Overview

Choosing a ULIP involves more than comparing projected maturity values. Your actual returns depend on factors such as the fund you select, the policy charges deducted over time, and market performance.

In this guide, we'll explain how the LIC Nivesh Plus Returns Calculator works, how to interpret the 4% and 8% benefit illustrations, and the key factors that can influence your maturity value, helping you make a more informed investment decision.

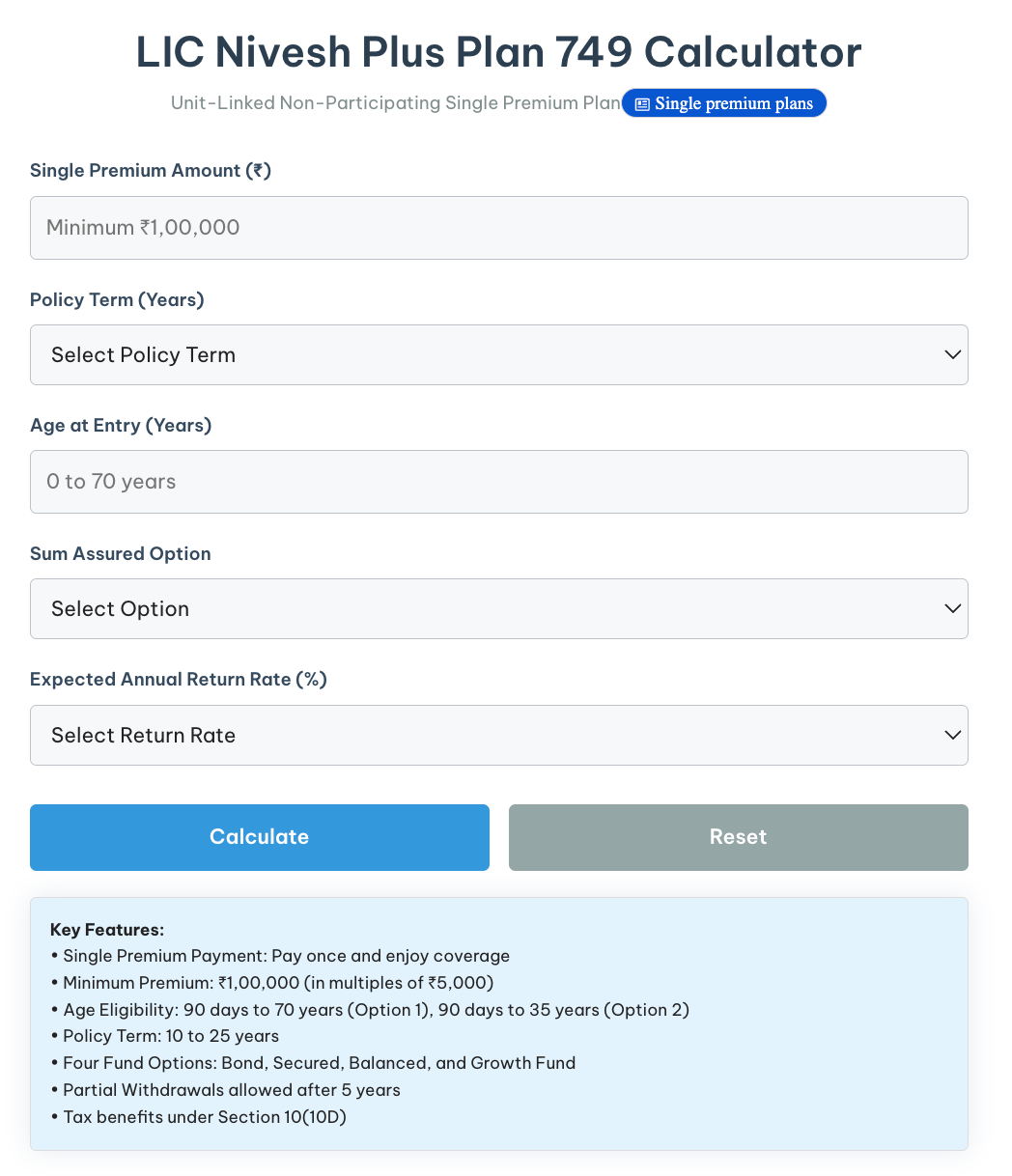

What Is the LIC Nivesh Plus Returns Calculator?

The LIC Nivesh Plus Returns Calculator is a tool that helps estimate the potential maturity value of your policy based on factors such as your single premium amount, policy term, fund option, and sum assured choice.

If you want a personalized estimate, you can generate a quote on the LIC website by entering your investment amount and policy details. LIC will then provide a personalized benefit illustration based on the information you enter.

Several third-party informational websites also offer LIC Nivesh Plus calculators to estimate returns. However, these tools rely on assumptions about policy charges, illustration rates, and sum assured options. Therefore, their projections should be treated as estimates and not as guaranteed maturity values or official benefit illustrations.

Note: The product brochure also includes standard benefit illustrations at 4% and 8%, based on sample assumptions and intended only for illustration.

How to Use the Calculator?

To estimate your projected maturity value, enter the following details:

- Entry age

- Single premium amount

- Policy term

- Sum assured option

- Expected annual return rate

The calculator will estimate your maturity value based on the details provided. Compare the projections at 4% and 8%, as these are the standard illustration rates prescribed for ULIPs by IRDAI.

Keep in mind that these are hypothetical illustration rates. They are not guaranteed returns, are not fund-specific, and do not represent the minimum or maximum returns you can earn. Your actual maturity value will depend on factors such as the fund's NAV performance, market conditions, policy charges, and other applicable deductions.

LIC also states that it does not authorize anyone to make projections about future ULIP fund performance beyond the prescribed 4% and 8% benefit illustrations.

Fund Options and Sum Assured Choices

LIC Nivesh Plus offers four investment funds with different levels of equity exposure and risk. Your choice of fund determines how your premium is invested and can significantly influence your long-term returns.

Generally, funds with higher equity exposure have the potential for higher returns but also carry greater market risk, while funds with lower equity exposure tend to be relatively more stable.

The Bond Fund invests only in debt securities and is suitable for conservative investors seeking lower risk. The Secured Fund maintains limited equity exposure, offering a balance between stability and growth. The Balanced Fund allocates a larger portion to equities, making it suitable for investors with a moderate risk appetite. The Growth Fund has the highest equity exposure and is intended for investors willing to accept higher market volatility in pursuit of potentially higher long-term returns.

LIC Nivesh Plus offers two sum assured options:

- Option 1: Basic sum assured is 1.25 times the single premium. This option is available for applicants up to 70 years of age.

- Option 2: Basic sum assured is 10 times the single premium. This option is available only for applicants up to 35 years of age.

Option 2 provides significantly higher life insurance coverage. However, it also attracts higher mortality charges, which can reduce the maturity value compared with Option 1, assuming all other factors remain the same. Your choice between the two options should depend on your age, insurance needs, and investment objectives.

Charges That Affect Your Returns

The LIC Nivesh Plus Returns Calculator can overstate your returns if you look only at the assumed growth rate. Your actual maturity value is reduced by various policy charges deducted during the policy term.

These include:

- Premium Allocation Charge: 3.30% for offline purchases and 1.50% for online purchases.

- Fund Management Charge (FMC): 1.35% per year across all four fund options.

- Mortality Charge: Varies based on the policyholder's age and the sum at risk.

- Rider Charges: Applicable if you opt for any available rider.

- Fund Switching Charges: The policy allows 4 free fund switches in each policy year. Any additional switch beyond this limit is charged at ₹100 per switch.

- Partial Withdrawal Charges: May apply as per the policy terms.

- Applicable Taxes: Levied on relevant charges as per the prevailing tax laws.

For LIC's official sample illustration, a 30-year-old investing ₹1,25,000 for 20 years under Option 1 has a projected maturity value of ₹4,65,044 at the 8% illustration rate. However, the corresponding net yield after charges is 6.79%, highlighting the impact these charges can have on your overall returns.

Sample Returns at 4% and 8%

This sample illustration is for a 30-year-old standard life, offline purchase, ₹1,25,000 single premium, 20-year policy term, and no accidental death benefit rider.

Is LIC Nivesh Plus Worth Buying?

You may consider LIC Nivesh Plus if you:

- Prefer a single-premium ULIP over regular premium payments.

- Want market-linked investment exposure with life insurance.

- Value guaranteed additions credited to the unit fund at specified policy durations.

- Are comfortable with the mandatory five-year lock-in period.

- Want the flexibility to switch between the available funds during the policy term.

Before investing, keep the following in mind:

- Life Cover May Be Limited: Under Option 1, the basic sum assured is only 1.25 times the single premium. Option 2 provides 10 times the single premium as life cover but is available only to applicants up to 35 years of age and attracts higher mortality charges. So, LIC Nivesh Plus should not be treated as a substitute for a standalone term insurance plan if your goal is meaningful life coverage.

- Policy Charges Reduce Investment Returns: Premium allocation charges, Fund Management Charges (FMC), mortality charges, rider charges (if opted), and applicable taxes can lower the effective return. In LIC's official illustration, an 8% assumed gross return translates to a net yield of 6.79% after charges.

- Compare Alternatives. If your primary objective is long-term wealth creation, compare LIC Nivesh Plus with investing in low-cost mutual funds alongside a separate term insurance plan. Separating insurance and investment may offer greater flexibility and lower overall costs for many investors.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 24,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat with us on WhatsApp!

Conclusion

The LIC Nivesh Plus Returns Calculator estimates your policy's potential maturity value, but it does not predict your actual returns. Since the plan is market-linked, your maturity value depends on fund performance, market conditions, and the charges deducted during the policy term.

Look beyond the 4% and 8% benefit illustrations. Consider the impact of policy costs, compare the two sum assured options, and assess whether a ULIP suits your financial goals.

If you want a single-premium plan that combines life insurance with market-linked investments, LIC Nivesh Plus may be an option. If your priority is long-term wealth creation, compare it with low-cost mutual funds and a standalone term insurance plan before investing. If you are looking for reliable long-term coverage, explore our guide on the best term insurance plans in India.

Frequently Asked Questions

Last updated on: