Yes, you can change the nominee in term insurance at any time while the policy is active. Most insurers allow policyholders to update nominee details either online through the insurer’s website or offline by submitting a nomination change form at a branch office.

The process usually requires the policy number, identity proof, nominee KYC documents, and appointee details if the nominee is a minor. Once the request is verified, the insurer updates the nomination through an endorsement acknowledgment. Policyholders can change nominees multiple times, and the latest valid nomination automatically replaces all previous nominee details in the policy records.

This guide explains how to change a nominee in term insurance, the required documents, key term insurance nominee rules, and common mistakes to avoid during the update process.

When buying term insurance, most policyholders primarily focus on the coverage amount and premium. However, one important detail that often gets overlooked is the nominee in term insurance, the person authorized to receive the claim payout if the policyholder passes away during the policy term.

A nominee is usually the policyholder’s spouse, children, or parents, since they are financially dependent on the insured individual and are also natural legal heirs. However, nominee details should not remain unchanged forever. Major life events such as marriage, childbirth, divorce, remarriage, or shifts in financial dependency are strong reasons to review and update the nomination. For example, a policyholder may initially nominate parents while purchasing the policy in their 20s, but later their spouse and children may become the primary financial dependents.

That is why regularly reviewing nominee details is just as important as maintaining adequate life insurance coverage.

If you need help understanding nominee rules, claim settlement processes, or reviewing your term insurance policy, book a free call or WhatsApp us for clear, unbiased guidance tailored to your needs.

Can You Change the Nominee After Buying Term Insurance?

Yes, you can change the nominee in term insurance at any time while the policy is active. Under Section 39 of the Insurance Act, 1938, policyholders may add or update nominee details before the policy matures. Once the request is submitted and approved, the insurer updates the nomination in its records through an endorsement acknowledgment.

Here are a few important things to know:

You can update your nominee multiple times during the policy term.

The latest nomination automatically replaces all previous nominations.

Most insurers do not charge any fee for nominee changes.

Insurers issue an endorsement acknowledgment instead of a fresh policy document, so it is advisable to safely store this acknowledgment along with your original policy papers.

For example, you may have purchased a term plan at age 25 and nominated your mother. Later, after getting married and having a child, you can update the nomination to reflect your current financial dependents more accurately.

CTA

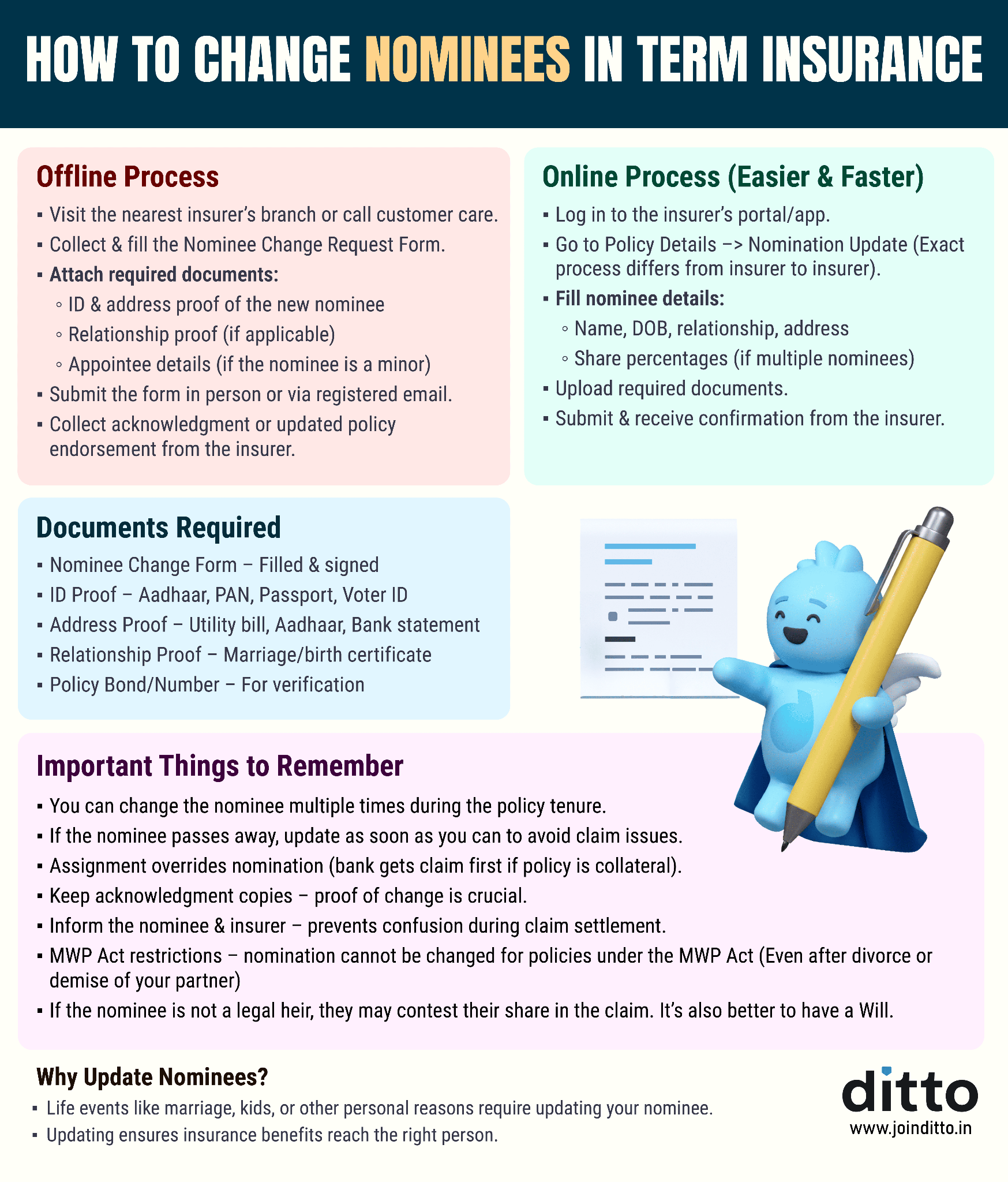

Step-by-Step Process to Change Nominee in Term Insurance

Updating your nominee in term insurance is a simple servicing request. Most insurers today offer a built-in nominee update option through their website or mobile app, making the process fairly quick and convenient.

However, in certain situations, insurers may still require a signed offline servicing form and supporting documents, especially for complex changes such as adding a minor nominee, changing appointee details, or updating multiple nominees. For example, insurers like HDFC Life Insurance may ask policyholders to submit a physical policy servicing request form for specific nomination-related changes.

You can refer to the visual guide below for a complete step-by-step breakdown of the nominee change process.

Term Insurance Nominee Rules: Who Can Be a Nominee?

Insurers recognize the following types of nominees in term insurance:

Beneficial Nominee: A beneficial nominee includes immediate family members such as your spouse, children, or parents. As per the Insurance Laws (Amendment) Act, 2015, these nominees are considered the rightful beneficiaries of the claim amount. Since they are also natural legal heirs in most cases, insurers usually process claims more smoothly for them. Legal heirs generally cannot override their claim unless directed by a court.

Minor Nominee: A minor can also be added as a nominee in term insurance. However, since a child below 18 years cannot legally handle financial payouts, the policyholder must appoint an adult guardian or appointee. The guardian manages the claim amount until the minor turns 18.

Multiple Nominees: Most insurers allow policyholders to add multiple nominees to a term insurance policy, usually up to 3 or 4, and divide the claim amount among them in specific percentages.

For example:

Spouse: 50%

Child 1: 25%

Child 2: 25%

The total allocation across all nominees must always add up to 100%. This option is particularly useful when multiple family members are financially dependent on the policyholder’s income.

Non-family Nominee: In some cases, insurers may allow siblings, distant relatives, friends, or business partners to be added as nominees. However, such requests are usually evaluated carefully on a case-by-case basis due to “moral hazard” concerns, in which insurers assess whether the nominee has a legitimate financial relationship with the policyholder.

This is why immediate family members are preferred as nominees. In many cases, non-family nominees may receive the insurance payout as recipients, while the ultimate ownership of the amount may still be subject to succession laws or legal disputes among heirs.

Why Choosing the Right Nominee Matters Legally

Nominee rules in term insurance have changed significantly over the years, which is why choosing the right nominee is important.

Earlier, under a 1983 Supreme Court judgment (Sarbati Devi v. Usha Devi), a nominee was treated only as the person receiving the insurance money on behalf of the legal heirs. The nominee did not automatically become the final owner of the claim amount.

However, after the 2015 amendment to Section 39 of the Insurance Act, the law introduced the concept of a “beneficial nominee.” This means that if the nominee is the policyholder’s spouse, children, or parents, they are generally treated as the rightful beneficiaries of the claim amount.

As a result, choosing immediate family members as nominees can help reduce legal disputes and make claim settlement smoother for families.

Common Mistakes to Avoid When Updating Your Nominee

Keeping Outdated Nominees: Many policyholders continue to keep parents as sole nominees even after marriage or the birth of children, despite changing financial responsibilities.

Forgetting Updates After Major Life Events: Nominee details are often not updated after marriage, divorce, remarriage, childbirth, or the death of an existing nominee.

Not Appointing a Guardian for Minor Nominees: If the nominee is a minor, appointing an adult guardian or appointee is mandatory for claim processing.

Incorrect Personal Details: Using nicknames, initials, or spellings that do not match Aadhaar or PAN records can create verification issues during claims.

Ignoring the Endorsement Acknowledgment: Insurers usually issue an endorsement acknowledgment after nominee updates, not a fresh policy document. This acknowledgment should be safely stored.

Not Informing the Nominee: Many nominees are unaware of the policy, insurer details, or document location, which can create confusion during claim settlement.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Ditto’s Take on Changing Nominees in Term Insurance

A term insurance policy is meant to financially protect the people who depend on your income. That is why your nominee details should accurately reflect your current family and financial responsibilities at every stage of life.

Here are a few simple practices that can help avoid future claim complications:

Prefer immediate family members such as your spouse, children, or parents as nominees.

Divide the claim amount based on the actual financial dependency of each nominee.

Ensure names, dates of birth, and other details exactly match official government IDs such as Aadhaar or PAN.

Safely store every endorsement acknowledgment received after updating nominee details.

Most importantly, review your nomination whenever major life events occur, such as marriage, childbirth, divorce, or the death of an existing nominee.

Frequently Asked Questions

Can we change the nominee in term insurance after buying the policy?

Yes, you can change the nominee in term insurance anytime while the policy is active. Under Section 39 of the Insurance Act, 1938, policyholders can modify nominations before the policy matures. Most insurers allow nominee changes free of cost through online or offline servicing requests. The latest nomination automatically replaces the previous one. After approval, the insurer updates its records and issues an endorsement acknowledgment confirming the change. This becomes the valid proof of nomination, since insurers usually do not issue a fresh policy document after updating nominee details.

How many times can I change the nominee in term insurance?

There is no restriction on how many times you can change the nominee in term insurance while the policy remains active. Each new nomination automatically cancels the earlier nomination, and the insurer considers the most recent valid nominee at the time of claim settlement. Most insurers process nominee changes at no additional cost. It is advisable to review and update nominee details after major life events such as marriage, childbirth, divorce, remarriage, or the death of an existing nominee to ensure the insurance payout reaches the correct financial dependents without unnecessary complications.

What documents are required to change the nominee in term insurance?

To change nominee details in a term insurance policy, insurers generally require a signed nomination change form, policy number, and KYC documents of the new nominee, such as Aadhaar and PAN. The nominee’s name should exactly match official government records to avoid verification issues during claim settlement. If the nominee is a minor, details and KYC documents of the appointed guardian or appointee must also be submitted. Online requests are usually processed faster, while offline requests at branches may take longer. Always preserve the endorsement acknowledgment issued after the nominee update is completed.

Is there any charge to change the nominee in term insurance?

No, most insurers in India do not charge any fee for changing nominee details in a term insurance policy. It is treated as a standard policy servicing request and can usually be completed online through the insurer’s portal or offline at a branch office. Once the request is processed, the insurer updates the nomination in its records and issues an endorsement acknowledgment confirming the change. Since nominee updates are generally free, policyholders should regularly review and update nomination details after important life events to ensure smoother claim settlement for their family members later.

What happens if the nominee dies before the policyholder?

If the nominee dies before the policyholder and the nomination is not updated, the insurer may not be able to release the claim amount directly. In such cases, the payout usually goes to the legal heirs based on succession laws, which can delay claim settlement. Family members may also need to provide additional legal documents, such as a succession certificate or probate before the claim is processed. To avoid complications, policyholders should update nominee details whenever there is a major family change or the existing nominee passes away.

Can a minor be a nominee in term insurance?

Yes, a minor can be named as a nominee in a term insurance policy. However, since a child below 18 years cannot legally manage the insurance payout, the policyholder must appoint an adult guardian or appointee. The guardian receives and manages the claim amount on behalf of the minor until the child reaches legal adulthood. Insurers generally require the guardian’s identity proof, relationship details, and KYC documents during nomination. Forgetting to appoint an appointee for a minor nominee is one of the most common mistakes policyholders make while purchasing or updating term insurance.

Can I add multiple nominees to one term insurance policy?

Yes, most insurers allow policyholders to add multiple nominees in a single term insurance policy, usually up to 3 to 4 nominees. You can divide the claim amount among them in percentage terms based on financial dependency. For example, you may allocate 50% to your spouse, 30% to your child, and 20% to your parents. The total allocation across all nominees must always equal 100%. Adding multiple nominees is particularly useful when more than one family member depends on your income, as it helps ensure that the insurance payout is distributed clearly and smoothly during claim settlement.

Can a friend or distant relative become a nominee in term insurance?

Yes, some insurers may allow friends, distant relatives, or even business partners to become nominees in a term insurance policy. However, such nominations are usually reviewed more carefully because insurers assess whether a genuine financial relationship exists between the policyholder and the nominee. This helps insurers reduce “moral hazard” risks and avoid suspicious or financially motivated arrangements. In some cases, insurers may ask for additional clarification or supporting documents before approving the nomination. Immediate family members such as spouse, children, or parents are generally preferred because claim settlement is usually simpler and legally clearer for all parties involved.

How long does it take to update nominee details in term insurance?

Online nominee update requests are usually processed within 3 to 7 working days if all documents are submitted correctly. Offline requests submitted through branch offices may sometimes take longer, depending on the insurer’s internal processing timelines and documentation requirements. Under IRDAI’s Master Circular on Protection of Policyholders’ Interests, 2024, insurers are required to acknowledge nominee change requests immediately and update the changes within 7 days. Once the request is approved, the insurer issues an endorsement acknowledgment confirming the updated nominee details. Since insurers generally do not issue a fresh policy document after nominee changes, this endorsement should be safely stored along with the original policy papers.

Does assigning a term insurance policy affect the nominee?

Yes, assigning a term insurance policy can affect or even cancel the existing nomination. Under Section 39 of the Insurance Act, 1938, if a policy is assigned under Section 38, the nomination is generally canceled automatically. However, there is an important exception. If the assignment is made to a bank, lender, or financial institution as collateral for a loan, the nominee’s rights are affected only to the extent of the assignee’s financial interest. After the outstanding loan amount is recovered, the remaining claim amount may still be payable to the nominee. This is why policyholders should review nominee details whenever they assign their policy for loans or other financial arrangements.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.