Overview

Buying term insurance is one of the most important financial decisions you’ll make. But before you commit, you need one simple answer: how much will it cost?

That’s exactly what the ICICI term insurance premium calculator is built for. In a few clicks, it estimates your annual or monthly premium based on your personal details.

This guide walks you through how to use it, shows you real sample premiums across age groups, and helps you decide whether ICICI’s iProtect Smart Plus is the right choice for your needs.

How to Use the ICICI Pru Term Insurance Calculator

Follow these steps to get your premium estimate:

1. Go to the official website: iciciprulife.com

2. Click the “Check Quote” button under the ‘Calculate Term Insurance Premium’ section.

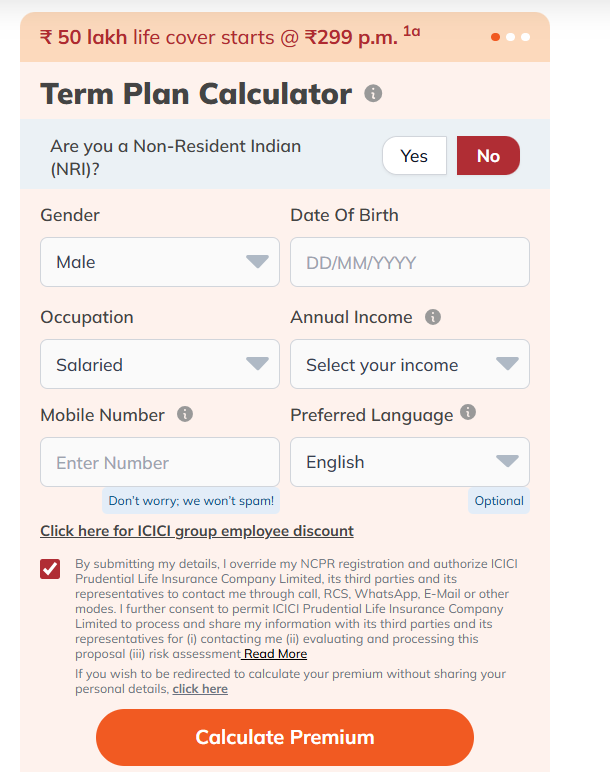

3. Enter your basic details, such as gender, date of birth, occupation, annual income, NRI status, mobile number, and preferred language.

4. Specify whether you smoke or use tobacco products.

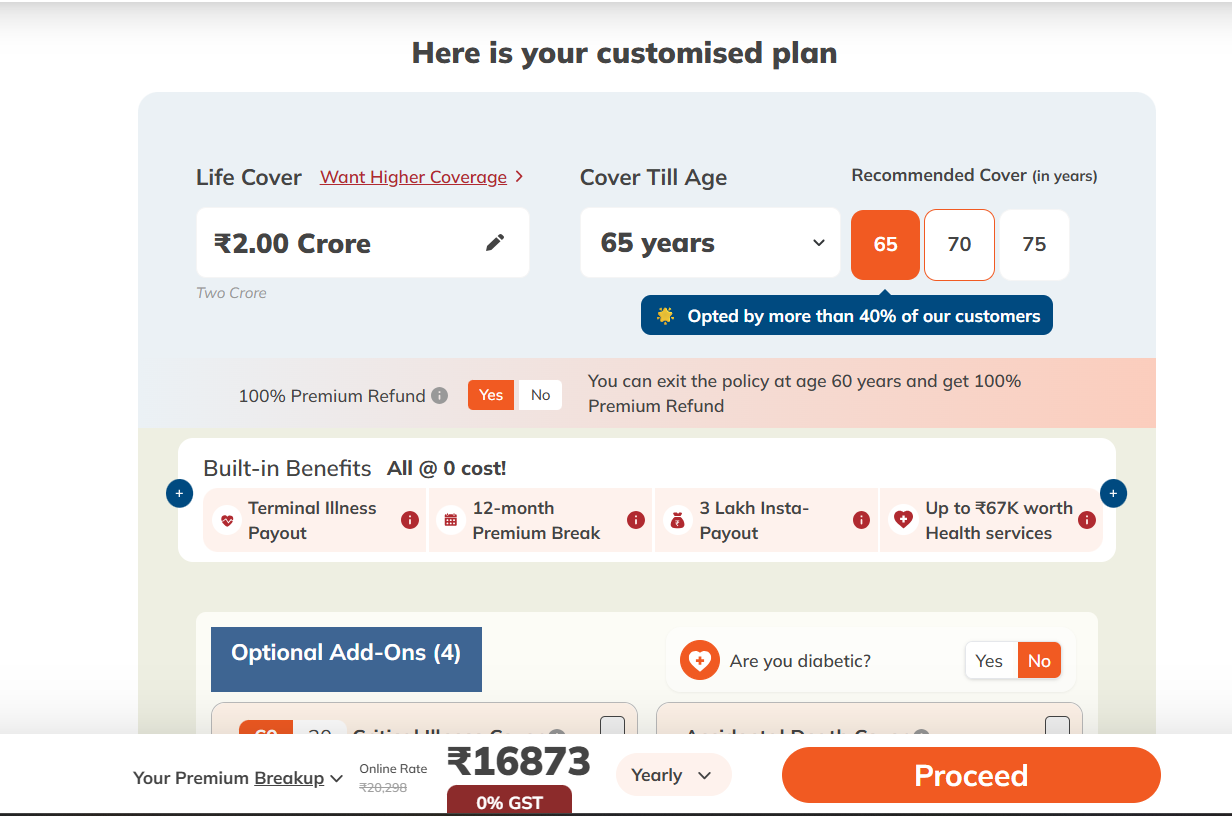

5. Customize your plan: choose the sum assured (e.g., ₹1 crore or ₹2 crore), policy term, payout option (lump sum or income), and any add-on riders.

6. Your annual premium will be displayed immediately at the bottom of the screen.

Pro Tip: Always check the second-year premium (not the introductory first-year discount) to understand your actual long-term cost. Apart from that, keep in mind that the ICICI term insurance plan calculator only shows baseline numbers. The actual premium may vary depending on loading charges applied after underwriting and medical tests.

Factors That Affect Your ICICI Term Insurance Premium

Here are the biggest factors that influence your ICICI term insurance premium:

- Age: Age is one of the most important pricing factors. The younger you are when you buy a policy, the lower your premium tends to be because insurers see younger individuals as lower-risk applicants. Premiums usually rise gradually in your 20s and early 30s, but can increase more sharply after 35 or 40.

- Sum Assured: A higher cover amount naturally increases the premium because the insurer assumes a larger payout obligation. However, larger covers are often more cost-efficient on a per-lakh basis, which is why many financial advisors recommend adequate coverage rather than opting for the lowest possible premium.

- Policy Term: Policies with longer coverage durations generally cost more because the insurer is covering you for a greater number of years. For example, a policy lasting until age 65 will usually cost less than one extending till age 85.

- Smoker Status: Tobacco usage significantly impacts pricing. Smokers and tobacco users are considered higher-risk applicants due to the increased likelihood of health complications, which is why premiums can sometimes be 60% to 100% higher than those for non-smokers.

- Gender: Women typically receive slightly lower premiums than men because statistically, they tend to have a longer life expectancy and lower mortality risk in certain age groups.

- Add-on Riders: Optional riders such as critical illness cover, accidental death benefit, or waiver of premium provide additional protection beyond basic life cover. While these benefits improve the policy’s overall coverage, they also increase the premium.

- Payout Option: Choosing how the death benefit is paid can also affect pricing. A pure lump-sum payout may be priced differently from options that combine lump-sum benefits with monthly income payouts for dependents.

For more detailed information, refer to the factors affecting your life insurance premium guide.

Sample ICICI Term Insurance Premiums by Age and Cover

Premium Comparison for a ₹2 Crore Cover

Profile Considered: Premiums are for a ₹2 crore sum assured with coverage until age 65, for a non-smoking male resident of Delhi (110010). The figures do not include first-year discounts (2nd-year premiums) or any additional riders.

Premium Comparison for a ₹1 Crore Cover

Profile Considered: Premiums are for a ₹1 crore sum assured with coverage until age 65, for a non-smoking male resident of Delhi (110010). The figures do not include first-year discounts (2nd-year premiums) or any additional riders.

Key Takeaways:

- ICICI Prudential iProtect Smart Plus remains competitively priced across most age groups, especially at ages 30 and 35, where it is priced slightly lower than HDFC Life.

- Axis Max Life offers marginally lower premiums at ages 25 and 40, but the differences are fairly small overall.

- This shows that all three plans are closely matched in pricing, making features, claim experience, and rider options equally important when choosing a plan. If you want more options, you can take a look at the best term insurance plans in India in 2026.

ICICI iProtect Smart Plus: Is It the Right Plan for You?

ICICI Prudential’s iProtect Smart Plus is one of India’s most popular term plans, and for good reason.

What Makes It Worth Considering

- Comprehensive Add-on Options: critical illness cover for up to 60 conditions, accidental death benefit, and waiver of premium.

- Flexible Payout Options: lump sum, monthly income, or a combination of both.

- Terminal Illness Benefit: The terminal illness benefit is included as an accelerated payout from the base life cover at no extra cost.

- Life Cover Increase: Option to increase cover at key life milestones (marriage, childbirth).

Potential Drawbacks to Keep In Mind

- Lower CSR (98.03%, on average from FY 2022-2025) than the industry average of 98.66%. Insurers like HDFC Life and Axis Max Life have CSRs above 99.5%.

- Complaint volumes for the insurer (11 per 10,000 claims, on average for FY 2022-2025) are higher than those of competitors like HDFC Life (1.33 complaints) and Axis Max Life (5.67 complaints).

Verdict: ICICI Pru iProtect Smart Plus is a strong term insurance plan that combines competitive pricing with useful features. It is particularly attractive for buyers looking for higher cover amounts at relatively affordable premiums.

That said, while the plan performs well overall, competitors like HDFC Life and Axis Max Life currently have slightly stronger claim settlement and complaint metrics. The right choice ultimately depends on your age, budget, required cover amount, and whether features like critical illness riders or income payouts matter to you. Since term insurance is a long-term commitment, it is always advisable to compare at least 2-3 top policies before making a final decision.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat with us on WhatsApp!

Conclusion

The ICICI term insurance calculator is one of the quickest ways to estimate how much you may pay for an ICICI Pru iProtect Smart Plus policy before starting the application process. In just a few minutes, you can compare premiums across different cover amounts, policy terms, and rider combinations to understand what fits your budget best.

While iProtect Smart Plus is a strong and competitively priced plan from the insurer, term insurance is a long-term financial commitment. Even small differences in annual premiums, features, or claim experience can matter over a 30–40 year policy term. That is why it is important to use the ICICI term insurance calculator as a starting point and compare it with at least 2–3 other top term plans before making a final decision.

Frequently Asked Questions

Last updated on: