Overview

Many people searching for LIC investment plans want to know whether it is possible to double their money in 5 years. While LIC offers several savings and insurance products, understanding the difference between policy term, premium payment term, guaranteed benefits, and actual returns is essential before evaluating such claims.

In this article, we separate facts from marketing myths, explain how LIC plans really work, and explore alternatives available to investors seeking short-term growth and capital protection.

Does LIC Have a Plan That Doubles Your Money in 5 Years?

No. LIC does not currently offer any mainstream savings or insurance plan that can realistically be described as a guaranteed "double your money in 5 years" product.

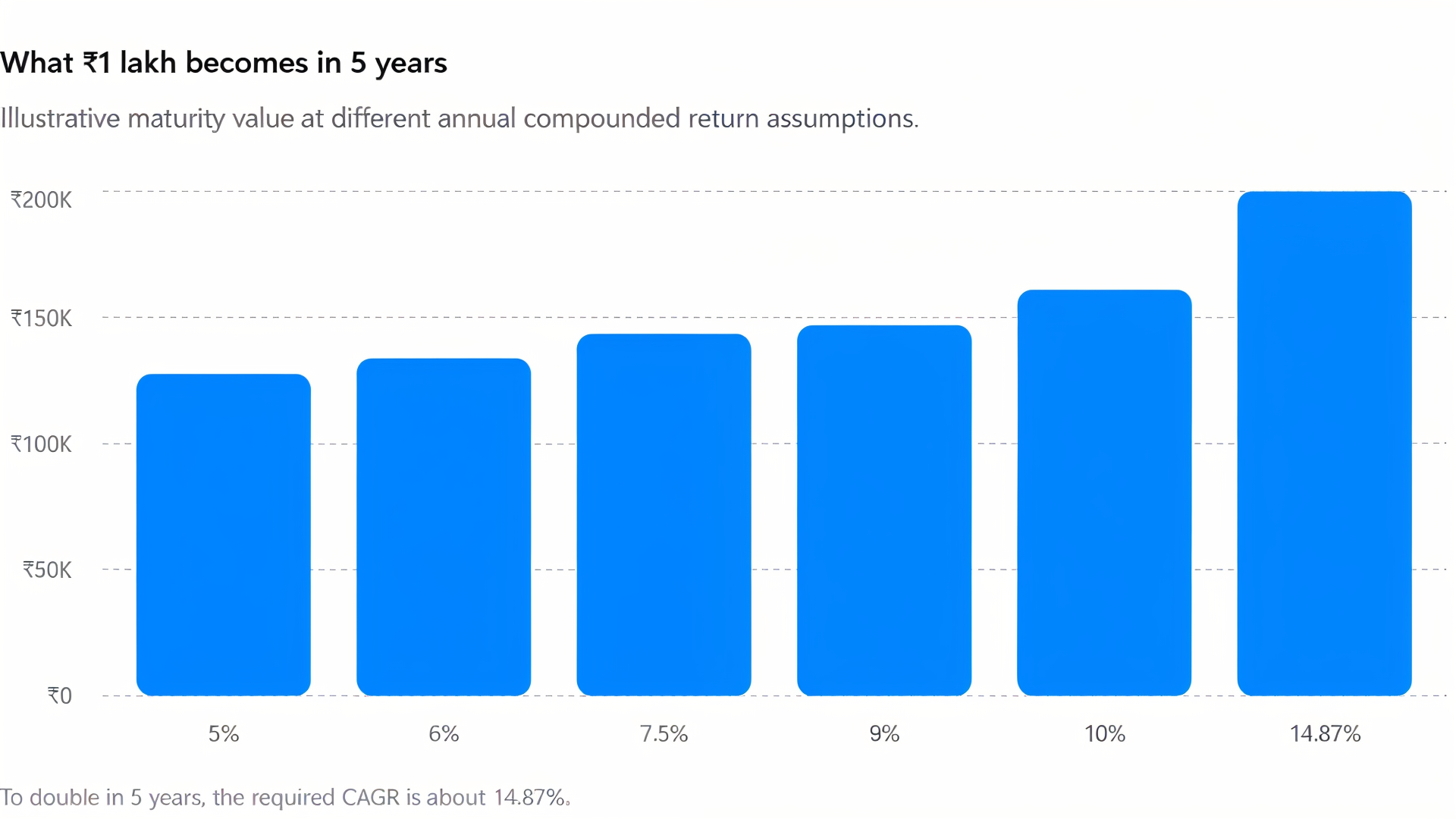

To double an investment in 5 years, you would need an annual return of roughly 14.9%. Here’s an illustrative example of how math works with an investment of ₹1 lakh.

Returns of around 14–15% per year usually require meaningful exposure to equities. Over the past 5 years, some small-cap and mid-cap stocks and indices have delivered returns in this range or higher, as per the National Stock Exchange (NSE) Indices.

However, such returns are market-driven and come with volatility and risk. Traditional LIC savings plans focus on capital protection and stability, which is why they are generally not designed to double your money within 5 years.

Note: The commonly used Rule of 72 estimates the return needed to double money. Dividing 72 by 5 years gives roughly 14.4% per annum. A more precise Compounded Annual Growth Rate (CAGR) calculation shows that doubling money in 5 years requires an annual return of about 14.87%.

LIC Plans With Shorter Tenures (5-Year or Near)

LIC does not currently offer any active savings, endowment, money-back, pension, or investment-oriented plan that offers the guarantee to double your money in 5 years. While some LIC term insurance plans may offer shorter policy durations, they are pure protection products and do not provide maturity benefits or investment returns.

However, certain LIC plans may help accumulate value over time through guaranteed additions, simple reversionary bonuses, final additional bonus, or deferred income benefits.

Note: Agent-led sales often frame LIC maturity payouts as “double the premiums paid,” especially for low-awareness customers. This oversimplifies how the policy works and may lead buyers to expect returns that are not guaranteed in practice.

Key Features of LIC Short-Term Plans

Limited Premium Payment

Pay premiums for a shorter period, such as 5 years, while the policy may continue for much longer. However, a short premium term does not mean a short investment tenure.

Single Premium Option

Make a one-time investment upfront. Suitable for lump-sum investors, but returns should be compared with other low-risk alternatives.

Life Insurance Cover

Provides a death benefit (usually up to 10x annual premiums) along with savings, though pure term insurance usually offers higher coverage at a lower cost.

Guaranteed Additions

Fixed additions may accrue as per policy terms. These should not be confused with annual investment returns.

Participating Bonuses

Some plans may earn bonuses declared by LIC. Future bonuses are not guaranteed and can vary over time.

Policy Loan Facility

Loans may be available against the policy after certain conditions are met, subject to interest charges.

Surrender Value

Early exit is possible, but it can significantly reduce overall returns and benefits.

What Returns Can You Realistically Expect?

For traditional LIC savings plans, return expectations should generally be moderate rather than equity-like.

- In many endowment, money-back, and similar savings plans, the effective long-term return often falls in the low-to-mid single-digit range, depending on several factors.

- These factors include policy term, age at entry, premium amount, bonus declarations, guaranteed additions, and whether the policy is held until maturity.

- More importantly, do not judge returns based only on the sum assured or advertised benefits.

- The best way to evaluate a policy is by calculating its actual Internal Rate of Return (IRR) using all premiums paid versus all benefits received over the policy term.

LIC's traditional plans deliver approximately 4.5% to 6% effective IRR post-tax, depending on policy term, sum assured, and bonuses, if any. Furthermore, if we go by the rule of 72, and let’s assume 5% IRR, the years it will take the money to double is 14.4.

Note: You can upload your benefit illustration into a Large Language Model (LLM) chatbot and ask it to calculate the policy's Internal Rate of Return (IRR). In most cases, this provides a reasonably accurate estimate and can help you evaluate the plan more objectively before investing.

Did You Know?

LIC Short-Term Plans vs Other Investment Options

Who Should Consider These LIC Plans?

- Very Conservative Investors: May find these plans suitable if capital stability, predictable benefits, and the comfort of a well-known insurer matter more than maximizing returns.

- People Who Struggle to Save Regularly: The long-term commitment and restricted access to funds can help create disciplined savings habits, though this comes at the cost of flexibility.

- Investors Seeking Insurance Plus Savings: These plans can work as a supplementary savings tool alongside insurance needs, especially for those who prefer an all-in-one product.

However, those expecting their investment to double in 5 years should look elsewhere, as traditional insurance plans are designed for stability rather than high growth.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 24,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Ditto’s Verdict

Claims that an LIC plan can guarantee your money will double in 5 years do not hold up mathematically. A doubling period of 5 years requires returns of 14.87% per annum, which traditional LIC savings plans are not designed to deliver. In many cases, the "5 years" refers only to the premium payment term, while the policy itself runs much longer.

Certain life insurance products like Unit Linked Insurance Plans (ULIPs) can potentially deliver higher returns because of their market-linked nature, but those outcomes are neither guaranteed nor predictable. Higher equity exposure brings higher risk, and policy charges can meaningfully reduce long-term returns. Always evaluate the actual benefit illustration and expected IRR rather than relying on headline claims. More importantly, separate your life protection needs from your investment goals when assessing any financial product.

Term insurance is generally the most cost-effective way to secure a high life cover, while investment options such as mutual funds, NPS, PPF, and FDs offer transparent return structures that make it easier to build wealth and track performance over time.

Frequently Asked Questions

Last updated on: