![Generali Central Life Insurance: Plans, Review & CSR [2026]](https://stat.joinditto.in/images/2026/05/Generali-Central-Life-Insurance-@2x.webp)

Overview

What happens when a global insurance major teams up with a trusted public sector bank? You get Generali Central Life Insurance, a rebranded player aiming to combine global expertise with local reach. It is still evolving, but it is quickly becoming a name worth watching in India’s term insurance space.

In the next few minutes, we will walk you through Generali Central Life Insurance plans and whether it fits your needs, so you can make a clear and confident decision.

Did You Know?

Generali Central Life Insurance Plans

1. Generali Central Care Plus Plan

Care Plus is a pure term plan that provides life cover with an optional accidental death benefit. It focuses on protection, with flexible payout options and no savings component.

Eligibility Conditions:

- Entry Age: 18 to 65 years

- Maturity Age: 23 years to 85 years

- Premium Payment Type: Regular pay and limited pay

- Sum Assured: ₹25 lakh with no upper limit

- Policy Term: 5 years to 67 years

- Premium Mode: Yearly, half-yearly, quarterly, and monthly

Key Features:

- Offers two options, which include Life Cover and Extra Life Cover (Life Cover with Accidental Death Benefit)

- Optional accidental death cover with extra payout

- Lump sum, fixed, or mixed death benefit payout options

- No maturity benefit or investment component

However, the policy lacks modern features such as premium break options and terminal illness cover, which would add value. Additionally, riders such as waiver of premium and accidental total permanent disability are missing.

2. Generali Central Saral Jeevan Bima

Saral Jeevan Bima is a simple, standardized term plan designed for basic life protection with easy terms and a uniform structure. Such plans are mandated by IRDAI for insurers to offer. Saral Jeevan Bima is designed to make life insurance simple, affordable, and accessible for everyone.

Eligibility Conditions:

- Entry Age: 18 to 65 years

- Maturity Age: 23 to 70 years

- Sum Assured: ₹5 lakh to ₹25 lakh

- Policy Term: 5 to 40 years

- Premium Options: Single, limited, or regular pay

- Premium Payment Frequency: Yearly, half-yearly, and monthly

Key Features:

- Pays the sum assured on death during the policy term

- 45-day waiting period for non-accidental deaths

- No maturity or survival benefit

- Simple and standardized design, with no riders offered

3. Generali Central Saral Ashray Yojana

Saral Ashray Yojana is a term plan with life cover plus accelerated benefits for critical illness and accidental disability.

Eligibility Conditions:

- Entry Age: 18 to 60 years

- Maturity Age: 23 to 65 years

- Sum Assured: ₹3 lakh to ₹25 lakh

- Policy Term: 5 and 10 years

- Premium Options: Single or regular pay

- Premium Payment Frequency: Yearly and single

Key Features:

- Life cover with a death benefit payout

- Covers 20 critical illnesses (CI) with accelerated payout

- Accelerated Accidental Total and Permanent Disability Benefit (ATPD) included

- Waiver of premium after the first valid claim on diagnosis of a covered CI or ATPD

- No maturity, surrender, or loan benefit

While the plan offers useful features, the maximum policy term is limited to 10 years, and the sum assured options are restricted. This makes it inadequate for long-term protection needs. It also lacks key built-in features, such as life stage benefit.

Other Plans Offered:

Apart from the above term plans by Generali Central Life Insurance, the insurer also offers:

- Unit Linked Insurance Plans (ULIPs) like Generali Central Dhan Vridhi

- Savings Plans like Generali Central New Assure Plus Plan

- Child Plans like Generali Central Assured Education Plan

- Retirement Plans like Generali Central Saral Pension

However, at Ditto, we do not recommend plans that combine insurance and investment. They usually offer lower life cover and are less efficient than buying a pure term plan and investing separately.

Sample Premiums

Let’s take the Care Plus Plan as an example to understand how premiums work. Assume you choose a ₹1 crore life cover, a policy term up to age 65, and a 10-year premium payment term. You pay premiums annually, fall under the general category, and opt for a lump sum payout.

Note: The figures are illustrative, and actual premiums depend on your age, gender, sum assured, and the insurer's underwriting criteria. These are first-year premiums. Use the Care Plus Plan calculator to get an estimate of your premiums.

Generali Central Life Insurance: Performance Metrics

Note: These metrics are based on IRDAI annual reports and Generali Central public disclosures for the overall insurer. Solvency ratio for the year FY2022-23 is not available at the moment.

Key Insights:

- Below-Average Claim Settlement Performance: Both CSR and ASR are lower than industry benchmarks. This means the insurer settles fewer claims and may pay a lower share of claim amounts than peers, which can affect overall trust.

- Smaller Business Scale: The annual business volume (around one-fourth of the industry average) and claim payout figures are much lower than industry medians. This reflects a smaller presence, which can affect reach, pricing efficiency, and brand strength.

- High Complaint Levels: The complaint ratio is around nine times the industry median. This points to possible gaps in customer service, claims experience, or communication quality.

- Moderate Financial Strength: The solvency ratio is above the regulatory minimum but below the industry median. The insurer is stable, but it does not offer the same level of financial comfort as its stronger peers.

For a closer look at these insurer metrics, explore Ditto Data Lab. It includes term insurance data from public disclosures that have been carefully curated by our team over the years.

Pros & Cons of Generali Central Life Insurance

Pros of Generali Central Life Insurance

Stronger Strategic Backing

The tie-up with the Central Bank of India gives the insurer access to a large branch network and a trusted public-sector brand. This can improve reach, especially in smaller cities and bank-led sales channels.

Improving Claims Experience

Claim settlement performance has improved in recent years. The CSR improved steadily from 95.05% in 2022 to 98.08% in 2025, reflecting better claims performance over time.

Adequate Financial Stability

The insurer meets regulatory solvency requirements of 1.5x, which shows basic financial strength. It is stable, but not among the strongest in the market.

Cons of Generali Central Life Insurance

- Not a Top-Tier Term Brand Yet: The insurer is improving, but it does not yet match the scale, track record, or market confidence of leading term insurance providers.

- Lower Cover in Basic Plans: Standard plans, such as Saral Ashray, offer limited coverage. This may not be enough for people with dependents, loans, or long-term financial goals.

- Profitability Still Developing: The company is still building its business and has not yet reached strong profitability, according to the insurer’s 2024-25 annual report. This shows it is in a growth phase rather than a mature stage.

- No Rider Option: Plans like Care Plus do not include additional riders such as critical illness cover or waiver of premium. This keeps the plan simple and focused only on life protection, but it also limits the scope of financial support during health-related or disability-related situations.

Which Type of Life Insurance Should You First Buy from Generali Central Life Insurance?

Start with a pure term plan like the Care Plus Plan. Once this core protection is in place, you can explore savings or retirement plans. Always secure risk first before looking at returns or wealth creation. Here’s why you should get a term insurance first:

- Protects the Most Important Risk First: The first purpose of life insurance is simple. It should protect the family if the earning member is no longer around. A term plan directly addresses this need by replacing income and helping the family manage everything without financial distress.

- Keeps Insurance Simple and Focused: A term plan does one job well. It provides life cover. It does not mix savings, investment, or maturity benefits. This clarity makes it easier to understand and ensures that the full focus remains on protection.

- Helps Avoid Inadequate Cover: Many people end up with small insurance amounts through savings-linked policies. These may feel safe, but they often fall short during real financial emergencies. A term plan ensures that protection matches the actual responsibility a family carries.

- Provides Clear Financial Support to the Family: In a claim situation, a term plan offers a straightforward payout. It supports essential needs such as living expenses, loan repayment, education, and long-term stability without hassle.

- Prevents Wrong Financial Priorities: When insurance is bundled with investment, the focus often shifts away from protection. People may feel covered, but the actual insurance value may be low. A term plan ensures protection remains the first priority, not an afterthought.

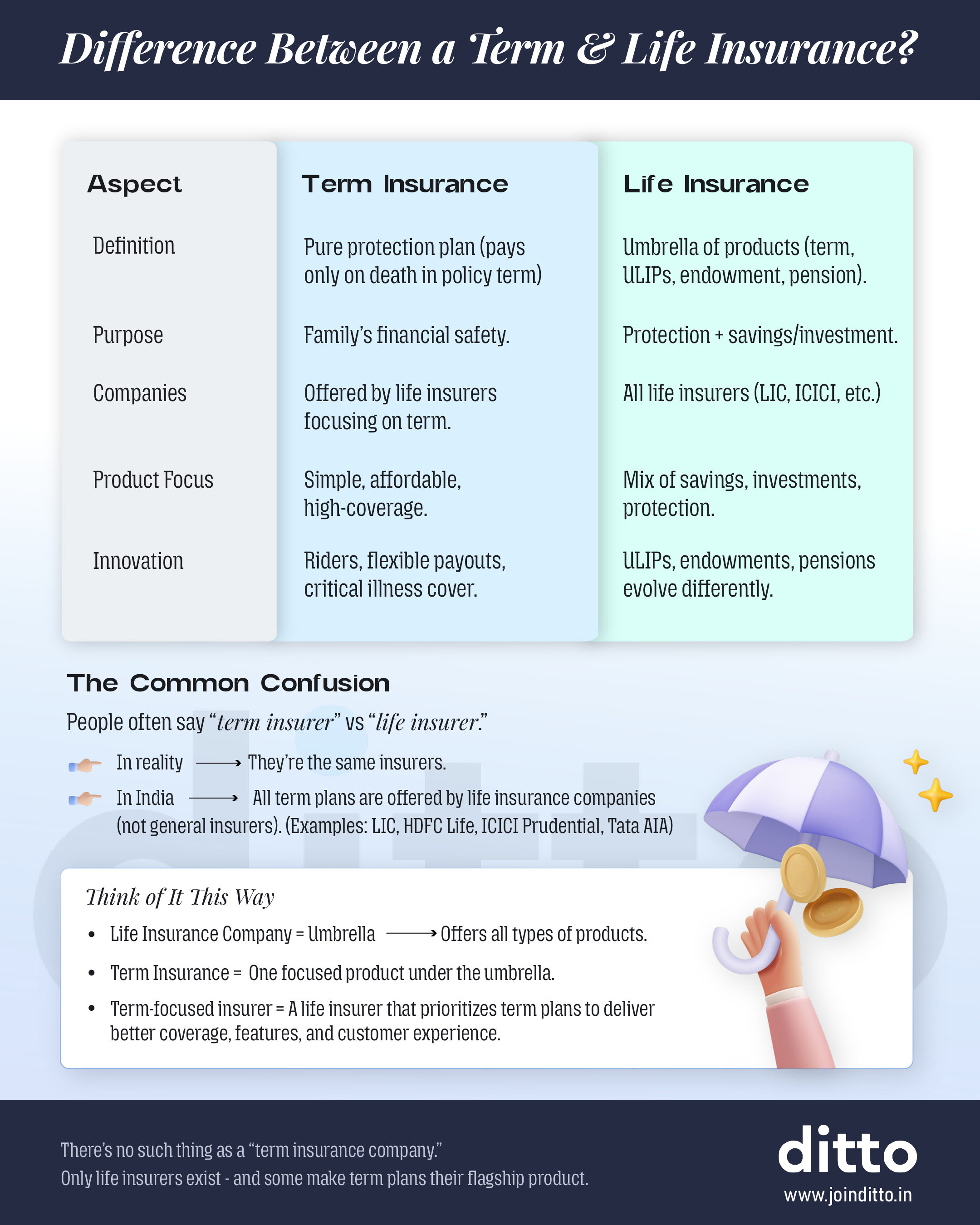

Take Note: People often confuse life insurance with term insurance. Life insurance is the broader category, while term insurance is the pure protection tool. Most other life insurance products mix protection with savings, which reduces the actual cover for the same premium. The core purpose of life insurance is not to return money but to replace income if something happens to the earning member. Refer to the infographic for clarity.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

Generali Central Life Insurance has been improving its performance over the years. Its product range is clear and protection-focused. However, it still remains a cautious shortlist choice rather than a default recommendation and may not be ideal for everyone.

Generali Central is going through a transition after its ownership and management change. The direction looks positive, but it is not yet a market leader. Since life insurance is a long-term commitment, it is better to track its performance over time before making a decision.

If you wish to purchase a term plan offered by established insurers, explore our guide on the best term insurance companies.

Frequently Asked Questions

Last updated on: