Quick Overview

PNB MetLife’s ULIP plans offer fund choices, flexibility, and long-term investment potential. At the same time, they come with market-linked returns, policy charges, a 5-year lock-in, and lower insurance cover compared to a pure term plan.

In this guide, we break down the key plan features, costs, and trade-offs and compare them with alternatives like term insurance so you can decide what truly aligns with your financial goals.

ULIP Plans Offered by PNB Metlife Life Insurance

Note: Systematic Transfer Strategy (STS) is a feature in ULIPs where your money is initially invested in low-risk funds (like debt funds) and then gradually shifted to higher-risk funds (like equity funds) over a fixed period. This helps reduce the impact of market volatility and allows you to enter equity markets in a more disciplined manner instead of investing everything at once.

PNB Metlife Life Insurance: Performance Metrics

Note: The above metrics reflect the overall performance of PNB MetLife Life Insurance and are not limited to its ULIP portfolio.

Key Insights:

- Strong Claims Reliability: The insurer’s Claim Settlement Ratio improved from 99.09% in FY 2022-23 to 99.57% in FY 2024-25, with a three-year average of 99.29%. This indicates strong claims performance overall.

- Improving Payout Quality: The Amount Settlement Ratio has increased over time, which suggests a larger share of claim amounts are being paid out.

- Meaningful Operating Scale: PNB MetLife appears to operate at a healthy scale relative to the industry benchmark shown above.

- Complaint Levels Remain a Watchpoint: Complaint volumes have historically been high, although the article notes a sharp drop in FY 2024-25.

- Adequate Financial Stability: The solvency ratio remains above the IRDAI requirement of 1.5x, which indicates acceptable financial stability, though it is not especially high versus some peers.

Note: These metrics reflect the insurer’s overall performance and do not necessarily indicate that its ULIP plans are the best choice for every investor.

Premium Illustration for PNB MetLife ULIP Plans

Note: Projected values are illustrative and depend on fund performance, mortality charges, policy administration charges, and fund management fees. ULIP returns are not guaranteed and can vary based on market performance. The figures are extracted from the Smart Platinum Plus brochure.

Drawbacks of Buying a PNB MetLife Life Insurance ULIP Plan

1. Market-Linked Risk: Returns from ULIPs depend on the performance of the underlying equity or debt funds. Since these are market-linked investments, returns are not guaranteed and can fluctuate based on market conditions.

2. Multiple Charges: ULIPs include several charges, such as premium allocation charges, fund management charges, mortality charges, and policy administration charges. Over time, these costs can significantly reduce the overall returns compared to investing directly in low-cost instruments like mutual funds.

3. Mandatory Lock-in Period: ULIPs come with a 5-year lock-in period, during which withdrawals are restricted. This makes them less flexible compared to many other investment options.

4. Lower Insurance Coverage: Compared to pure protection products like term insurance, ULIPs offer lower life coverage relative to the premium paid, since a portion of the premium is allocated toward investments.

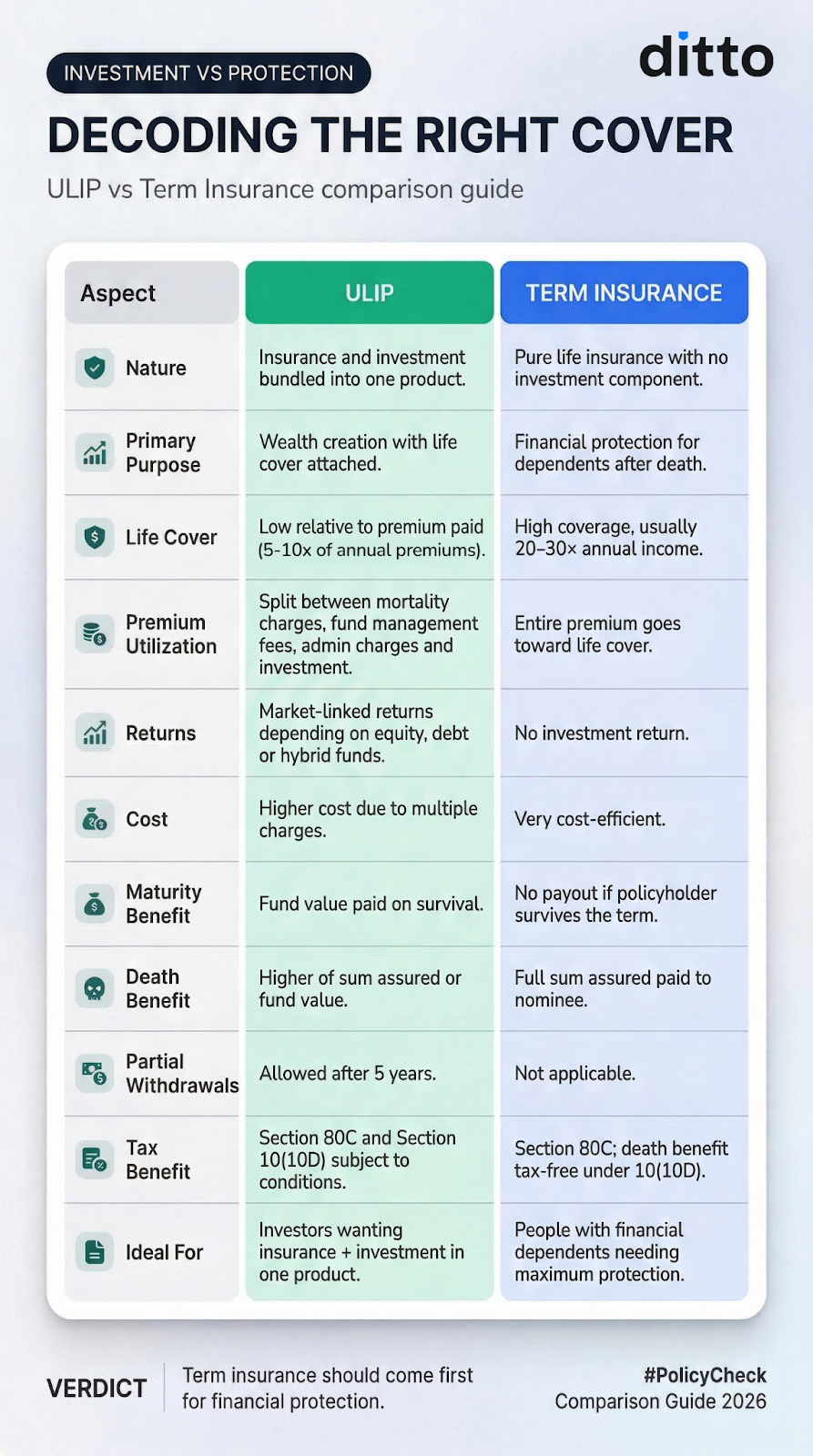

ULIP vs. Term Insurance: Which Is Better?

You may also refer to our detailed guide on ULIP vs term insurance for a clearer comparison of both options.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Ditto’s Take on PNB MetLife

ULIPs from PNB MetLife may appeal to individuals who prefer a single product combining insurance with market-linked investments. Plans like Smart Platinum Plus, Mera Wealth Plan, and Smart Goal Ensuring Multiplier offer exposure to equity and debt funds along with life cover.

However, based on our experience, these plans are not always the most efficient way to manage protection and wealth creation. They involve market risk, multiple charges, and a lock-in period, which can reduce flexibility and returns.

A ULIP may still suit someone comfortable with market risk, planning to stay invested long-term, and valuing tax-efficient switching. That said, we generally recommend separating the two goals by opting for a term plan and investing the rest separately.

Frequently Asked Questions

Last updated on: