Quick Overview

Edelweiss Life Insurance offers several ULIPs with flexible fund options for long-term investing. Although it is newer and smaller than major insurers such as ICICI Prudential and HDFC Life, it has expanded steadily.

This guide explains how Edelweiss Life ULIP plans work, reviews key performance metrics, and compares popular plans to help you decide if a ULIP fits your financial goals.

Edelweiss Life Insurance: Performance Metrics

Take Note: The above metrics reflect the insurer's overall performance and are not limited to its ULIP portfolio.

ULIP Plans Offered by Edelweiss Life Insurance

Premiums for Edelweiss Life ULIPs

Note: Projected values are illustrative for a 35-year-old for the Wealth Rise Plus plan and for a 40-year-old for Wealth Premier. The figures listed are taken from the Wealth Rise Plus Brochure and the Wealth Premier Brochure.

Drawbacks of Buying an Edelweiss Life Insurance ULIPs

1. Multiple Charges Reduce Returns

ULIPs include several charges such as premium allocation, policy administration, mortality, and fund management fees. These charges are deducted from your premium or fund value, so not all of your money gets invested or compounded from the beginning.

2. Life Cover May Be Limited

Most ULIPs provide life cover of about 10 times the annual premium. For people with financial dependents, this may not be enough to replace lost income. A separate term insurance plan usually offers much higher coverage at a lower cost.

3. Five-Year Lock-in Restricts Liquidity

All ULIPs have a mandatory five-year lock-in period as per IRDAI regulations. If the policy is surrendered before this period, the fund value is transferred to a discontinued policy fund that earns about 4% annually after charges, limiting early access to funds.

4. Market Risk and Limited Fund Choices

ULIP returns depend on market performance and are not guaranteed. Although fund switching is allowed, investors can choose only from funds offered by the insurer, and the number of switches per year may be limited.

5. Product Complexity

ULIPs are complex products because charges like administration fees are built into the structure; it can be difficult to clearly compare them with simpler options like term insurance and mutual funds.

6. No Policy Loan Facility

ULIP plans like Wealth Premier do not offer a policy loan option, meaning policyholders cannot borrow against the policy's value during the policy term.

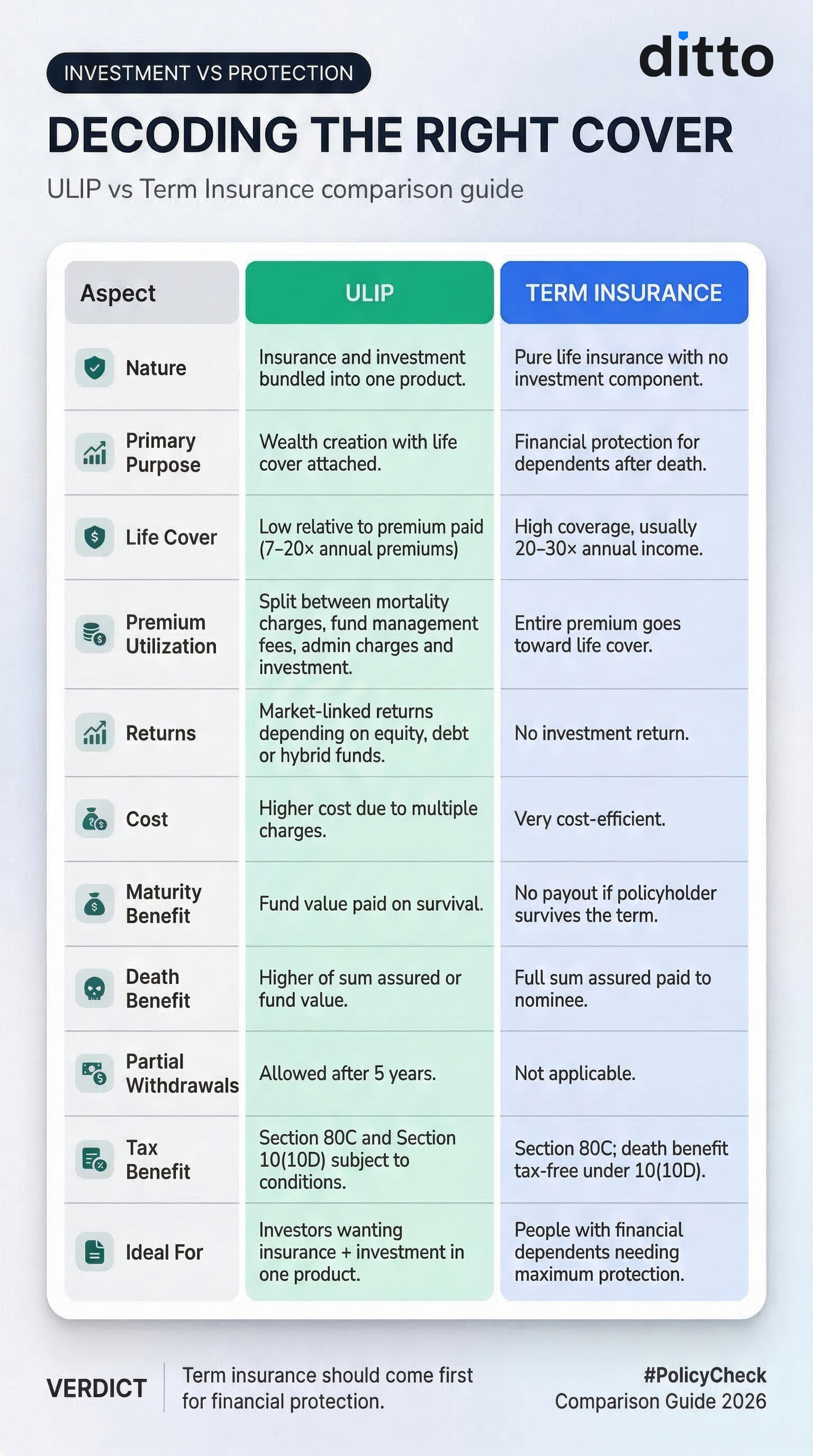

ULIPs vs Term Insurance: Which is Better?

The difference between ULIP and term insurance lies in their purpose. ULIPs combine life insurance with market-linked investments, while term insurance focuses purely on providing high life cover at a lower cost.

Check out the infographic to understand the differences between a term plan and a ULIP.

Numerical Illustration: ULIP vs Term Insurance + Mutual Fund SIP

Comparison Table

Note: The calculations are illustrative for a 30-year-old investing ₹15,000 per month for 20 years to build long-term wealth while maintaining life cover. Actual returns are based on market performance.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right term insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or WhatsApp us now, slots fill up fast!

Conclusion

Edelweiss Life Insurance Company Limited ULIPs may suit individuals who cannot easily qualify for term insurance due to medical conditions or occupational risks. They can also work for people who already have adequate term cover but want an investment-linked insurance product.

Edelweiss Life shows strong claim settlement performance and solid solvency, indicating reliability. However, its small scale and low business volumes mean limited operational experience.

If you are looking for term plans from insurers with established track records, we recommend the best term insurance companies that offer reliable protection and plans aligned with your long-term financial goals and family needs.

Disclaimer: Edelweiss Life Insurance is not one of our partner insurers. At Ditto, we do not recommend ULIPs, and the information in this guide is based on publicly available sources and the insurer’s official website. The article is shared for educational purposes only.

Frequently Asked Questions

Last updated on: