The LIC Claim Settlement Ratio (CSR) for FY 2024 to 25 stands at 98.15%. Life Insurance Corporation of India has maintained this strong performance consistently, with a 3-year average of 98.35% from FY 2022 to 25, which is well above the industry benchmark. This indicates that LIC settles a large share of claims, reinforcing its position as one of the most reliable life insurers in India.

This guide helps you break down what these numbers actually mean, analyse LIC’s performance over time, and evaluate whether it aligns with your specific term or life insurance needs.

Life Insurance Corporation of India (LIC), established in 1956, is India’s largest life insurer by total first-year premium income. As of March 31, 2025, LIC managed total assets worth approximately ₹56.23 lakh crore, held a 57.05% market share in total first-year premium income, had 2,048 branch offices, and worked with more than 14.86 lakh agents.

When buying a life insurance policy, one question matters above everything else: will LIC actually pay my family’s claim? That is exactly what the CSR helps you understand.

Confused about whether LIC is the right insurer for your term plan? Book a call or chat on WhatsApp, and our expert advisors will guide you.

What is a Claim Settlement Ratio?

A Claim Settlement Ratio (CSR) represents the percentage of death claims an insurer successfully settles out of the total claims it was required to process in a given financial year. It is the single most cited metric for judging how reliably an insurer pays up.

For instance, if LIC receives 10,000 death claims and settles 9,815 of them, its CSR for that year is 98.15%. The higher the ratio, the more dependable the insurer is generally considered to be.

How To Interpret CSR:

97% and Above: Indicates a strong, efficient, and highly reliable insurer with a high claim settlement track record.

90%–97%: Most claims are settled, but you should review other metrics before deciding.

Below 90%: May signal higher chances of delays, rejections, or an inconsistent claims experience.

Note: LIC's CSR for FY 2024–25 sits in the 'strong' range. While a handful of private insurers now cross 99%, LIC's performance across over 8 lakh claims per year makes its ratio especially meaningful.

Want to go beyond the interpretation? Ditto Data Lab features detailed term insurance data from insurers and IRDAI, collected from official sources and curated by our team.

How to Calculate the LIC Claim Settlement Ratio?

Here's how the LIC claim settlement ratio is calculated:

This gives LIC a claim settlement ratio of 98.15% for FY 2024-25.

At Ditto, we recommend evaluating CSR alongside other key metrics such as the Amount Settlement Ratio (ASR), complaint volume per 10,000 claims, Gross Written Premium (GWP), and solvency ratio. This is because CSR only tracks the number of claims settled, not the value. An insurer could settle a high volume of smaller claims while disputing larger ones, resulting in a high CSR but a low ASR. Looking at multiple metrics together gives a more accurate picture of an insurer’s true claims reliability.

CTA

Where Can I Find the Claim Settlement Ratio for LIC?

You can check the LIC claim settlement ratio from the following verified sources:

CSR: Despite handling the highest individual death claim volume in India, LIC maintains a CSR consistently above 97%, a stronger reliability indicator than the marginally higher CSR achieved by insurers operating on a much smaller scale.

ASR: LIC's amount settlement ratio is higher than the industry average, indicating that not only are claims being settled, but a larger proportion of the claim value is being paid out.

Complaints: LIC records significantly lower complaint volumes per 10,000 claims compared to the industry median, suggesting a relatively smoother claims experience and fewer disputes during settlement.

GWP: LIC collects the highest gross written premium among all life insurers in India, reflecting both its scale and the sustained trust of its policyholder base.

Solvency ratio: LIC maintains a solvency ratio of 2.0x, broadly in line with the regulatory requirement. This indicates that the insurer holds adequate capital buffers to meet future claim obligations comfortably.

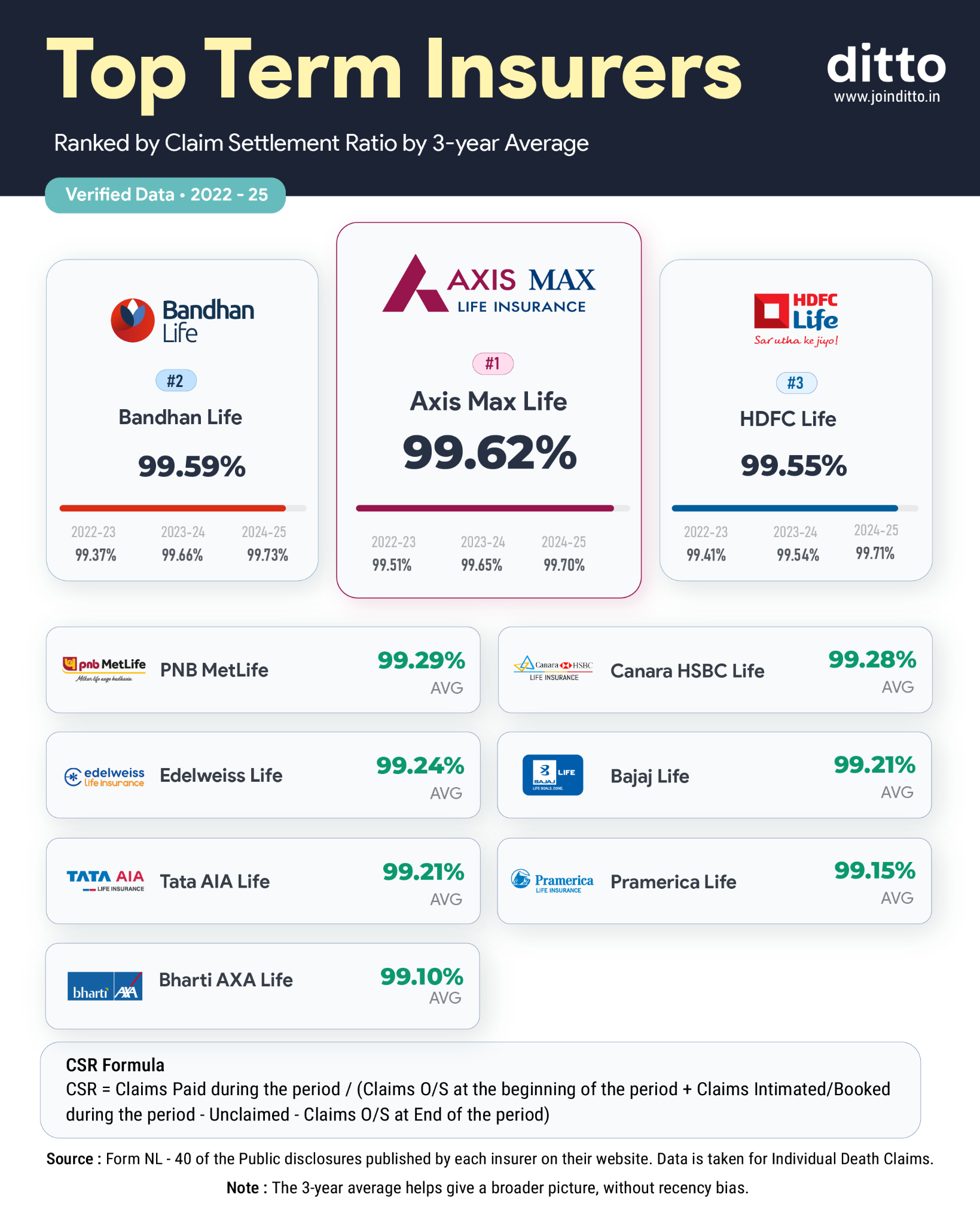

Top 10 Term Insurance Providers by Claim Settlement Ratio

Key Insight: Even with a 3-year average CSR of 98.35%, Life Insurance Corporation of India narrowly misses the top 10 list, primarily because private insurers now consistently exceed 99%. However, LIC's performance at its massive claim volumes remains genuinely impressive and should not be discounted when evaluating its term insurance claim settlement reliability.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

LIC is one of the largest and most trusted life insurers in India. Its consistent claim settlement ratio, low complaint volume, and government backing make it a dependable choice for those who prioritize reliability above all else. On the downside, premiums tend to run higher and product flexibility is limited compared to leading private insurers, which is worth factoring in before you decide.

Overall, LIC is a solid, time-tested insurer with a claims track record that holds up well given the sheer scale at which it operates.

If you'd like to see how the insurer compares with other leading insurers, check out our detailed guide on the best term insurance plans in India.

Frequently Asked Questions

What is the LIC claim settlement ratio for 2024–25?

Life Insurance Corporation of India reported a claim settlement ratio of 98.15% for FY 2024 to 25, based on data from the Insurance Regulatory and Development Authority of India. The LIC claim settlement ratio 2025 reflects this figure, along with a strong 3-year average of 98.35% from FY 2022 to 2025. LIC also settled 97.08% of claims within 30 days in FY25, processing over 8 lakh claims efficiently. These numbers indicate robust operational capability and reliability at scale, and can be verified through IRDAI reports, LIC disclosures, or trusted advisory platforms.

Has the LIC claim settlement ratio improved or declined over the years?

LIC’s claim settlement ratio has seen a slight decline over recent years, moving from 98.66% in FY 2022-23 to 98.24% in FY 2023-24 and 98.15% in FY 2024-25. While this may appear concerning at first glance, the change is marginal. LIC continues to process the highest number of death claims in India, exceeding 8 lakh annually. Its 3-year average CSR of 98.35% at this scale remains a strong indicator of reliability. When compared fairly, smaller insurers with higher CSRs often operate at significantly lower claim volumes.

What does the amount settlement ratio (ASR) mean for LIC, and why does it matter?

The Amount Settlement Ratio measures the percentage of total claim value paid by an insurer, rather than just the number of claims settled. LIC’s 3-year average ASR of 95.48% is slightly above the industry average of 94.83%. This indicates that a high proportion of claim amounts are paid out, reducing the likelihood of partial settlements. Since CSR counts both full and partial settlements equally, ASR becomes an important complementary metric. Evaluating both CSR and ASR together provides a more accurate understanding of an insurer’s claim settlement quality.

Where can I find the official LIC claim settlement data?

LIC’s claim settlement data can be accessed through multiple reliable sources. These include the IRDAI Annual Report and Handbook on Indian Insurance Statistics, LIC’s public disclosures under Form L 40, and platforms like Ditto Insurance that compile verified insurer data. IRDAI usually publishes its annual report around December for the previous financial year. Referring to these sources ensures accuracy and helps you make informed decisions when comparing insurers.

Does a high CSR guarantee my LIC claim will be approved?

No, a high CSR does not guarantee that every individual claim will be approved. LIC’s CSR reflects aggregate performance across all claims. Individual claims may still be rejected due to non-disclosure of medical history, policy exclusions, lapsed premiums, or fraud. To improve the likelihood of claim approval, it is essential to provide accurate and complete information at the time of purchase. Keeping the policy active by paying premiums on time and understanding policy terms also plays a critical role in ensuring successful claim settlement.

How does LIC settle term insurance death claims, and what is the process?

After the policyholder’s death, the nominee must inform Life Insurance Corporation of India through a branch office or its online portal. The required documents typically include the death certificate, original policy bond, claimant statement, identity proof, and bank details. LIC reviews the submitted documents and processes the claim. Straightforward cases are usually settled within 30 days, while claims made within the first three years of policy issuance may undergo additional verification. In FY 2024 to 25, LIC settled 97.08% of claims within 30 days, indicating efficient turnaround times and strong operational capability.

How does Ditto evaluate LIC as an insurer?

At Ditto Insurance, we evaluate insurers using a 3-year average claim settlement ratio instead of relying on a single year’s data, as it provides a more reliable view of long-term performance. We also assess additional metrics such as the Amount Settlement Ratio, complaint volume per 10,000 claims, Gross Written Premium, and solvency ratio. Across these parameters, Life Insurance Corporation of India performs strongly and consistently. LIC is not a Ditto partner insurer, and our evaluation is completely independent, based only on publicly available Insurance Regulatory and Development Authority of India data.

What is LIC’s solvency ratio, and what does it indicate?

Life Insurance Corporation of India maintains a solvency ratio of 2.0x, which is broadly in line with the industry median of 2.04x and comfortably above the minimum requirement set by Insurance Regulatory and Development Authority of India at 1.5x. The solvency ratio measures an insurer’s ability to meet long-term financial obligations, including future claim payouts. A ratio of 2.0x means LIC holds twice the capital required by regulation, indicating strong financial stability. For term policyholders with coverage spanning 20 to 40 years, this is an important signal of long-term reliability.

How is LIC’s CSR calculated, and is the formula standardized?

Life Insurance Corporation of India calculates its claim settlement ratio by dividing total claims settled by total claims eligible for settlement, multiplied by 100. Total eligible claims include those carried forward from the previous year, plus new claims reported, minus claims rejected or still pending at the end of the year. Importantly, the Insurance Regulatory and Development Authority of India does not mandate a standardized formula. As a result, CSR figures may vary slightly across platforms and insurers depending on the methodology used, which is important to consider when comparing data.

Does LIC’s CSR include maturity and survival benefit claims or only death claims?

Life Insurance Corporation of India publishes its claim settlement ratio based only on individual death claims, not maturity claims or survival benefit payouts. Maturity claims, where the policyholder outlives the term and receives the sum assured, are processed separately and are rarely disputed. The CSR reported in Insurance Regulatory and Development Authority of India (IRDAI) data reflects how reliably LIC pays claims when a policyholder dies during the policy term. This distinction is important because including maturity claims would inflate the ratio and reduce its usefulness as a true indicator of claim settlement reliability.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.