Quick Overview

ULIPs, such as those offered by Canara HSBC Life Insurance, promise long-term wealth creation along with life cover. But many buyers struggle to answer a simple question: are these plans actually worth it, or are you better off separating insurance and investment?

In this guide, we look at the Canara HSBC Life Insurance plans’ features, charges, drawbacks, and how they compare with term insurance.

ULIP Plans Offered By Canara HSBC Life Insurance

For additional plan-related details, please refer to the insurer’s official website.

Canara HSBC Life: Performance Metrics

Key Insights:

- Canara HSBC Life Insurance maintains a strong claim settlement ratio, which is higher than the industry average, indicating reliable claims experience.

- The insurer’s amount settlement ratio is also above the industry mean, suggesting fair treatment across both high-value and low-value claims.

- Its complaint volume is in line with the industry median, which indicates average service quality rather than a clear edge.

- The solvency ratio is well above the IRDAI requirement of 1.5x, reflecting strong financial stability and the ability to meet future obligations.

- However, the insurer’s business volume is slightly below the industry median, indicating a relatively smaller scale compared to some peers.

Note: Canara HSBC Life Insurance performs well across key operational metrics and appears financially stable. However, these numbers reflect the insurer’s overall performance and do not necessarily indicate that its ULIP plans are strong or suitable for every buyer.

Charges in Canara HSBC Life Insurance ULIPs

- Mortality Charges: Depends on age, sum assured, and risk profile.

- Fund Management Charge (FMC): Charged as a percentage of the fund value, typically up to 1.35 % per annum, depending on the fund chosen.

- Policy Administration Charge: Charged periodically (often monthly) and may vary based on premium and policy terms.

- Premium Allocation Charge: Applicable in the initial policy years, depending on the plan; reduces over time.

- Discontinuance Charges: Applicable if the policy is surrendered or discontinued during the lock-in period (first 5 years).

Drawbacks of Canara HSBC Life Insurance ULIPs

- Operational Complexity: With multiple fund options, plan variants, and portfolio strategies such as rebalancing and return protection, these plans may require a better understanding of how the product works and some ongoing review over time.

- Strict lock-in and Limited Liquidity: ULIPs have a mandatory 5-year lock-in period, during which withdrawals are not allowed. Even after that, partial withdrawals are subject to policy terms, so they may not offer the same liquidity as some other investment options.

- Multiple Charges can Affect Returns: Although some charges may reduce over time, these plans can include costs such as fund management charges, mortality charges, policy administration charges, and, in some variants, premium funding charges. Over the long term, these may affect overall compounding and net returns.

- Higher Minimum Premium Requirements: Some plans, such as SecureInvest and Wealth Edge, may come with higher minimum premium requirements. This may make them less suitable for those who want to begin with a smaller investment amount.

- Not Ideal for Pure Protection Needs: Since these plans combine insurance and investment, the life cover cost can be higher than a pure term plan. Also, returns are market-linked, so they may not be the right fit for those looking for simple protection or more predictable outcomes.

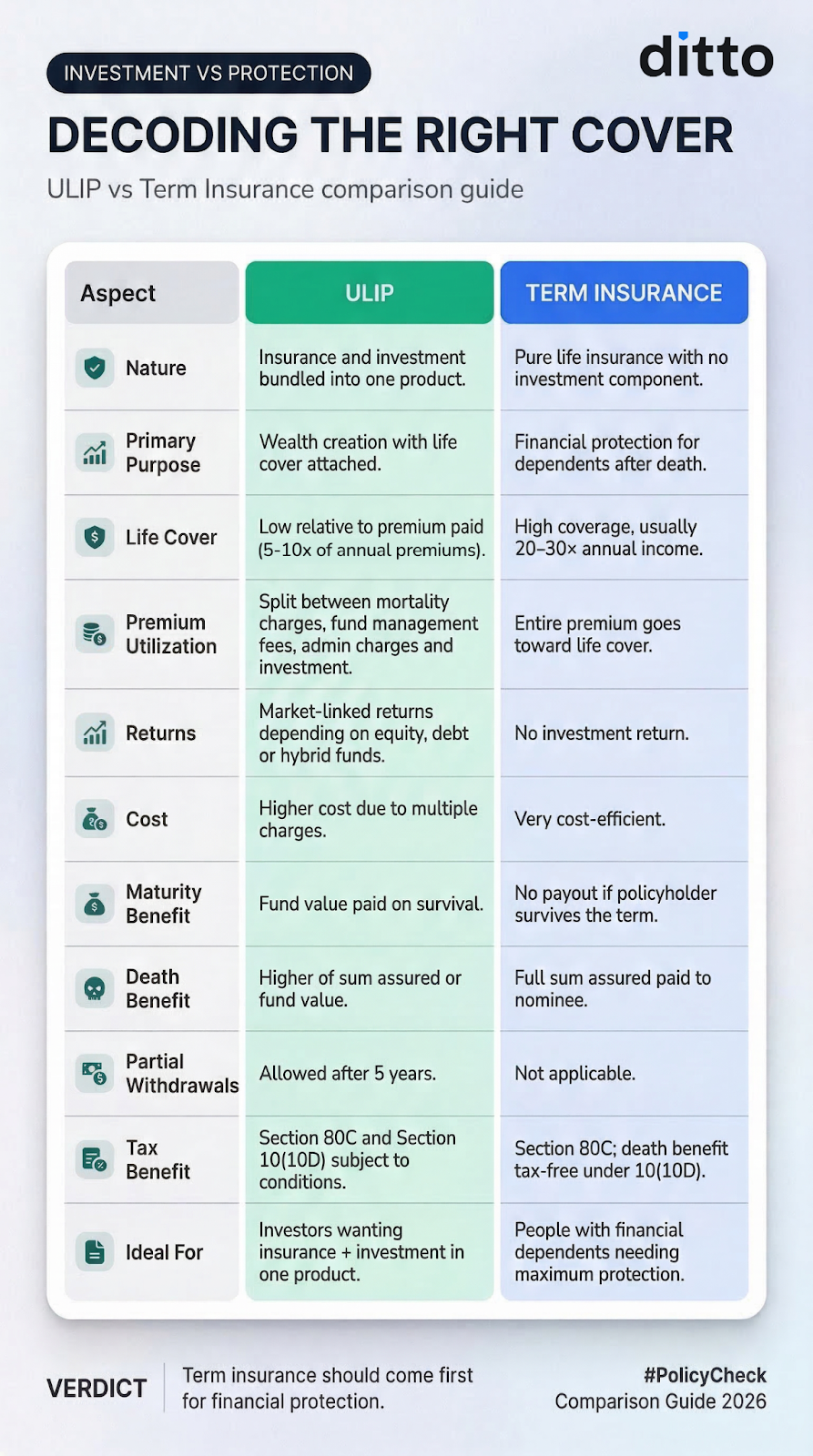

ULIP vs Term Insurance: Which Is Better?

To understand how ULIPs compare with simpler alternatives, you can also read our detailed guide on ULIP vs term insurance.

Premium Illustration for Canara HSBC Life Insurance ULIPs

Note: Projected values are illustrative and based on assumed returns of 4% and 8%. Actual returns may vary depending on fund performance, charges (such as mortality, fund management, and policy administration), and market conditions. ULIPs do not offer guaranteed returns. The figures are extracted from the Canara HSBC Promise4Growth Plus brochure.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Ditto's Take

Canara HSBC Life Insurance ULIPs involve multiple decisions, such as choosing variants, fund options, switching strategies, and premium structures. This requires ongoing involvement and a clear understanding of market movements.

Some plans have higher minimum premium requirements and relatively lower life cover multiples. Multiple charges, especially in the early years, can reduce overall efficiency and make the product harder to manage.

From a cost perspective, if a 21-year-old wants ₹1 crore life cover till age 40, a term plan can usually offer this at a much lower premium. In comparison, ULIPs allocate part of the premium toward insurance and policy charges, making them less efficient for pure protection.

At Ditto, we do not recommend or sell ULIPs. This is because combining insurance and investment often leads to higher costs, lower transparency, and reduced flexibility compared to buying term insurance and investing separately.

For most buyers, a simpler approach works better. Buy term insurance for coverage and keep investments separate through options like mutual funds, the Public Provident Fund (PPF), or Fixed Deposits (FDs).

Frequently Asked Questions

Last updated on: