Quick Overview

Axis Max Life Insurance is one of India's leading private life insurers, formed through a joint venture between Axis Bank and Max Financial Services. Earlier known as Max Life Insurance, it was officially rebranded as Axis Max Life Insurance on December 13, 2024. Currently, Axis Bank holds a significant strategic stake in the company.

Axis Max Life’s product portfolio covers term insurance, unit-linked insurance plans (ULIPs), savings plans, retirement plans, and group insurance. The ULIP range is among the most actively distributed offerings, available through Axis Bank branches, the company's direct online channel, and an independent agent network across India.

This guide explains how Axis Max Life Insurance ULIP plans work. It also reviews the insurer’s key performance metrics and compares some of its popular ULIP plans.

Axis Max Life Insurance: Performance Metrics

Note: The above metrics reflect the overall performance of Axis Max Life Insurance and are not limited to its ULIP portfolio.

Key Insights:

- CSR rose from 99.51% (FY 2023) to 99.70% (FY 2025), with a 3-year average of 99.62%, which is well above the industry average of about 98.66%. This means fewer than 1 in 100 claims are rejected.

- ASR improved sharply from 94.64% (FY 2023) to 97.38% (FY 2025), with a 3-year average of 96.40%. The narrowing gap between CSR and ASR suggests fair treatment of low and high-value claims.

- With a 3-year average of ₹10,719 cr, business volumes are growing steadily year-on-year and are significantly higher than the industry median of ₹3,411.73 cr. This indicates expanding distribution and rising demand for Axis Max policies.

- Death claims paid increased from ₹1,242 cr (FY 2023) to ₹1,452 cr (FY 2025), with an average of ₹1,316 cr. Rising payouts alongside high CSR signals consistent claim servicing as the insurer grows.

- Complaint ratio improved significantly from 10(FY 2023) to 3(FY 2025) per 10,000 claims, with an average of 5.67. The downward trend suggests improving claim handling and customer service.

- Solvency ratio stayed above the IRDAI requirement of 1.5x, with a 3-year average of 1.88x. The rebound to 2.0x in FY 24-25 indicates comfortable capital strength.

ULIP Plans Offered by Axis Max Life Insurance

Premiums for Axis Max Life ULIP plans

Note: Projected values are illustrative for a 40-year-old. Actual returns are not guaranteed and will depend on market performance. The figures are extracted from the Fast Track Super and Flexi Wealth Plus Plan prospectus.

Drawbacks of Buying an Axis Max ULIP Plan

- Life cover in ULIPs is usually up to 10x the annual premium. For example, a ₹1,20,000 premium gives roughly ₹12 lakh cover, which is often insufficient for most families. A standalone term plan can provide ₹1 cr or more at a much lower cost.

- ULIPs include multiple embedded charges such as fund management, mortality, and premium allocation charges. These deductions reduce the amount that actually gets invested and compounded, especially during the early years of the policy.

- All ULIPs have a mandatory 5-year lock-in as per IRDAI rules. If the policy is discontinued earlier, the money moves to a discontinued policy fund, earning about 4% per year, and life cover stops.

- Even though these plans offer multiple fund options, they are limited to the insurer’s in-house funds. Direct mutual fund investors have access to a much wider universe of funds across different asset managers.

- Fast Track Super follows an older ULIP design with relatively fewer additional benefits. While Flexi Wealth Plus has a cleaner structure compared with traditional ULIPs but still combines insurance and investment in one product. Online Savings Plan Plus Wealth includes multiple features and options, though the overall complexity may make it harder for some buyers to understand.

- Tax benefits are conditional. Maturity proceeds remain tax-free under Section 10(10D) only if the premium is within 10% of the sum assured. For policies issued after February 2021 with annual aggregate premiums (across all ULIPs) above ₹2.5 lakh, maturity proceeds become taxable. That being said, the death benefit remains exempt even for such high-premium ULIPs.

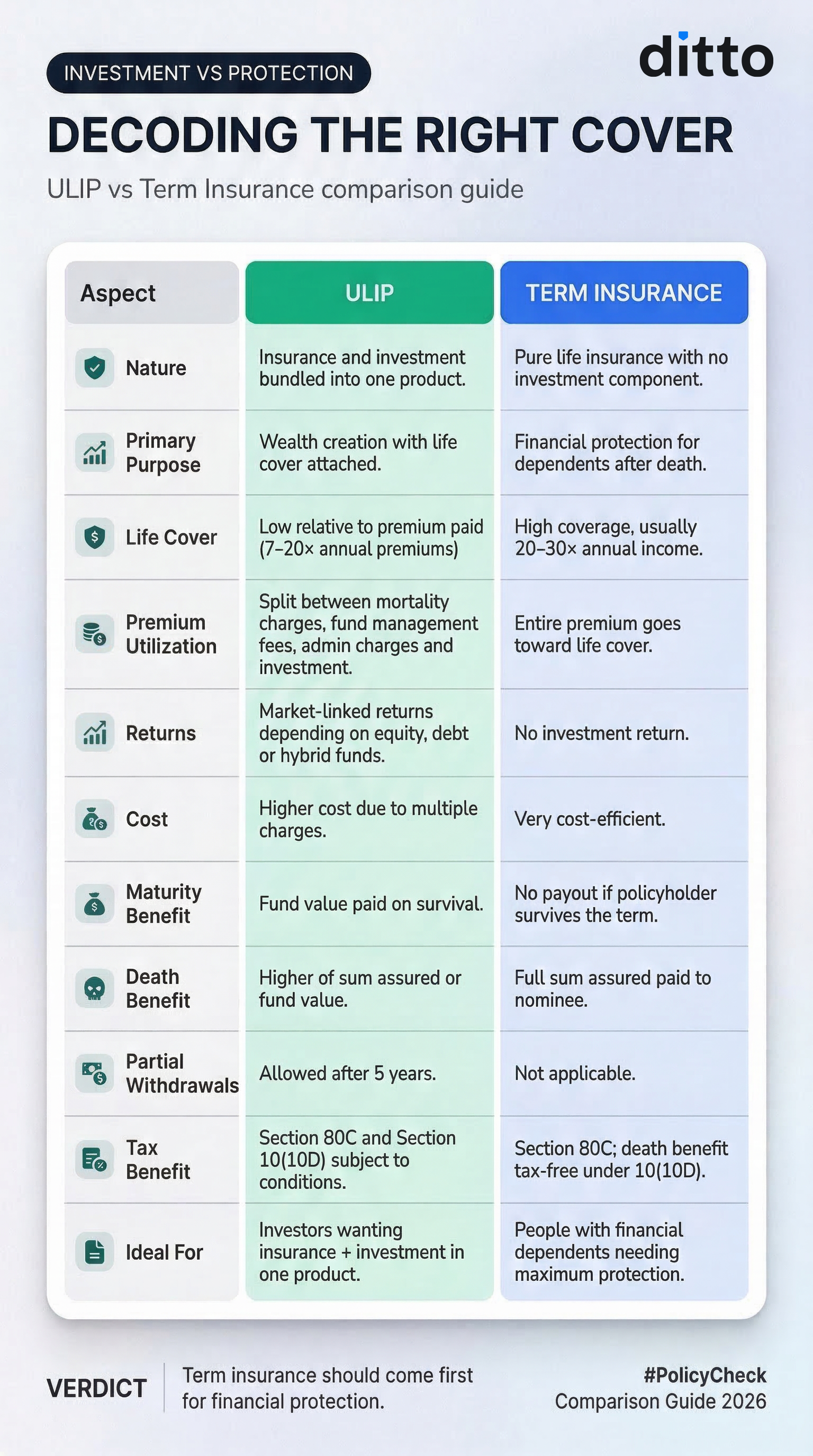

ULIP vs Term Insurance: Which is Better?

From a pure protection perspective, term insurance is a far stronger option. A ULIP that provides about ₹12 lakh cover on a ₹1,20,000 annual premium offers limited financial protection. In comparison, a standalone term plan can provide ₹2 cr or more in cover at a comparatively lower cost. Axis Max Life’s own term plans, such as Smart Term Plan Plus, can offer this level of cover for roughly ₹12,000 to ₹16,000 annually for a 25-year-old male.

From an investment perspective, low-cost equity mutual fund Systematic Investment Plans (SIPs) or the National Pension System (NPS) often deliver better long-term returns after charges. ULIPs include several embedded costs that reduce the effective compounding of your investment. Keeping insurance and investments separate allows you to choose better-performing funds, maintain flexibility, and clearly understand the costs and returns.

Check out the infographic below to understand the difference between a term insurance policy and ULIP.

Note: If you choose a Return of Premium Term Insurance (TROP) and survive the policy term, the insurer refunds the base premiums you paid. This may appeal to people who want their money back. However, premiums are much higher (about 50–100% more than regular term plans), the money does not grow, and rider premiums are not refunded, which is the primary reason why we don't recommend TROPs at Ditto.

Numerical Illustration: ULIP vs Term Insurance + Mutual Fund SIP

Let's consider a 30-year-old investing ₹15,000 per month (₹1.8 lakh per year) for 20 years to build long-term wealth while maintaining life cover.

Option 1: ULIP

Assume the market delivers about 12% annually, but ULIP charges reduce returns, resulting in a net return of about 10.5% after charges.

- Monthly Investment: ₹15,000

- Annual Premium: ₹1.8 lakh

- Life Cover: about ₹18 lakh (10× premium)

- Corpus after 20 years: ₹1.15 cr

Option 2: Term Insurance + Mutual Fund SIP

Instead, the individual buys a ₹1 cr term plan for around ₹12,000 per year. The remaining ₹14,000 per month is invested through a mutual fund SIP, earning around 11.5% annually after expenses.

- Annual Term Premium: ₹12,000

- SIP Investment: ₹14,000 per month

- Life Cover: ₹1 cr

- Corpus after 20 years: ₹1.21 cr

Comparison

Note: ULIPs do not charge a flat annual fee. Costs typically include premium allocation charges, policy administration charges, mortality charges, and fund management charges (capped at around 1.35%). Charges are usually higher in the early years and lower later, which is why the long-term impact often averages around 1.5% to 2.5% per year.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right term insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or WhatsApp us now, slots fill up fast!

Conclusion

Axis Max Life Insurance offers a range of Unit Linked Insurance Plans (ULIPs) that combine life insurance with market-linked investments. Some newer plans, such as the Flexi Wealth Plus Plan, include features like the return of mortality charges and lower policy administration costs, making them more efficient than older ULIP structures for long-term investors.

ULIPs may be suitable for certain investors depending on their insurance eligibility and investment preferences.

- Not Eligible for Term Insurance: Individuals who face rejection for term plans due to medical conditions or high-risk occupations. In such cases, insurers can offer ULIP plans as they come with a lower sum assured.

- Already have Term Cover: People with adequate term insurance who want an additional combined investment and insurance product.

- Prefer Disciplined Investing: Investors who value structured, long-term investing with a mandatory lock-in period.

However, buying a standalone term life insurance policy for protection and investing separately through options like SIPs or the Public Provident Fund (PPF) can provide higher coverage, potentially better returns, and greater flexibility.

If you are looking for a term plan from insurers with established track records and affordable riders, we recommend the best term insurance plans, which align with your future goals. When you choose a term insurance with the right coverage amount, policy duration, and term riders, it fulfills your family's needs.

Note: Axis Max Life Insurance is one of Ditto’s partner insurers, and its term plans are among the top recommended plans on our platform. At Ditto, we do not recommend ULIPs, and the information in this guide is based on publicly available sources and insurer disclosures and is shared for educational purposes only.

Frequently Asked Questions

Last updated on: