Wars bring destruction, uncertainty, and wide-reaching effects, and the latest tensions escalating in the Middle East are proof. Now, you might wonder what a conflict involving the United States, Israel, and Iran has to do with people living in India. But the honest answer is quite a lot.

You see, India imports 80-85% of its LPG from Gulf suppliers. Millions of Indians also live and work in the region. Our ships rely heavily on the Strait of Hormuz, one of the world’s busiest sea routes in the world, which is currently in danger. And many flights from India also transit Gulf airspace and hubs.

So when something disrupts the Middle East, the consequences rarely stay local. They tend to ripple outward through trade, travel, energy markets, and eventually even financial products like insurance.

A Quick Recap of What’s Happening

Travel and Trade Disruptions: The Fastest Insurance Impact

The conflict has already affected the aviation and shipping sectors. In early March 2026, large parts of Gulf airspace and key transit hubs experienced disruptions. Indian carriers such as IndiGo and Air India announced massive cancellations and suspensions on several Middle East routes.

This resulted in rebookings, delays, missed connections, and last-minute itinerary changes for passengers who use Gulf hubs to reach Europe and North America. Now, two things matter for insurance here:

Travel Insurance

A standard travel policy typically covers things like emergency medical expenses, baggage loss or delay, and travel delay benefits. However, many policies exclude war and war-like situations, with limited exceptions such as coverage for sudden acts of terrorism (subject to terms and conditions). So, any trip cancellation, curtailment, or evacuation driven by conflict, airspace closures, and security events may not always be covered in insurance, unless the policy wording or add-ons explicitly provide such protection.

Freight Risks

Shipping faces a different but equally important challenge. War-risk insurance for ships has tightened sharply for the Gulf and Hormuz corridors, with cancellation notices and premium spikes under discussion globally. Even India's reinsurer, GIC Re, reportedly withdrew marine hull war cover in several high-risk regions from early March 2026.

When war-risk cover gets pulled back or becomes more expensive, shipping companies often respond by rerouting vessels, charging higher freight rates, increasing cargo insurance costs, and extending delivery timelines.

For India, this can translate into costlier imports, especially fuel-related and time-sensitive goods. Exporters may also face delays and volatile shipping costs. And when freight costs rise, inflation often follows.

What Does it Mean for Your Term Life Insurance?

The Gulf is home to over 90 lakh Indians who work and live in countries such as Kuwait, Bahrain, Qatar, and other countries. If you or your family members are based there, here are a few things worth understanding about your term insurance:

Term Plans Typically Cover Death Due to War

Most term life insurance policies in India do cover death resulting from war or terrorist acts (unless specifically excluded in the policy contract). However, if a conflict escalates to a large-scale global disruption that severely affects financial systems or national stability, the practical settlement of claims could become more complicated. Situations like these fall into a gray area where operational disruptions can affect insurers.

Premiums May Fluctuate for New Buyers

For existing policyholders, the locked-in premium will remain unchanged. But if you are planning to buy a new term plan, there's a high chance that insurers may reconsider risk factors, especially for applicants who reside in or frequently travel to conflict zones. This doesn’t necessarily happen immediately, but prolonged geopolitical risks can influence underwriting decisions.

Restrictions on New Term Covers

In fact, the current situation has already led to temporary operational changes. Even if someone were to apply now, most insurers might postpone the application, stating that one can apply once the situation gets better.

Our partner insurers, HDFC Life, ICICI Prudential, and Axis Max Life, have already implemented a temporary halt on the sourcing of new business from the affected Middle East region. This applies to all life insurance products.

Hence, no new applications will be accepted from individuals currently located in, residing in, or sourcing the policy from the affected Middle East region until further notice. This move is expected to be followed by several other leading life insurers in India.

In this context, Middle Eastern countries refer to Bahrain, Cyprus, Egypt, Iran, Iraq, Israel, Jordan, Kuwait, Lebanon, Oman, Palestine, Qatar, Saudi Arabia, Syria, Turkey, the United Arab Emirates, and Yemen.

Quick Update

The Inflation Angle in Term Insurance

Here's a chain reaction that hits your term insurance, even if you have never set foot in the Middle East:

Inflation in India will likely rise due to a hike in crude oil prices (with 50% of imports over five years routed through Hormuz). This can make the sum assured of your existing cover feel inadequate because expenses may be higher 10 years from now. At the same time, global reinsurance costs may increase, and Indian insurers may pass some of that through to new policyholders via higher premiums.

If the rupee weakens against the dollar (which is already the case), imported medical equipment and some medicines get more expensive. That could raise healthcare costs and, in some cases, might increase health and mortality risk if treatment gets delayed. All this could impact how insurers price and underwrite new term cover, regardless of whether you are a resident Indian or an NRI.

But there’s a hidden benefit: Once a term plan is purchased, premiums are fixed for the entire coverage duration as mandated by the IRDAI.

What About Your Health Insurance?

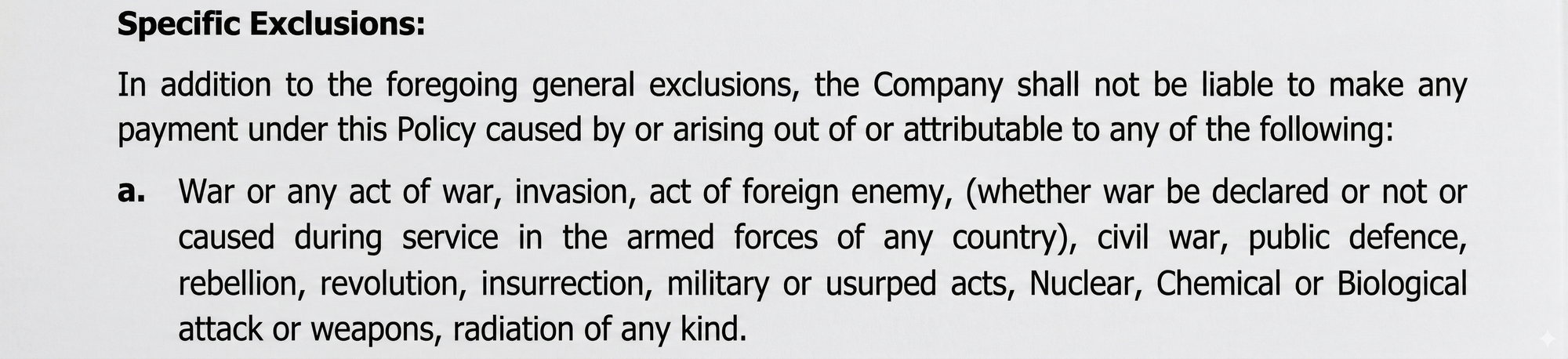

War or any act of war is excluded under most health insurance plans, and it is usually listed clearly in the exclusions section. Terrorism, however, may be covered in many health plans depending on the insurer and policy wording.

This is how war/terrorism exclusion is framed in an Indian health insurance policy (domestic coverage):

Let’s understand this further by considering 2 scenarios:

Scenario 1: You and Your Family Are in the Gulf

If any family member of yours is in the Middle East and is hospitalized due to the ongoing Iran-Israel war, here are some facts to be aware of:

- Standard health insurance policies cover hospitalization only in India. So if your policy does not have an international cover add-on, hospital bills abroad will not be reimbursed.

- Group health insurance provided by some employers may include international coverage. It’s best to check the policy document carefully.

- If you are in the Gulf for a short period, it's generally advisable to buy a customized travel insurance plan. Make sure to check the policy document for exclusions related to war-like situations to be on the safer side.

Scenario 2: You Are in India And You Have Health Insurance

Even if you are far from the conflict zone, your health insurance can still feel the effects indirectly.

- Premiums May Likely Rise at Renewal

We already talked about the war and oil spike angle earlier, which leads to inflation. Since healthcare costs also increase during this time, insurers notice this and eventually adjust pricing during policy renewals. In fact, medical inflation is one of the primary reasons behind increasing premiums in health insurance, alongside age and location.

- Your Sum Insured Might Become Inadequate

Here's a question worth asking yourself: If crude oil prices rise significantly and hospital costs jump up by 20-25% over the next few years, will your ₹5-10 lakh sum insured be enough for a major hospitalization in 2027? For many families, the answer may be no. That’s why we generally recommend a minimum cover of ₹15-25 lakh in India to avoid black swan events (rare, unpredictable occurrences that impact your financial situation), medical inflation, or difficulty in increasing the sum insured after being diagnosed with a health condition.

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or chat on WhatsApp with us now!

The Big Picture: What Should You Actually Do?

By now, it’s clear that the US-Israel-Iran conflict has and will have a real impact on the Indian insurance sector. But we don't want to alarm you. India has experienced such geopolitical shocks before (e.g., the Russia-Ukraine war in 2022), and the insurance market has managed to function through them all. Still, these moments remind us of an important lesson: people who plan ahead are usually better protected.

So here’s a simple checklist to help you overcome the current scenario:

- Review your term plan's exclusions, especially if you travel to or have family in the Middle East.

- Don’t let your health insurance policy lapse. Set up auto-pay if you haven’t.

- If any family member is in the Gulf, check the inclusions and exclusions of their health cover. If you are planning to visit any of those countries, get travel insurance and review its coverage and exclusions.

- International health insurance plans have their own limitations, and some do not provide coverage for specific countries. So, choose your policy wisely and seek an expert's advice, if needed.

Disclaimer

Frequently Asked Questions

Last updated on: