Overview

According to the Economic Times, India’s group credit life insurance segment has already grown into a ₹30,000 crore premium market in 2025 despite being relatively young. Its rapid growth highlights how lenders and borrowers increasingly use loan protection cover to protect outstanding debts.

This guide explains how loan protection insurance works, what it actually covers, where it adds value, the key costs, exclusions, and trade-offs borrowers should understand before buying.

What Is Loan Protection Insurance?

Loan protection insurance is designed to help repay an outstanding loan if the borrower dies, suffers a permanent disability, or is diagnosed with a covered critical illness.

In India, most loan protection policies are offered as group insurance products through banks and lenders at the time of taking a loan. Examples include plans like ICICI Pru Group Term Plus. However, for group loan protection plans, Goods and Services Tax (GST) is charged on the premium at the applicable rates, making the policy more expensive.

Loan protection plans generally come in two formats.

1) Reducing Cover: The cover decreases as the outstanding loan balance falls, making it suitable for loan repayment protection.

2) Level Cover: The cover remains unchanged throughout the policy term, providing an additional payout to the family even after the loan is fully cleared, which is why it's more expensive.

Did You Know?

How Does Loan Protection Insurance Work?

The primary objective is to protect both the borrower's family and the lender from the financial impact of an unpaid loan. Here’s how the insurance works:

- The borrower is the insured person under the policy.

- If the borrower dies during the policy term, the insurer pays the eligible claim amount.

- In group loan protection plans, the insurer will first pay the outstanding loan balance to the lender.

- Any claim amount remaining after the loan is fully repaid is paid to the nominee.

Note: In group loan insurance plans, the insurer usually settles the claim directly with the lender, who serves as the master policyholder or beneficiary under the policy structure. In individual loan protection plans, the borrower can assign the policy to the lender under Section 38 of the Insurance Act, 1938.

Types: Home, Personal, and Car Loan Cover

What It Costs and What It Excludes

The cost of loan protection insurance varies from borrower to borrower. Premiums are influenced by factors such as the loan amount, loan tenure, borrower’s age, health condition, and the type of cover chosen. Policies with level cover, joint-life cover, or add-ons like critical illness, disability, accidental death, or EMI protection generally cost more.

Many lenders also offer a single-premium option that is added to the loan amount. For example, if a ₹50,000 single-premium loan protection policy is financed into a 20-year home loan at 9%, the EMI could increase by about ₹450 per month. Over the full tenure, the borrower may repay nearly ₹1.08 lakh, more than double the original insurance premium.

While this may seem convenient, it increases the overall borrowing cost because interest is charged on the financed insurance premium as well. Most loan insurance plans in India are group plans. Here is an example of a group term plan from ICICI Prudential.

Sample Premiums

Using ICICI Prudential's Group Term sample rate of 2.237 per ₹1,000 of sum assured for a 35-year-old borrower, the estimated base annual premium for a ₹50 lakh life cover is around ₹11,185. This is only a sample illustration and excludes applicable taxes, lender mark-ups, policy fees, and insurer-specific pricing adjustments.

Note: Loan protection insurance plans have exclusions like suicide in the first year, death due to involvement in illegal activities, which must be checked before buying.

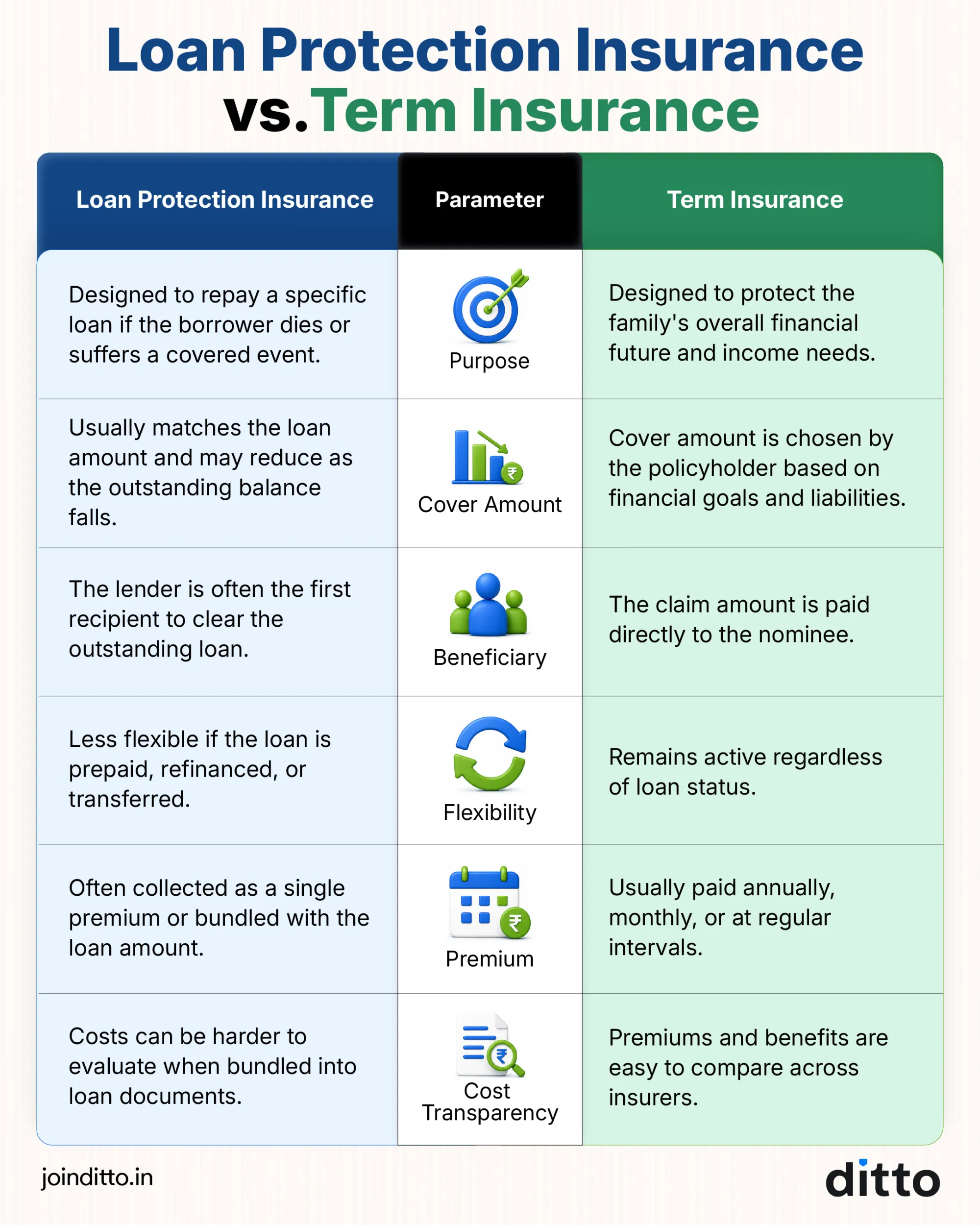

Loan Protection Insurance vs. Term Insurance

Loan protection insurance and term insurance serve different purposes. Loan protection insurance is designed to clear a specific debt, while term insurance aims to protect your family's overall financial future.

See the infographic for a clear understanding.

Do You Actually Need Loan Protection Insurance?

Loan protection insurance is not essential for every borrower. In many cases, a sufficiently large term insurance policy can achieve the same objective while offering broader family protection. However, loan protection cover may deserve consideration in the following situations:

- It makes sense when you already have a large term insurance cover for your family's financial needs and simply want a separate policy dedicated to clearing the home loan. This helps offset the loan liability without reducing the portion of the term insurance payout intended for your family's future expenses and goals.

- If automatic loan closure on death is a priority, and the borrower or family places a high value on the certainty that the loan is cleared without requiring the nominee to coordinate repayment.

- The premium compares favorably with that of a standalone term plan, and the prepayment and premium refund terms are transparent.

- The lender allows external insurance, but the borrower values the convenience of a loan-linked solution.

- Certain borrowers with existing conditions like diabetes or heart disease, older age at entry, or high-risk occupations may find standalone term insurance expensive or declined by underwriters. In these cases, group credit life insurance (which typically uses simplified underwriting) may be the more accessible option.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 24,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat over WhatsApp with our advisors.

Conclusion

Loan protection insurance works best when it is voluntary, transparent, fairly priced, and genuinely aligned with the loan being protected. Problems arise when it is bundled without clear consent, financed into the loan without full disclosure, sold with restrictive exclusions, or mistaken for complete family protection.

For most borrowers, a personal term insurance plan remains the more practical solution. If required, the policy can be assigned to the lender as additional security.

At Ditto, we recommend a cover of ₹1 to ₹2 crore, which strikes a balance between affordability and adequate protection. The sum assured covers not just the loan but also your family's broader financial needs. To get a better understanding, use this cover calculator to find the ideal cover for you.

If you're evaluating protection options, it is worth exploring the best term insurance plans available today to ensure your family's future and outstanding loan obligations remain protected even if you are not around.

Frequently Asked Questions

Last updated on: