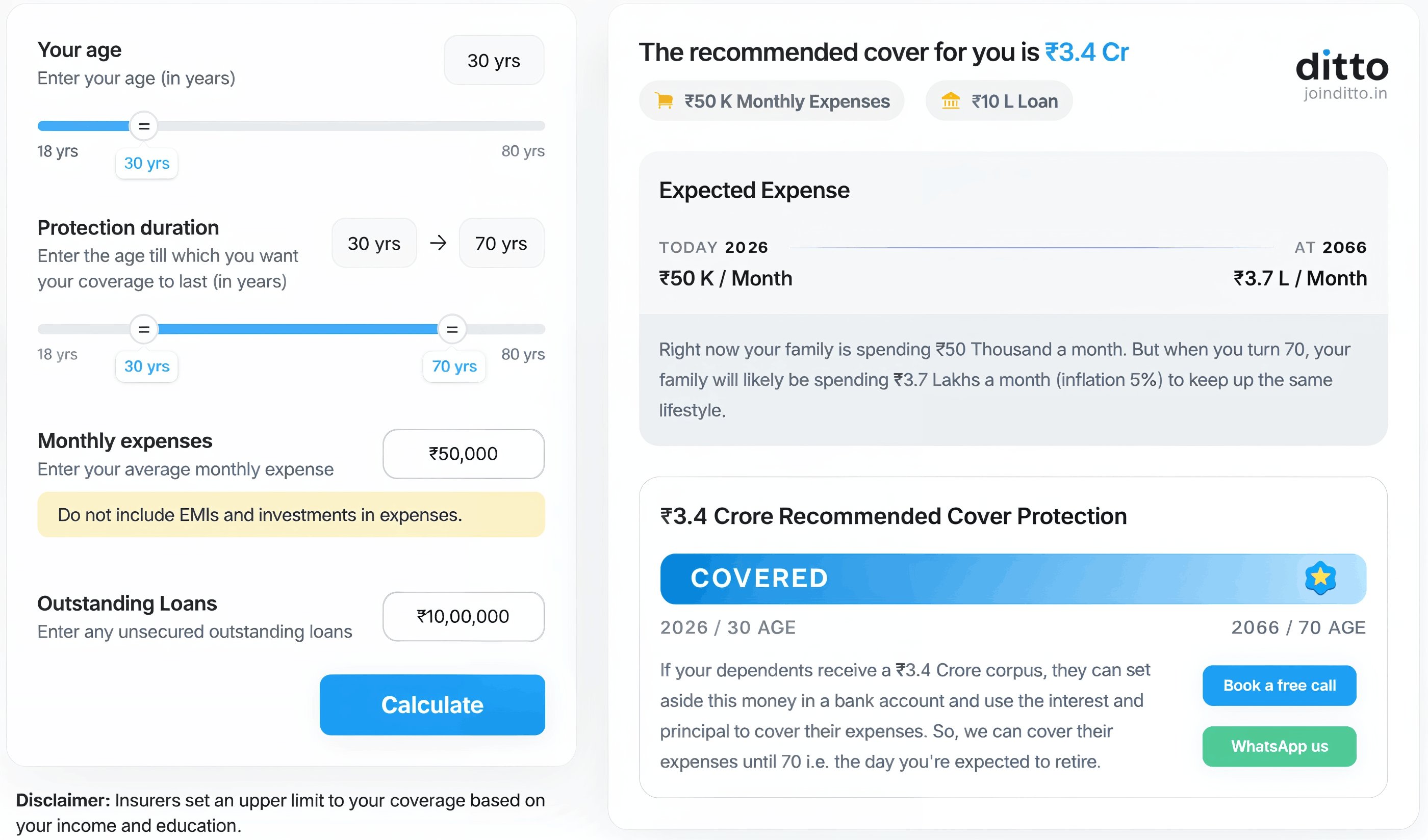

Note: At Ditto, we estimate your ideal term cover using the expense and liabilities method. For a clearer picture, you can use our online calculator to find the coverage that fits your needs. Unlike many tools, it does not subtract personal assets, ensuring your cover fully protects your family’s financial needs rather than relying on long-term investments.

Here’s a snippet from our term calculator based on a 30-year-old married person’s profile.

When to Consider ₹2 Crore or a Higher Sum Assured?

- You have Significant Financial Responsibilities: If you have dependents, a home loan, or a single-income household, a higher cover ensures your family can manage both immediate and long-term needs comfortably.

- Your Income Needs to be Replaced for Several Years: If your family depends on your earnings for 15–25 years, ₹1 crore may not sustain expenses over that period, especially with rising costs.

- You Have Major Future Goals: Children’s education, marriage, and other milestones can require substantial funds, making higher coverage more practical.

- You want to Ensure Long-Term Financial Stability: A higher cover provides a stronger cushion for your spouse’s future and reduces the risk of financial compromise later.

You can apply for any level of cover you consider appropriate. However, the final approved sum assured is determined by the insurer based on factors such as age, income, education, and existing life insurance. Income documents are required to support the requested cover, and the policy issuance is subject to underwriting and an overall assessment of your profile.

Note: Term premiums do not increase proportionately with higher cover, which means moving from ₹1 crore to ₹2 crore often costs far less than people expect.

Premiums Across Ages and Sum Assured

Note: The illustrative annual premiums for a non-smoker male vary with sum assured and age. These premiums are for HDFC Life Click 2 Protect Supreme Plus with coverage up to age 70, without discounts.

Key Insights:

- A ₹3 crore term cover typically costs only about 2.5 to 2.8 times a ₹1 crore plan, making a higher sum assured more cost-efficient.

- Premiums rise sharply with age. A 45-year-old may pay more for a ₹1 crore cover than a 25-year-old pays for a ₹3 crore cover.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Conclusion

₹1 crore term cover can feel like a large, reassuring number. But once you factor in loans, everyday expenses, and inflation, it often works more as a starting point than a complete solution. Here’s few tips you must go through before purchasing a term plan:

- Opt for Higher Cover Early: If you have dependents, loans, or long-term responsibilities, choosing a higher sum assured early can be more effective and helps lock in lower premiums.

- When a Lower Cover May Suffice: If you have strong assets, investments, or multiple income sources, a lower cover could be adequate.

- Look Beyond Price: Evaluate features, benefits, insurer metrics like Claim Settlement Ratio (CSR), and flexibility, not just premiums.

- Plan Comprehensively: Align term insurance with investments like mutual funds, health cover, and savings for complete financial security.

If you are looking for a term plan from insurers with established track records, we recommend the best term insurance policies, which align with your long-term goals.

Frequently Asked Questions

Last updated on: