Quick Overview

HDFC Life Insurance Company was established in 2000 as a joint venture between Housing Development Finance Corporation and Standard Life. Headquartered in Mumbai, it offers term insurance, ULIPs, savings, retirement, health, and child plans. After the 2023 merger of HDFC Ltd. with HDFC Bank, HDFC Life became an associate company of the bank.

HDFC Life Insurance: Performance Metrics

Key Insights:

- The insurer has a strong 3-year average CSR of 99.55%, higher than the industry average of 98.66%. This means fewer than 1 in 100 claims are rejected, placing it among the most reliable life insurers in India.

- Its 3-year average ASR stands at 96.72%, well above the industry average of 94.83%.

- The insurer’s average business volume of ₹30,560 cr is significantly higher than the industry median of ₹3,411.73 cr, reflecting its large-scale operations, strong distribution network, and established brand presence.

- Average death claim payouts stand at ₹1,678 cr, compared to an industry median of ₹195.05 cr. This difference largely reflects variations in portfolio composition. Importantly, death claim payouts rose over the period, while CSR also improved, indicating consistent claim servicing.

- Customer complaints averaged 1.33 per 10,000 claims, which is relatively low. Complaints dropped from 2.0 to 1.0, showing improvement in grievance handling and customer experience.

- The 3-year average solvency ratio is 1.94x, which is above the 1.5x regulatory requirement set by the IRDAI, but slightly below the industry median of 2.04x. The gradual decline may be worth monitoring as claim payouts increase.

ULIP Plans Offered by HDFC Life Insurance

ULIP Premiums Across HDFC Life Plans

Note: Projected values are illustrative for a 25-year-old. Actual returns are not guaranteed and will depend on market performance. Differences in projected values reflect differences in product structure, charges, and benefit design.

Drawbacks of Buying an HDFC ULIP Plan

- Multiple Charges Reduce Effective Returns: ULIPs include several charges, such as premium allocation, policy administration, mortality, and fund management charges. These are deducted from your premium or fund value, which means a portion of your money does not get invested and compounded from the start.

- Life Cover is Often Insufficient: Most ULIPs offer life cover of about 10 times the annual premium. For individuals with financial dependents, this is usually not enough to replace lost income. A separate term insurance plan typically offers much higher coverage at a lower cost.

- Five-Year Lock-in Limits Liquidity: All ULIPs have a mandatory five-year lock-in as per IRDAI rules. If the policy is surrendered before this period, the fund value moves to a discontinued policy fund that earns 4% annually after charges. Access to funds is therefore restricted in the early years.

- Market Risk with Limited Investment Flexibility: ULIP returns depend on market performance and are not guaranteed. While fund switching is allowed, the options are limited to funds offered by the insurer, and the number of switches allowed each year may be capped.

- Product Complexity makes Comparison Difficult: ULIPs combine insurance and investment in one product. Because charges are embedded and returns are shown after deductions, it becomes difficult for buyers to clearly compare them with simpler alternatives like term insurance and mutual funds.

- Tax Benefits have Conditions: Maturity proceeds are tax-free only if the annual premium stays within 10% of the sum assured. For policies issued after February 2021 with aggregate premiums across all ULIPs above ₹2.5 lakh annually, the maturity proceeds are taxable.

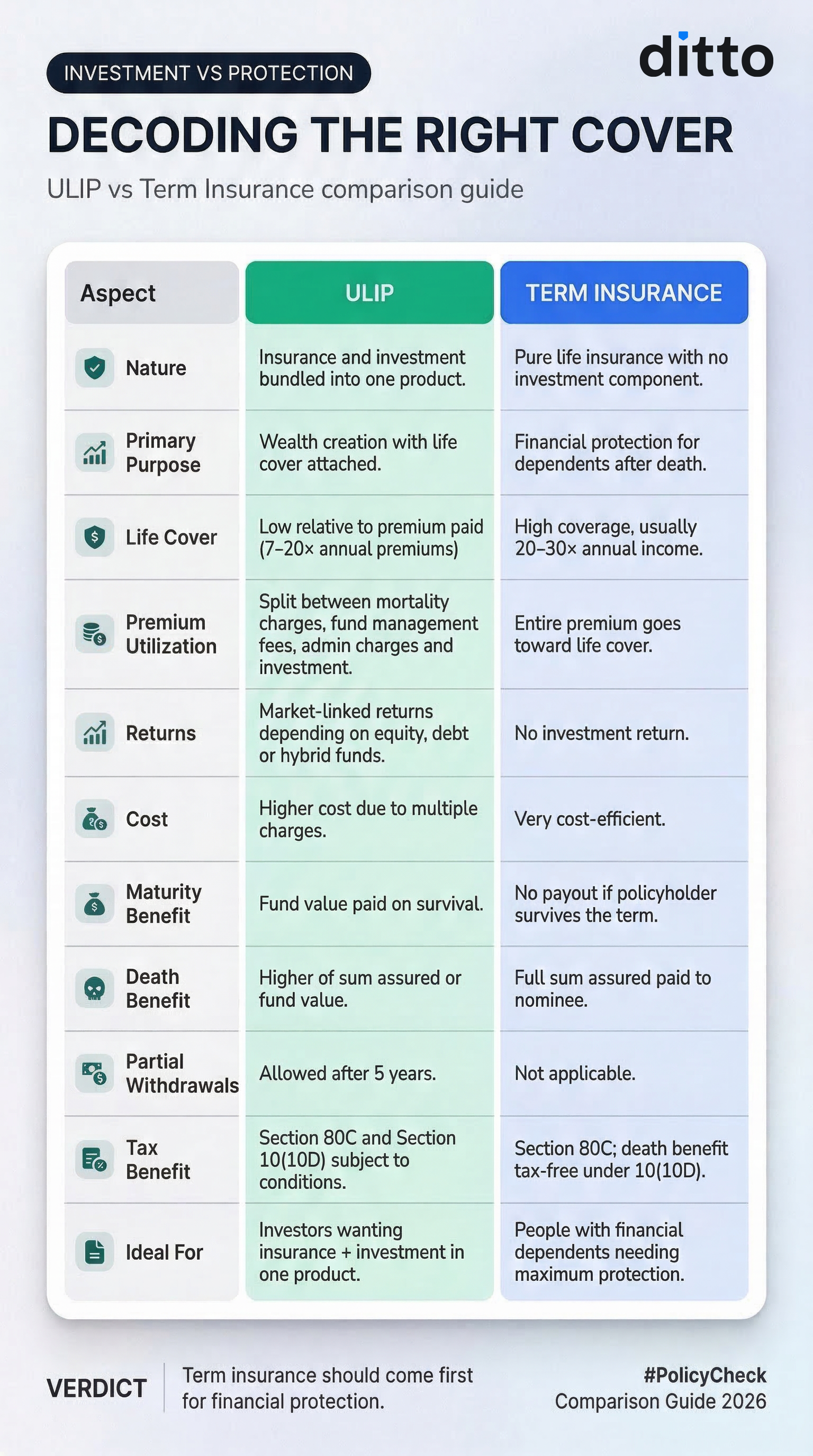

ULIP vs Term Insurance: Which is Better?

Term insurance offers maximum life cover (20-30x annual income) at minimum cost, making it the stronger choice from a pure protection standpoint. For wealth creation, low-cost options such as mutual funds, National Pension System (NPS), Public Provident Fund (PPF), and fixed deposits typically deliver better post-charge returns over long horizons.

ULIPs serve a purpose for those who prefer a structured, bundled approach to insurance and investment under a single product. However, keeping the two separate generally gives you more flexibility, transparency, and value for money.

Here’s a numerical illustration of investments in the two products:

Let’s take an example. Consider a 30-year-old non-smoker who invests ₹10,000 per month (₹1,20,000 annually) for 20 years to build a retirement corpus while also ensuring financial protection for the family.

Option A: ULIP Child / Wealth Plan

Option B: Term Insurance + Direct Mutual Fund SIP

The Difference

At a 2% net return, the ULIP corpus after 20 years becomes about ₹35.5 lakh, even though the total premium paid is ₹24 lakh. This means the growth is very limited, as a large part of the compounding is reduced by various policy charges.

In comparison, a Term Insurance + SIP strategy can build a corpus of about ₹83.26 lakh with the same total outflow, while also providing ₹1 cr of life cover throughout the period. If the policyholder dies in year 10, the ULIP may pay around ₹12 lakh, whereas the term plan would pay ₹1 cr.

The key insight is that ULIPs bundle insurance and investment inefficiently. You get lower cover and reduced investment returns due to charges. Buying term insurance and investing separately through SIPs often works better.

Note: Corpus figures are illustrative and based on standard compounding calculations. Mutual fund returns are market-linked and not guaranteed, and past performance does not indicate future results. Term insurance premiums are indicative and may vary based on the insurer and underwriting assessment.

Check out the infographic to understand the differences between a term plan and an ULIP:

Note: If you opt for a Return of Premium Term Insurance (TROP) and survive the policy term, your base premiums are refunded. This suits low-risk buyers who want guaranteed returns. However, premiums are much higher (50-100%) than regular term plans, returns don’t grow, and rider premiums aren’t refunded, causing overall value loss over time.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right term insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or WhatsApp us now, slots fill up fast!

Conclusion

HDFC Life ULIPs may suit individuals who are not eligible for a term plan due to medical underwriting or occupational risks. They can also work for people who already have adequate term insurance but want a combined investment-plus-insurance product. ULIPs may appeal to investors who prefer structured, long-term investing with a mandatory lock-in, which can help maintain financial discipline.

Ditto does not recommend ULIPs because they tend to be less efficient than buying a term plan and investing separately. While HDFC Life Insurance Company is a Ditto partner insurer, our recommendation leans toward pure protection products such as the HDFC Life Click 2 Protect Supreme Plus term plan, which offers straightforward life cover without mixing insurance and investment.

If you are looking for a term plan from insurers with established track records and affordable riders, we recommend the best term insurance plans, which align with your future goals and family needs.

When you choose a term insurance plan with the right coverage amount, policy duration, and riders, it fulfills your financial responsibilities. The cover should be sufficient to replace your income and support goals such as children’s education, home loans, or household expenses.

Disclaimer: The information in this guide is based on publicly available sources and insurer disclosures and is shared for educational purposes only. Always verify policy details with the insurer and consult a licensed advisor before making financial decisions.

Frequently Asked Questions

Last updated on: