Quick Overview

Term insurance is one of those decisions you make once, and then hope you never have to test. When a new, app-first company like ACKO enters the life insurance space, it naturally raises two reactions at the same time: “This looks refreshingly simple,” but “will this actually hold up 25 years from now?”

ACKO’s term insurance plan promises flexibility that most traditional insurers usually don’t: the flexibility to increase or decrease your cover, change policy term or premium payment term, and manage everything digitally without paperwork or agents.

It’s modern, convenient, and priced well. But life insurance is about trust, claims, and whether the insurer will deliver when your family needs it the most. So, where does ACKO really stand? Let’s find out.

Note: A simple term insurance checklist can help you compare insurers, check claim settlement ratios, and understand exclusions without feeling overwhelmed.

What are the Features of ACKO Term Insurance Plans?

Entry Age

Policy Tenure

Customizable Cover

Ease of Buying

ACKO Life Term Plan Riders

The ACKO term insurance plan offers a small but practical set of riders that can be added to the base term plan for extra protection. These are optional and increase the premium.

1) Accidental Death Benefit (ADB) Rider

This rider pays an additional sum assured if the policyholder dies due to an accident. For example, with a ₹1 crore base cover, the nominee would receive another ₹1 crore from this rider in case of accidental death (if selected). However, it is generally not recommended, since standard term insurance already covers accidental deaths. In most cases, increasing the base cover is a simpler and more cost-effective option.

2) Accidental Total and Permanent Disability (ATPD) Rider

If the insured suffers a serious accident leading to permanent and irreversible disability (such as loss of both limbs or eyesight), this rider provides a lump-sum payout. It also waives all future premiums, ensuring the policy continues without financial burden. This rider can be useful for people in high-risk occupations or those who travel frequently.

3) Critical Illness (CI) Rider

This rider pays a fixed lump sum on diagnosis of any one of 21 specified critical illnesses, such as cancer, stroke, kidney failure, or major organ transplant, etc., subject to waiting periods. It also comes with a waiver of premium benefit, meaning you don’t have to pay further premiums after a valid claim. The payout can be used for treatment, income replacement, or recovery-related expenses.

Note: ACKO does not offer terminal illness cover, instant claim payout on claim intimation, or auto cover continuance (temporary premium deferment during financial hardship). These features are available in most of the established insurers’ term plans now and can make a meaningful difference during medical or financial emergencies.

ACKO Term Insurance Premium Details

Your ACKO term insurance premium depends on your age, chosen cover amount, policy term, health and smoking status, occupation, selected riders, and payout option. That said, younger and healthier buyers usually pay lower premiums.

Premiums are calculated for a person seeking a ₹2 crore sum assured, with coverage up to age 70, for a non-smoking male, with no added riders or 1st year discounts.

ACKO Term Insurance Premiums

Insight: ACKO’s premiums for a ₹2 crore cover are generally lower than HDFC Life, Axis, and ICICI Pru (with Bajaj slightly cheaper), and since ACKO follows a direct-to-consumer, online-only model with no agents or offline sales, it saves on commissions, keeping premiums competitive but at the cost of personal advisor support during claims or servicing.

Documents Required to Buy ACKO Life Term Insurance

- Income Proof: Salary slips, Form 16, ITRs, & bank statements (Last 3-6 months).

- Identity & Address Proof: Aadhaar, PAN, passport, driving licence, voter ID, or utility bills.

- Age Proof: PAN card, birth certificate, passport, etc.

- Medical Reports (If Asked Based on Profile): CBC, HbA1c, lipid profile, TMT, chest X-ray, abdominal ultrasound, and past medical records.

If you want a more in-depth look at the kind of documents required for term insurance purchase, you can refer to the linked blog.

Things to Consider Before Buying an ACKO Term Insurance Plan

- ACKO Life is a new insurer, so there is no long-term public data available on its claim settlement performance. If long-term claim reliability is your top priority, choosing an established insurer may be a safer option.

- The plan does not offer a terminal illness benefit, which means there is no early payout if the insured is diagnosed with a life-threatening condition. Moreover, there is no auto cover continuance, health management services, or instant claim payout benefits.

- Coverage ends at the age of 70, which may be restrictive if you want insurance protection until 75 or 85.

- ACKO follows a fully digital, agent-free model, so there is no personal advisor support for servicing or claims.

- The plan isn’t widely listed or detailed on aggregator platforms, giving it limited market visibility and making it harder for users to compare features transparently with other insurers.

How to Buy ACKO Life Term Plans Online in 2026

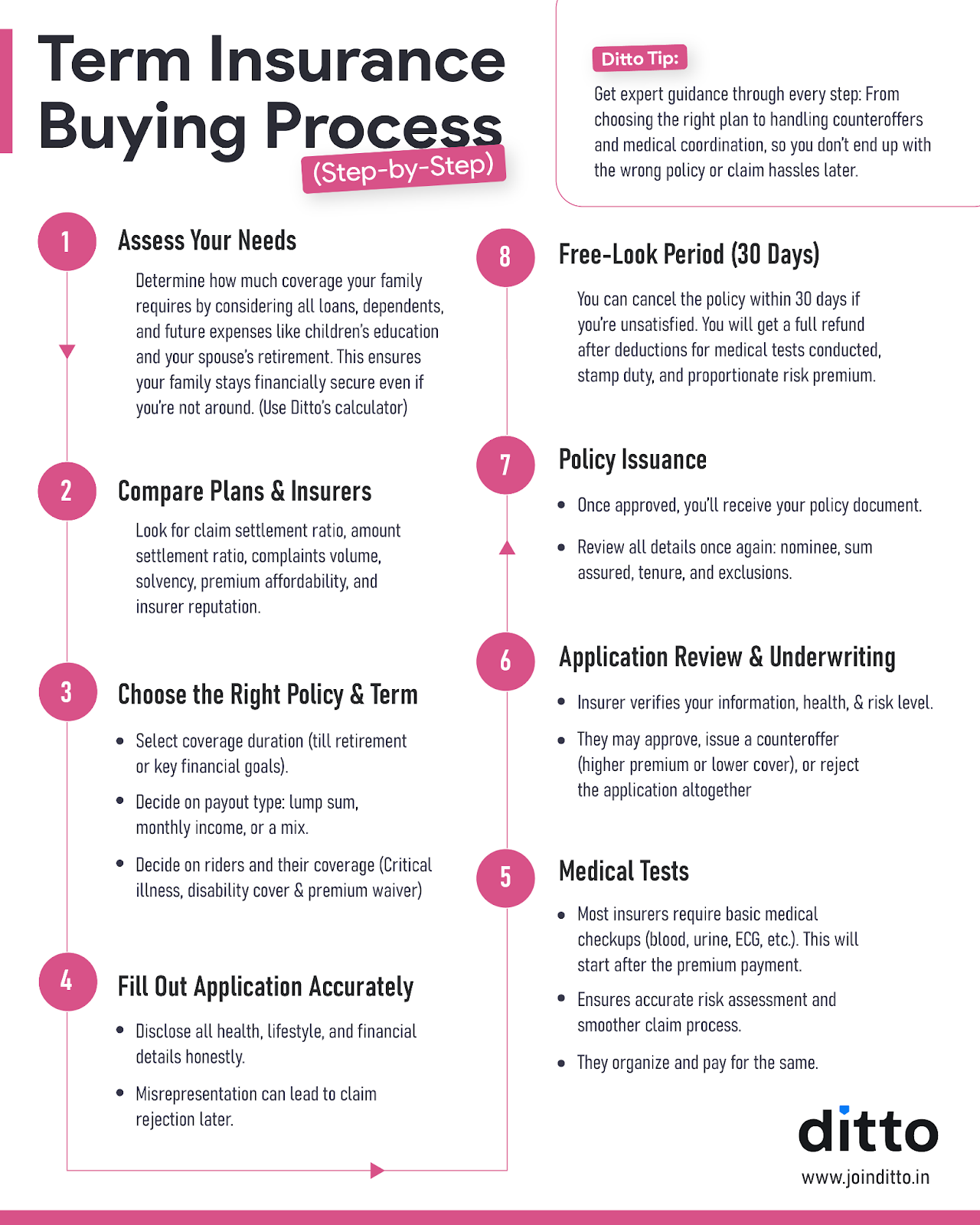

You can buy ACKO term insurance directly through the linked page. To know about the detailed purchase process of term insurance, check out the infographic below.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or text us on WhatsApp now!

Conclusion

ACKO term insurance brings a refreshing, modern approach to life cover. Backed by strong investors like Amazon and Accel and built by a company that has already simplified motor and health insurance, ACKO Life is clearly aiming to make term insurance easier, more flexible, and fully digital.

That said, life insurance is a promise that stretches across decades. And ACKO Life, despite its tech credentials, is still at an early stage, with limited public data on claim settlement performance, complaints, or long-term financial strength. While the product is modern, flexible, and affordable, it remains largely untested in real-world claim scenarios.

If you are looking for comprehensive term coverage that align your long-term goals, we recommend the best term insurance companies for 2026. Explore more about how our experts evaluate term plans through Ditto’s cut.

Frequently Asked Questions

Last updated on: