The Axis Max Life term insurance calculator helps you instantly estimate how much premium you’ll pay based on your age, income, and sum assured.

If you're evaluating plans from the insurer, Ditto’s top pick is the Axis Max Life Smart Term Plan Plus, which offers competitive premiums across age groups. For example, a 25-year-old in Delhi pays around ₹10,000 for a ₹1 crore cover until age 65. The plan also offers standout features, such as Lifeline Plus for females, built-in terminal illness cover, a zero-cost exit option, and essential riders.

This guide is for anyone planning to buy term insurance and wanting quick premium estimates before applying. We’ll cover how to use the calculator, what affects your premium, and real sample pricing across age groups.

If you're planning to buy term insurance, one of the first questions you'll have is, ‘How much will it cost me?’

Many insurers offer online tools to help with this. One such tool is the Axis Max Life Term Insurance Calculator. It gives you a quick estimate of your premium based on your personal and financial details.

But to get an accurate estimate, you need to know what details to enter and how each one affects your premium. Let’s dive in.

Need help estimating your Axis Max Life term insurance premium? Book a call or chat on WhatsApp with our IRDAI-certified advisors.

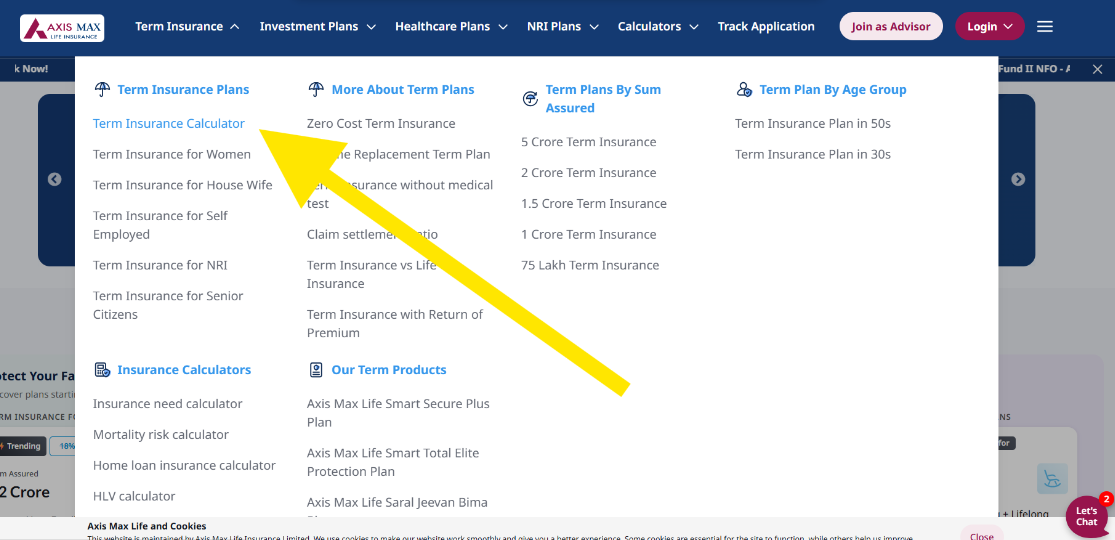

How to Use the Axis Max Life Term Insurance Calculator

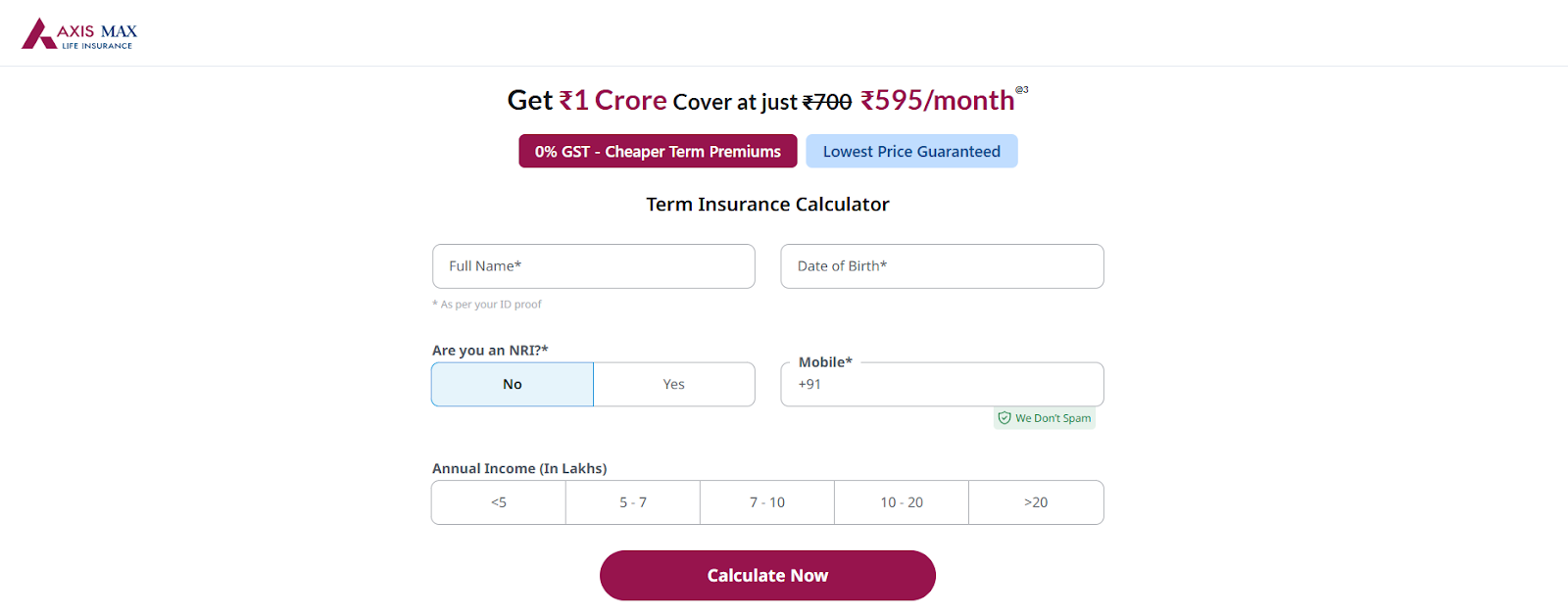

Step 3: Enter your basic details such as full name, date of birth, resident status, mobile number, and annual income. Click on ‘Calculate Now’.

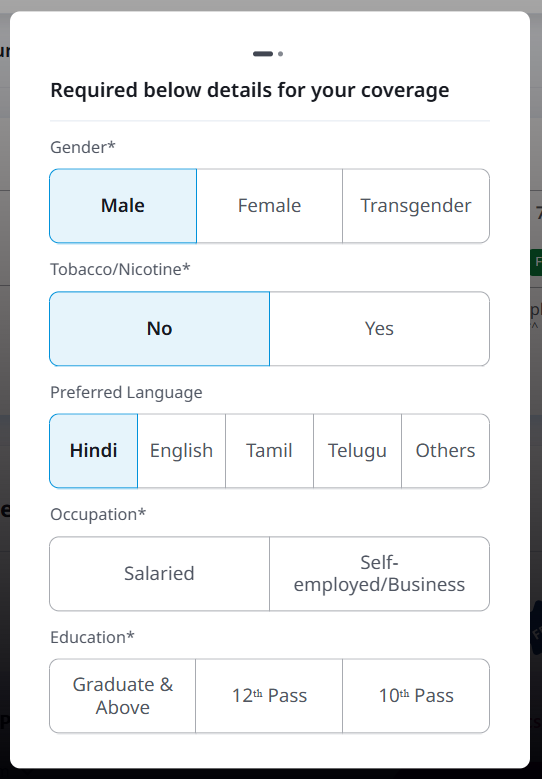

Step 4: Once redirected, enter your gender, smoking habits, preferred language, occupation, and education.

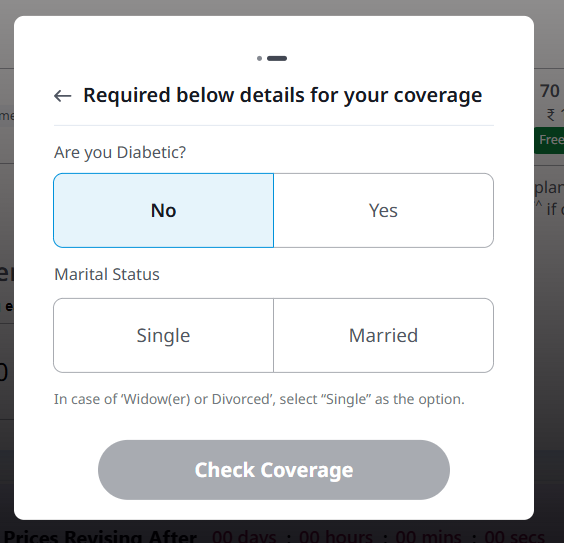

Step 5: Next, you’ll be asked to enter your health and lifestyle details. Mention details such as whether you have diabetes and your marital status.

Step 6: Now, you can check your premiums by entering the life cover (sum assured), policy term, and premium payment term, and preferred payment mode.

Step 7: Once you have your base premiums, you can also add the required riders and check the updated amount.

CTA

Factors That Affect Your Axis Max Life Premium

01

Age

Age is one of the biggest pricing factors insurance companies consider. Buying early can significantly reduce your premium because insurers consider younger individuals lower risk. Moreover, once you buy a term plan, your premiums stay locked in for life.

02

Sum Assured

The higher the life cover you choose, the higher your premium. However, premiums don’t increase proportionately with the sum assured. It’s recommended to choose a life cover after accounting for your financial liabilities, future expenses, and inflation. You can also use Ditto’s cover calculator on our website for help.

03

Policy Term

An ideal recommended policy term usually covers you until you’re 60 or 70, as this aligns with the retirement age for most individuals. This is the stage when most dependents become financially independent. Premiums tend to increase for policy terms beyond 70, especially for plans that extend to age 85 or 99 (whole life), since insurers price them based on life expectancy.

04

Smoking Status

Smokers pay significantly higher premiums, often 50% or more, because of the increased health risks associated with tobacco use. For example, a 25-year-old male smoker will have to pay around ₹18,000 annually for a ₹1 crore cover until age 65.

05

Health Conditions

Pre-existing conditions, such as diabetes, high blood pressure, or obesity, can increase your premium or lead to stricter underwriting. Insurers generally request medical tests before finalizing your policy.

06

Riders

Riders are add-ons that enhance your coverage but can also slightly increase your premiums. It’s crucial to choose only the ones that you truly need. At Ditto, we primarily recommend a critical illness rider, which pays a lump sum upon diagnosis of a listed illness. You can also opt for a waiver of premium rider, which keeps your policy active while waiving off future premiums if you’re diagnosed with a permanent disability or listed illness.

Note: Premium payment terms and payment modes also impact the overall premium outflow. At Ditto, we generally recommend the annual premium mode as it tends to be more cost-effective than monthly premium payments.

Sample Premium Estimates for Different Profiles

Profile

Sum Assured: ₹1 Crore

Sum Assured: ₹2 Crore

Sum Assured: ₹3 Crore

25, Male

₹10,160

₹17,222

₹25,218

25, Female

₹8,636

₹14,640

₹21,438

30, Male

₹12,296

₹20,656

₹30,405

30, Female

₹10,452

₹17,558

₹25,845

35, Male

₹16,114

₹26,552

₹39,285

35, Female

₹13,697

₹22,570

₹33,393

These estimates are for healthy individuals living in a tier-1 city like Delhi, covered for different amounts until age 65 under Axis Max Life Smart Term Plan Plus. The premiums are indicative and depend on the factors mentioned in the previous section.

Is Axis Max Life the Right Term Insurance Company for You?

Axis Max Life is one of the more popular insurers in India, especially for term plans. Here’s why it stands out:

High claim settlement ratio (99.62% for FY 22-25).

Strong amount settlement ratio (96.37% for FY 22-25).

Low complaint volume (5.67 per 10,000 claims for FY 22-25).

Competitive pricing across age groups.

Comprehensive plan options like Smart Term Plan Plus.

Multiple rider options for customization.

That said, the “best” insurer depends on your specific needs: premium budget, coverage requirements, and health profile. You can also refer to our guide to the best term insurance companies in India to make the right pick.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

The Axis Max Life Insurance term plan calculator is a great starting point for a quick premium estimate. But don’t stop there. Compare plans, understand features, and ensure your coverage truly fits your financial goals. A small step today, like checking your premium, can make a huge difference in your family’s financial security tomorrow.

Frequently Asked Questions

How do I use the Axis Max Life term insurance premium calculator?

Visit the Axis Max Life website, click on "Term Insurance," then select "Term Insurance Calculator" from the dropdown. Enter your name, date of birth, mobile number, annual income, and resident status, then click "Calculate Now." On the next screen, fill in your gender, smoking status, occupation, education, and health details, such as diabetes and marital status. Finally, enter your preferred sum assured, policy term, and premium payment term to see your estimated premium. This entire process typically takes just a few minutes to complete.

What is Axis Max Life Smart Term Plan Plus?

The Smart Term Plan Plus is one of Axis Max Life's flagship term plans and one of Ditto's top recommendations. It features competitive premiums. For example, a 25-year-old non-smoker male in Delhi pays around ₹10,000 annually for ₹1 crore of coverage until age 65. The plan includes built-in terminal illness cover, a zero-cost option, and support for essential riders, such as critical illness and waiver of premium. It is designed to offer both affordability and flexibility for different customer needs.

What factors affect my Axis Max Life term insurance premium?

Six main factors influence your Axis Max Life premium: age (younger buyers pay less and lock in rates for life), sum assured (higher coverage means higher premiums), policy term (longer coverage duration costs more), smoking status (smokers typically pay around 50% or more than non-smokers), pre-existing health conditions (like diabetes or hypertension), and optional riders (such as critical illness or waiver of premium add-ons). Even small changes in these factors can significantly impact your final premium quote.

How much does a 25-year-old pay for Axis Max Life Smart Term Plan Plus?

For a healthy, non-smoking 25-year-old male in a tier-1 city, Axis Max Life's Smart Term Plan Plus costs approximately ₹6,925 per year for ₹50 lakh coverage and ₹10,160 per year for ₹1 crore coverage. A 25-year-old female pays slightly less, around ₹5,887 for ₹50 lakh and ₹8,636 for ₹1 crore. These are indicative premiums for coverage up to age 65. These are indicative premiums for coverage up to age 65. Actual premiums may vary slightly depending on underwriting and individual profile details.

How much does a 30 or 35-year-old pay for ₹1 crore term insurance with Axis Max Life?

At age 30, a non-smoker male pays approximately ₹12,296 per year for ₹1 crore coverage under Axis Max Life's Smart Term Plan Plus, while a female pays around ₹10,452. By age 35, premiums rise to roughly ₹16,114 for males and ₹13,697 for females. These estimates assume coverage until age 65 for healthy individuals in a tier-1 city. The steady increase highlights how premiums rise with age even for similar coverage.

Does smoking status affect Axis Max Life term insurance premiums?

Yes, significantly. Smokers typically pay around 50% or more than non-smokers for the same coverage level with Axis Max Life. For example, a 25-year-old male smoker pays around ₹18,288 per year for ₹1 crore of coverage, compared to roughly ₹10,160 for a non-smoker of the same age. This premium loading reflects the higher health risks associated with tobacco use and is standard practice across all term insurers in India. Quitting smoking can help reduce premiums over time if declared truthfully.

What is Axis Max Life's claim settlement ratio?

Axis Max Life has a strong claims track record. For FY 2022-25, it maintained a Claim Settlement Ratio of 99.62% and an Amount Settlement Ratio of 96.37%, with a low complaint volume of just 5.67 per 10,000 claims. These metrics are among the best in the life insurance sector in India and are key reasons why Axis Max Life is considered a reliable option for term insurance buyers. To learn more about Axis Max Life’s claim settlement ratio, you can also refer to our detailed guide.

How much life cover should I choose in my term plan?

Your ideal life cover should account for your outstanding financial liabilities (such as a home loan), your family's future living expenses (adjusted for inflation), policy tenure, and any key future goals, such as children's education or marriage. Online tools like Ditto's cover calculator can help you arrive at a more precise figure based on your specific financial profile. Choosing insufficient coverage can leave your family financially vulnerable in the long run.

Should I buy term insurance early or wait?

Buying term insurance as early as possible is strongly recommended. Once you buy, your premiums are locked in for the entire policy term. A 25-year-old will pay significantly less per year than a 35-year-old for the same coverage, and those savings compound over decades. Additionally, if there are no pre-existing conditions, you are more likely to secure lower premiums compared to those who already have medical conditions. As age increases, the chances of developing health issues also rise, making it better to buy insurance when young and healthy.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.