Quick Overview

Bandhan Life Insurance leverages advanced technology to make life insurance more accessible and user-friendly. The solutions offered align with the needs of a digitally connected generation seeking simple and convenient financial protection.

This guide walks you through Bandhan Life ULIP plans, their features, charges, projected returns, performance metrics, and how they compare with term insurance plus Systematic Investment Plans (SIPs) for long-term financial planning.

Bandhan Life Insurance: Performance Metrics

Note: The above metrics reflect the overall performance of Bandhan Life Insurance and are not limited to its ULIP portfolio.

ULIP Plans Offered by Bandhan Life

Premiums for Bandhan Life ULIP Plans

Note: Projected values are illustrative for a 35-year-old. Actual returns are not guaranteed and depend on market performance. The figures listed are taken from the iInvest Advantage Brochure, iInvest II Brochure, and ULIP Plus Brochure.

Drawbacks of Buying a Bandhan Life ULIP Plan

- Limited Life Cover: Bandhan Life ULIP plans like iInvest Advantage and iInvest II offer life cover up to 20x the annual premium. Even with this multiplier, ULIPs typically provide lower protection than a standalone term plan for the same budget.

- Multiple Charges Reduce Investment Returns: ULIPs include charges for fund management, mortality, and premium allocation. These deductions reduce the amount invested and can affect long-term compounding, especially in the initial years.

- Mandatory Lock-in Period: ULIPs have a 5-year lock-in under IRDAI rules. If discontinued before the 5-year lock-in ends, the money is transferred to the Discontinued Policy Fund and becomes payable after the lock-in period, as per policy and regulatory terms.

- Limited Investment Choice and Tax Conditions: Investments are restricted to the insurer’s funds. Maturity is tax-free only if the premium stays within 10% of the sum assured and annual premiums remain within prescribed limits. For policies issued after February 2021 with annual premiums above ₹2.5 lakh, maturity proceeds become taxable, but your death benefit remains exempt.

Note: Some ULIPs, such as Bandhan Life iInvest Advantage, highlight zero premium allocation charges. While this can be beneficial, it reflects only part of the cost structure. Other charges, such as mortality charges, fund management charges, and policy administration fees, may still apply, so the overall cost of the ULIP should be evaluated carefully.

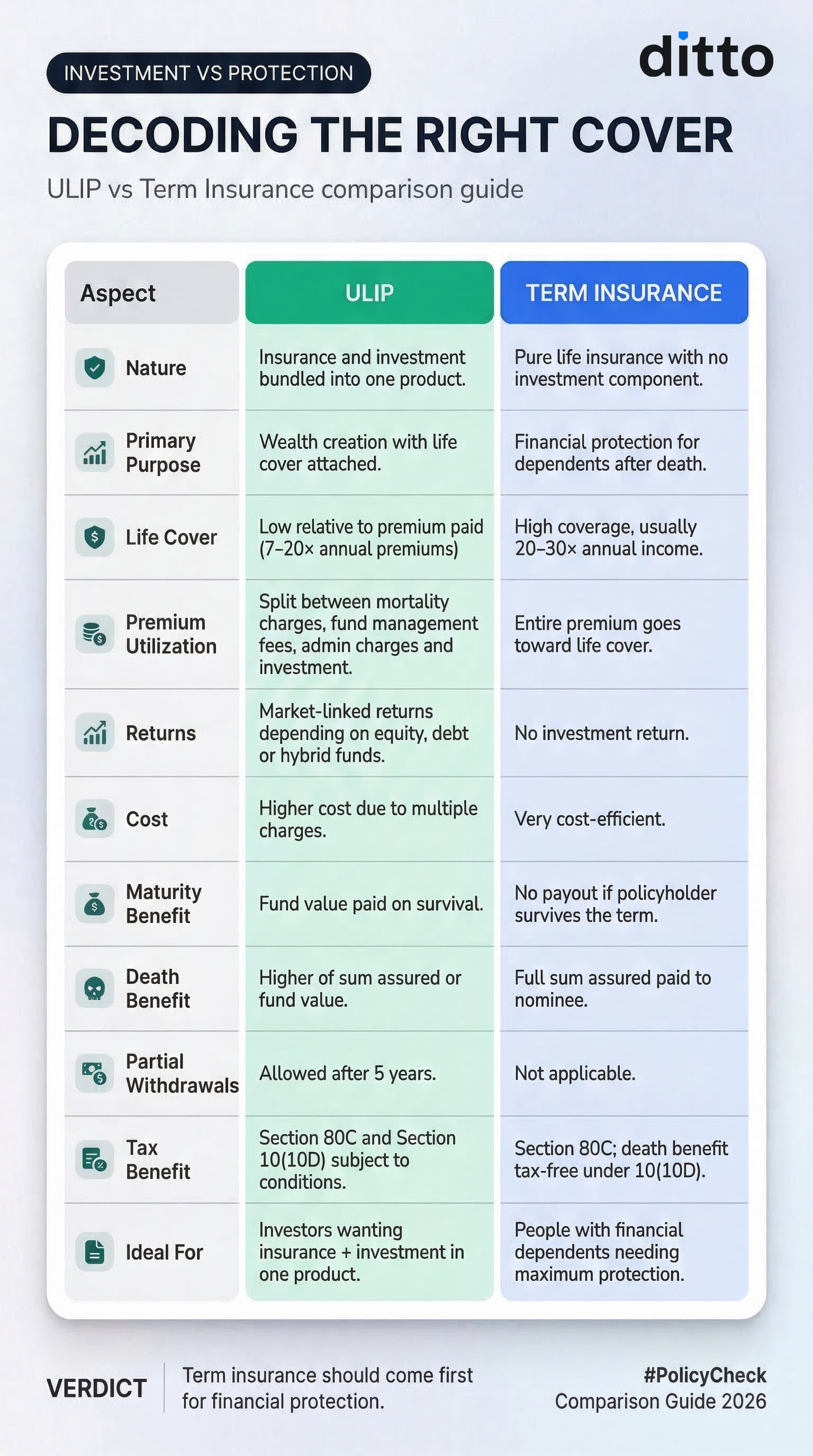

ULIP vs Term Insurance: Which is Better?

The difference between ULIP and term insurance lies in their purpose. ULIPs combine life insurance with market-linked investments, while term insurance focuses purely on providing higher life cover at a lower cost.

Check out the Infographic to have a clearer understanding.

Numerical Illustration:

Let’s take an example of a 30-year-old who invests ₹20,000 per month:

- If they opt for a ULIP, they invest ₹20,000 per month for 20 years to build wealth while maintaining life cover.

- If invested separately, they invest ₹12,000 per year for a ₹1 crore term plan, and the remaining ₹19,000 per month is invested in a mutual fund SIP.

Comparision Table

Note: This calculation is a generic illustration comparing a ULIP with a Term Insurance + SIP strategy. Actual returns depend on market performance.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right term insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or WhatsApp us now, slots fill up fast!

Conclusion

Bandhan Life ULIP Plans may suit certain investors based on their insurance eligibility and investment preferences. They can work for individuals who are not eligible for term insurance due to medical conditions or high-risk occupations. They may also appeal to people who already have adequate term cover but want an additional investment-plus-insurance product.

However, many people still choose to buy a standalone term insurance policy for protection and invest separately through options like SIPs. This approach can provide higher life cover, potentially better returns, and greater flexibility in managing investments.

Bandhan Life shows excellent CSR, ASR, and strong solvency, reflecting reliability. However, it operates on a small scale with modest annual business and death claim volumes, and while complaints are relatively high, they have been improving.

If you are looking for a term plan from insurers with established track records, we recommend the best term insurance plans, which align with your future goals and family needs.

Note: Bandhan Life is not Ditto’s partner insurer. At Ditto, we do not recommend ULIPs, and the information in this guide is based on publicly available sources and the insurer’s official website and is shared for educational purposes only.

Frequently Asked Questions

Last updated on: