Quick Overview

ICICI Prudential Life Insurance is a leading private insurer known for its strong claims record and digital-first approach. Its ULIPs combine market-linked investing with life cover, offering multiple fund options and flexibility.

This guide breaks down how ICICI Prudential ULIP plans work, their key features, associated costs, and how they stack up against simpler alternatives like term insurance and mutual funds.

ICICI Prudential Life Insurance Performance Metrics

Insights:

- CSR is slightly below the industry mean but remains consistently strong, indicating that the vast majority of genuine claims are settled without issue.

- ASR is above the industry average, suggesting ICICI Prudential typically pays out claims in full, even for larger claim amounts.

- Complaint volumes are well below the industry median, pointing to a smoother, less dispute-prone claims experience for policyholders.

- Annual business volumes are significantly higher than the median, reflecting ICICI Prudential's position as one of the largest private insurers in India.

- Solvency ratio is in line with the industry median and comfortably above the IRDAI regulatory minimum of 1.5x, indicating a financially stable insurer.

ULIP Plans Offered by ICICI Prudential

Note: This is not an exhaustive list. For the full list of all ICICI Prudential’s plans, refer to this ICICI list of plans page.

Premiums for ICICI ULIP Plans

Note: Returns are not guaranteed because they are market-linked. The death benefit includes a lump sum (higher of sum assured or minimum death benefit) along with a “Smart Benefit,” where future premiums are waived, and the insurer continues investing on the policyholder’s behalf.

Additionally, the nominee receives a fixed annual income (₹1 lakh in this case) until the end of the policy term. The figures are taken from the ICICI Pru SIP+ brochure, which provides more information on the ICICI Prudential ULIP plan returns.

Numerical Illustration Based on ICICI ULIP Plans

1) Life Cover

- ICICI iProtect Smart Plus ₹50 lakh cover for around ₹6,350/year

- ICICI Prudential SIP+ ULIP Life cover = 10x annual premium ₹1,00,000/year - cover of ₹10 lakh

A term plan provides significantly higher coverage at a much lower cost for a 30-year-old, non-smoking man for a policy term of 25 years.

2) Returns

ICICI’s 25-year illustration for SIP+ shows:

- 8% gross return - → Under 7% net yield

This drop is due to:

- Fund management charges

- Policy admin costs

- Mortality charges

While ULIPs participate in the market, actual returns are lower after costs. Term insurance delivers high, cost-effective protection. That’s why term plans are typically the cleaner choice for protection, while ULIPs should be evaluated separately as investment products.

Drawbacks of Buying an ICICI Prudential ULIP Plan

Multiple Charges Reduce Effective Returns

ICICI ULIP plans come with several charges, including premium allocation, fund management, mortality, and policy administration fees. While the fund may show decent gross returns, these layered costs can significantly eat into your actual long-term returns.

Returns Are Market-Linked and Not Guaranteed

Unlike traditional savings plans, ICICI ULIPs depend entirely on market performance. As seen in the SIP+ illustration, returns at 4% and 8% are only assumed scenarios, not guaranteed outcomes. This makes returns unpredictable, especially for conservative investors.

Life Cover is Relatively Low

Most ICICI ULIPs offer life cover in the range of 7–10× the annual premium. While this may seem adequate, it usually falls short of the ideal coverage recommended for proper financial protection, especially when compared to term insurance.

Five-Year Lock-In Restricts Liquidity

Like all ULIPs, ICICI ULIP plans come with a mandatory 5-year lock-in period. During this time, you cannot fully withdraw your funds, which makes these plans unsuitable if you need flexibility or access to your money in the short term.

Complex Structure Makes It Hard to Evaluate

With features such as Smart Benefit, fund switching, top-ups, and multiple variants (SIP+, Signature Assure, Pru1 Wealth), ICICI ULIPs can be complex to understand and compare. This makes it harder to evaluate returns, costs, and benefits clearly.

Combines Insurance and Investment Inefficiently

ICICI ULIPs bundle insurance and investment into one product. This often leads to compromises, lower life cover, and reduced investment efficiency due to charges.

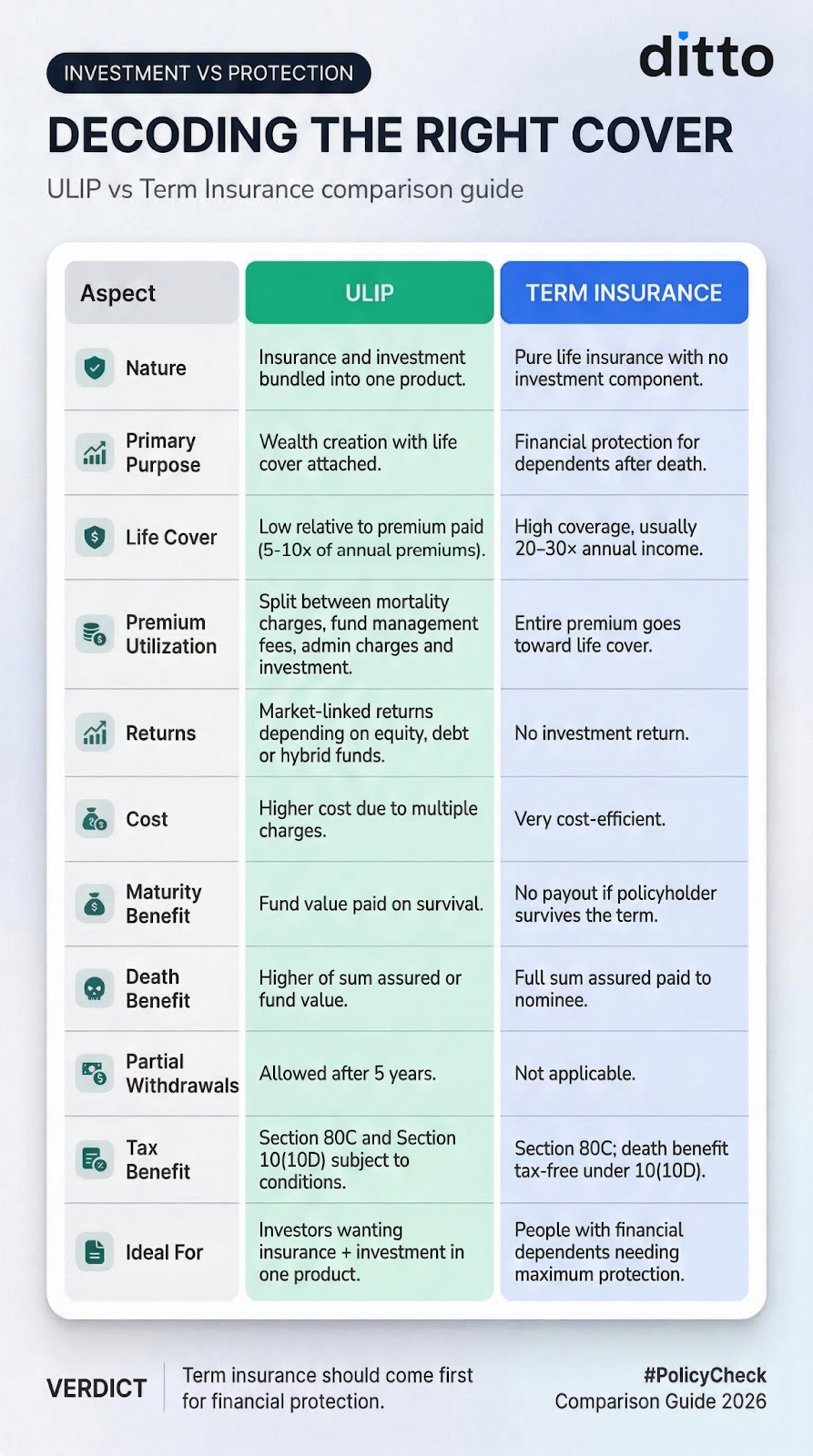

ULIP vs Term Insurance: Which Is Better?

If you’re comparing ULIPs and term insurance, the key is understanding how they differ in purpose, cost, and outcomes. At a high level, it’s a choice between a bundled product that combines insurance and investment, and a simpler approach where you keep both separate to optimise protection and returns. We’ve broken this down in detail in the infographic. For a deeper dive, check out our full guide on ULIPs vs term insurance.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat over WhatsApp with our advisors.

Conclusion

ICICI Prudential ULIPs combine insurance and investment in one plan, but this often leads to trade-offs. The life cover is relatively low, and returns can be impacted by charges over time.

At Ditto, we generally prefer keeping the two separate. A term plan gives you higher coverage at a lower cost, while investing in mutual funds, PPF, or NPS offers better flexibility and potential returns.

If you prefer ICICI Prudential as an insurer, you may be better off opting for their flagship term plan, ICICI Prudential iProtect Smart Plus, which offers significantly higher coverage at a lower cost. This plan is also among our top recommendations for the best term insurance plans in India in 2026.

Frequently Asked Questions

ICICI Prudential Customer Reviews

Last updated on: