Quick Overview

If you’re in your late 20s or early 30s, you may wonder if you’ve missed the ideal time to buy a term insurance policy. While starting earlier does come with clear cost advantages, the window hasn’t closed. Buying term insurance in your 20s vs 30s is less about timing and more about how your responsibilities, costs, and coverage needs evolve.

This guide explains how age affects premiums, eligibility, and coverage, helping you choose the right protection as your financial needs evolve.

Why Buying Term Insurance in Your 20s Is Financially Smarter?

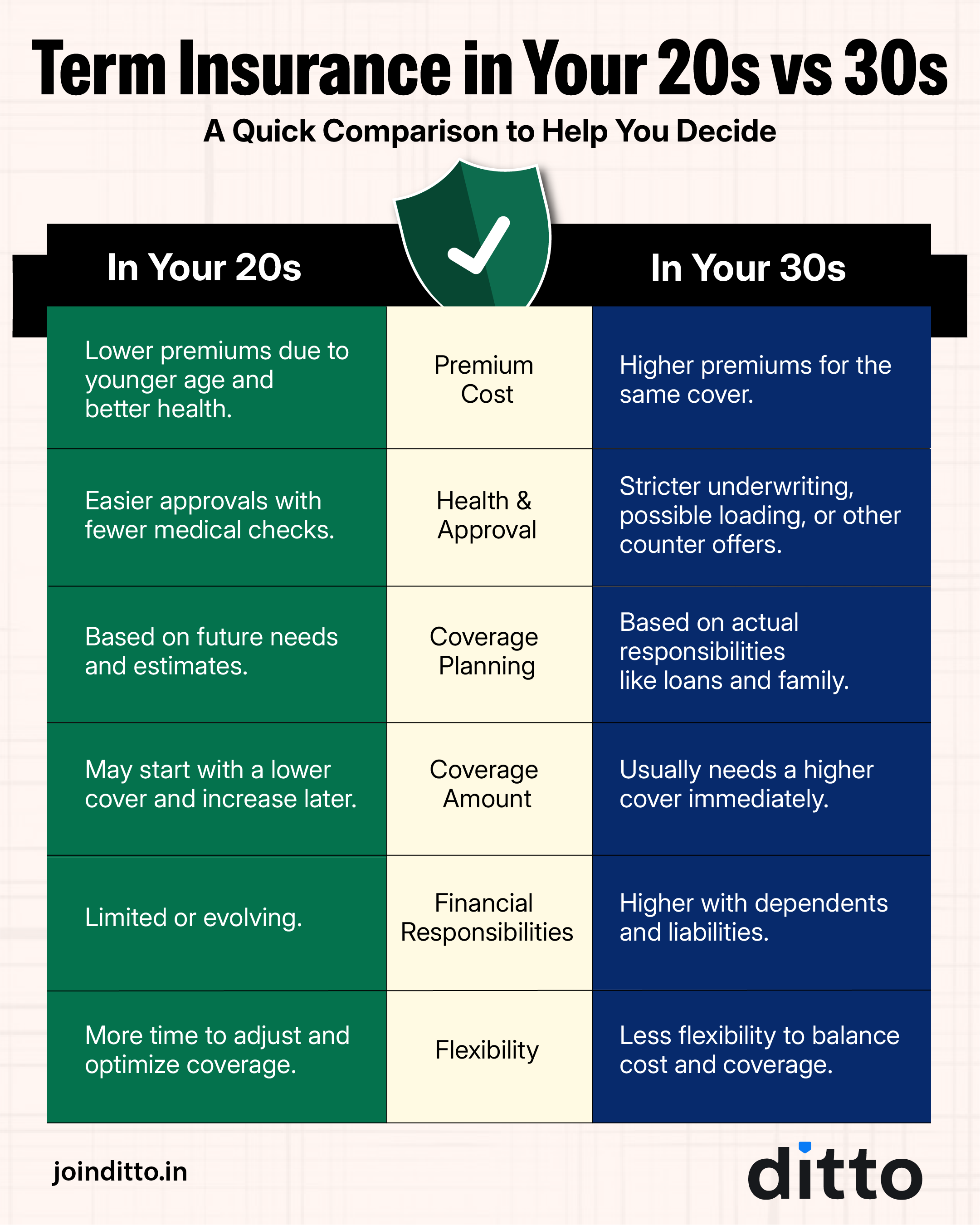

- Premiums Are Lower: Premiums generally depend on age, lifestyle, and health risk. In your 20s, insurers consider you a low-risk profile, so costs are much lower. The same ₹2 crore term cover can cost you around 1.5x more in your 30s than in your 20s.

- You Lock In Low Rates for Life: Term insurance premiums are fixed when you buy the policy. Starting early lets you secure lower premiums for the entire duration, often around 30 to 40 years.

- Longer Coverage Window: A policy started in your 20s can protect you through major life stages like career growth, family planning, and loan repayments.

- Financial Responsibilities Will Increase: Even if you have limited responsibilities now, they tend to grow over time. Buying early ensures your future dependents are financially protected from the start.

- Peace of Mind Supports Better Decisions: With financial protection in place, you can make long-term decisions like investing or career moves with greater confidence, knowing your family is secure.

Take Note: Adding riders like critical illness or waiver of premium can strengthen overall protection. These options are usually more affordable to purchase when you are in your 20s. Delaying may lead to higher costs or limited availability, especially if health conditions arise later.

Buying Term Insurance in Your 30s: What Changes and Why It Still Makes Sense

- By your 30s, responsibilities like a spouse, children, or home loans make the need for life cover more real and immediate.

- You are more likely to get coverage based on real expenses like loans, family needs, and future goals, so you do not end up with insufficient coverage. Since responsibilities are higher, you may need a larger cover right away, increasing your overall commitment.

- Premiums are higher than in your 20s, so the same cover now costs more.

- Insurers may conduct stricter medical checks, and any existing health/lifestyle conditions can lead to counteroffers with higher premiums.

Take Note: There’s no one-size-fits-all answer when it comes to term cover. The right amount depends on your income, expenses, future goals, and liabilities, and this evolves as you move from your 20s into your 30s. For a clearer view, use this cover calculator to find the ideal cover for you.

How Age Affects Your Premium, Eligibility & Term Insurance Age Limit?

1. How Age Shapes Your Premium

Even small delays in buying a term policy can increase premiums over time. As you move into your 30s, insurers assess your health more closely, and any risks identified can lead to higher premiums through loadings.

Premium Comparison Across Profiles and Sum Assured

Note: The annual premiums shown are for a male, non-smoker profile, residing in Delhi, with coverage up to age 70 and no first-year discounts applied. The figures for Axis Max Life Smart Term Plan Plus are illustrative.

At 25, you can get a ₹2 crore cover for about ₹18,952, which is only slightly higher than what a 35-year-old pays for a ₹1 crore cover at ₹17,740. In simple terms, buying earlier lets you secure nearly double the coverage for almost the same price.

2. What Changes in Eligibility Over Time?

Approvals are quicker, and medical checks are minimal in your 20s. Hence, you have access to multiple term insurance plans and higher coverage options. Health and financial eligibility can get complicated in your 30s. Insurers may ask for detailed medical tests, and even minor conditions can affect pricing or lead to counteroffers.

3. Understanding the Term Insurance Age Limit

The minimum age for term insurance is 18 years, with the entry age between 18 and 65, and the maturity age going up to 85 or even 99 years. While you can buy later in your life, the cost increases, and the available term reduces. This makes early planning more practical and cost-effective.

20s vs 30s: A Quick Comparison to Help You Decide

Take a quick look at the infographic below for a better understanding.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Conclusion

Buying term insurance is about having the right term cover in place without delay. Choose a term plan that reflects your current responsibilities and future needs, instead of focusing only on premiums or age.

- If You Are Looking for Term Life Insurance in Your 20s: Starting early helps you lock in lower premiums and secure coverage before any health or lifestyle changes. However, this is not a one-time decision. As your responsibilities grow, review your cover regularly and increase it through life stage benefits or by adding another policy if needed.

- If You Want To Purchase a Term Life Insurance in Your 30s: Higher premiums should not hold you back. Delaying further can increase costs and make it harder to secure adequate coverage. With growing responsibilities, ensure your dependents are financially protected without waiting longer.

Ultimately, the emphasis should be on maintaining adequate and well-structured coverage that aligns with changing responsibilities and financial goals. If you are looking for a term plan from insurers with established track records, we recommend the best term insurance plans, which align with your family's needs.

Frequently Asked Questions

Last updated on: