Quick Overview

Life Insurance Corporation of India (LIC) is the country’s largest life insurer, established in 1956 as a government-owned entity. With a dominant market share and a vast distribution network of over 14 lakh agents, LIC has built a strong reputation for trust and reliability across India.

Its ULIP portfolio is designed for individuals looking to combine long-term wealth creation with life insurance, offering multiple fund options, flexible premium structures (across plans), and market-linked returns.

This guide explains how LIC ULIP plans work, their key features, and how they compare in terms of flexibility, costs, and overall value.

LIC: Performance Metrics

Note: These metrics apply to the entire LIC life insurance portfolio, not just its ULIPs.

Insights:

- CSR is slightly below average but still shows a strong, consistent claims record at scale, which means that most genuine claims are paid out.

- ASR is above average, meaning LIC usually pays claims in full, regardless of size.

- Complaint levels are far below average, indicating a smoother claims experience.

- Business volumes are significantly higher than peers, highlighting LIC’s massive scale.

- The solvency ratio is slightly below average but remains within the safe regulatory limit of 1.5x.

Popular ULIP Plans Offered by LIC

Premiums for LIC ULIP Plans

Note: The projected values are illustrative for a 30-year-old. Actual returns are not guaranteed and will depend on market performance. The figures are extracted from the LIC Nivesh Plus ULIP brochure, where you will find more information on the ULIP plan returns.

Drawbacks of Buying a LIC ULIP Plan

Multiple Charges Reduce Effective Returns

LIC ULIPs come with several layers of charges, premium allocation, fund management, policy administration, and mortality charges. Even if the underlying fund generates decent returns, these costs can significantly reduce your effective long-term returns.

Life Cover is Often Insufficient

Most LIC ULIPs offer life cover of around 7–10× the annual premium. This is far below what a family actually needs, especially when compared to term insurance, which can offer much higher coverage (20-30x annual income) at a lower cost.

Five-Year Lock-In Limits Liquidity

All LIC ULIPs have a mandatory 5-year lock-in period. During this time, you cannot withdraw your money freely, which makes them unsuitable if you might need liquidity in the short term.

Limited Flexibility Compared to Alternatives

You’re restricted to LIC’s available fund options and switching rules. Unlike mutual funds, you cannot freely diversify, increase investments (in some plans), or optimise allocation dynamically.

Combines Insurance and Investment Inefficiently

LIC ULIPs bundle insurance and investment into one product, which often leads to compromises on both fronts: lower life cover and reduced investment efficiency. Separating term insurance and investing typically offers better outcomes.

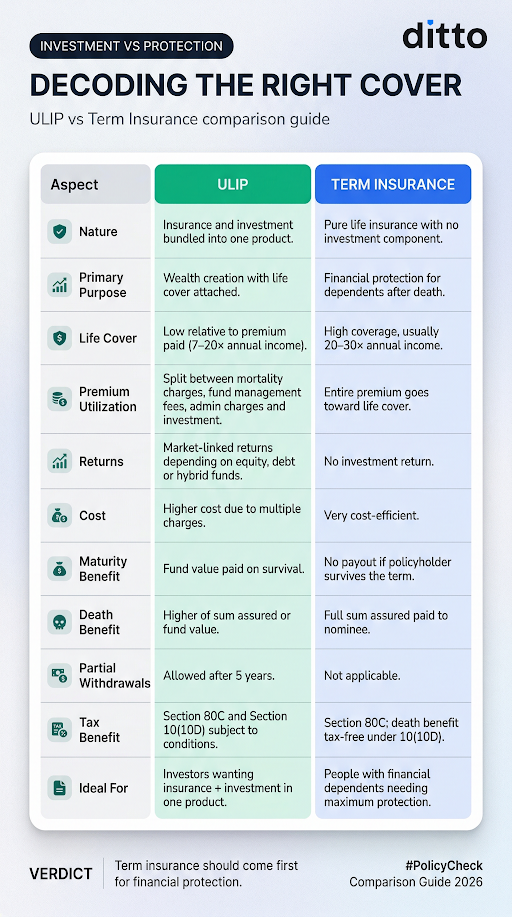

ULIP vs Term Insurance: Which One Should You Choose?

If you’re comparing ULIPs and term insurance, the key is to understand how they differ in purpose, cost, and overall outcomes. We’ve covered this in detail in the infographic.

In simple terms, it comes down to a choice: go for a bundled product that combines insurance and investment, or keep them separate to maximise both protection and returns. For a deeper dive, check out our full guide on ULIPs vs term insurance.

Numerical Illustration Based on LIC ULIP Plans

1) Life Cover

- LIC Digi Term Plan ₹50 lakh cover for around ₹4,700/year (exclusive of taxes)

- LIC Index Plus (ULIP) Life cover = 7x to 10x annual premium ₹1,00,000/year → cover of ₹7–10 lakh

A term plan gives significantly higher coverage at a much lower cost.

2) Returns

LIC’s 25-year illustration for Index Plus shows:

- 8% gross return → around 6.30% net yield

This drop is due to:

- Fund management charges

- Policy admin costs

- Mortality charges

While ULIPs participate in the market, actual returns are lower after costs. Term insurance delivers high, cost-effective protection. That’s why term plans are typically the cleaner choice for protection, while ULIPs should be evaluated separately as investment products.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

LIC ULIPs offer a familiar, trust-backed way to combine investing and insurance, with options across lump sum and regular premium plans, multiple fund choices, and guaranteed additions in select products. However, these plans come with trade-offs: relatively low life cover, multiple charges, and limited flexibility that can impact long-term returns.

At Ditto, we don’t recommend ULIPs since combining insurance and investment often leads to compromises on both fronts. A term plan + separate investments in low-cost avenues like mutual funds, NPS, PPF, FDs, etc., typically provides better protection and more efficient wealth creation.

If you specifically value LIC’s brand and backing, a better alternative could be pure protection plans like LIC Digi Term Plan or LIC Bima Kavach, which offer straightforward life cover without mixing it with investments. If your goal is protection, shortlist a pure term plan first. If your goal is wealth creation, compare ULIPs against mutual funds before locking yourself into a bundled product.

Disclaimer: LIC is not a partner insurer of Ditto. All information in this article has been obtained from publicly available sources and is for educational purposes only.

Frequently Asked Questions

Last updated on: