Quick Overview

Aditya Birla Sun Life Insurance Company Limited was established in 2000 as a joint venture between Aditya Birla Capital and Sun Life Financial. Headquartered in Mumbai, it is a private life insurer with a 51:49 shareholding split between Aditya Birla Capital Limited and Sun Life Financial (India) Insurance Investments Inc.

As part of its broader portfolio, ABSLI offers term insurance, ULIPs, savings/endowment plans, retirement plans, health plans, child plans, and group solutions, such as ABSLI DigiShield Plan, ABSLI Her Care term insurance for women, ABSLI Wealth Aspire Plan, and ABSLI Guaranteed Milestone Plan. In recent news, ABSLI launched its Super Term Plan in June 2025, reflecting a continued push into protection-led products.

This guide explains how Aditya Birla Sun Life Insurance’s ULIP plans work and reviews the insurer’s key performance metrics.

Aditya Birla Sun Life Insurance: Performance Metrics

Note: These metrics are for the entire life insurance portfolio of Aditya Birla Sun Life Insurance, and not just for their ULIPs.

Insights:

- CSR is slightly below the industry average, but still within a very tight range, indicating a stable and reliable claims approval experience overall.

- ASR is marginally lower than the industry average, indicating that while most claim amounts are honoured, a small proportion may remain unsettled, particularly in complex or high-value cases.

- Average complaints are significantly lower than the industry median, which is a strong positive indicator of good customer experience.

- Annual business volumes are substantially higher than the industry median, reflecting strong market presence, distribution strength, and scale of operations.

- Solvency ratio is below the industry median but comfortably above the regulatory requirement, indicating adequate financial stability, though with relatively lower capital buffers compared to peers.

ULIP Plans Offered by Aditya Birla Sun Life Insurance Company Limited

Note: Aditya Birla Sun Life Insurance also offers other ULIPs like Her Growth, Pram Suraksha, Wealth Infinia, Wealth Max, Wealth Secure, and Wealth Aspire. Refer to the respective brochures on ABSLI’S official website to see the Aditya Birla Sun Life Insurance policy details.

Premiums of Aditya Birla Sun Life Insurance ULIP Plans

Note: Projected values are illustrative for a 35-year-old. Actual returns are not guaranteed and will depend on market performance. The figures are extracted from the ABSLI Wealth Smart Plus plan page.

Drawbacks of Buying an Aditya Birla Sun Life Insurance ULIP Plan

Multiple Charges Eat Into Your Returns

ABSLI ULIPs come with several charges: fund management fees (up to 1.35%), mortality charges, and others. Even if some plans promise to return charges later, the money is still deducted upfront, which slows down compounding, especially in the early years.

Life Cover is Usually Not Enough

Most ULIPs offer life cover of around 7–10 times your annual premium. So if you’re paying ₹1 lakh a year, you might only get ₹10 lakh in cover, which is far from enough for most families.

You’re Locked In for 5 Years

Like all ULIPs, you can’t access your money freely for the first 5 years. If you exit early, your funds move to a low-return pool (4%), and your life cover stops.

You’re Limited to Their Funds

Even though ABSLI offers multiple fund options, you’re still choosing from their in-house funds. With mutual funds, you get access to a much wider universe and better-performing options across the market.

Tax Benefits Aren’t Always Straightforward

Tax-free maturity (under Section 10(10D)) comes with conditions. If premiums are too high relative to the cover, or cross ₹2.5 lakh annually (for newer policies), your returns could end up being taxed.

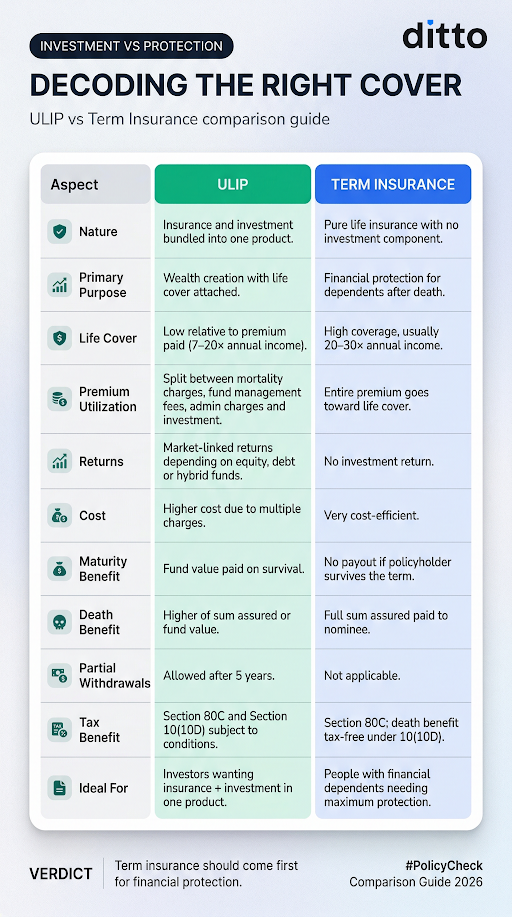

ULIP vs Term Insurance: Which is Better?

ULIPs combine insurance and investment in a single product, but this bundling often comes with trade-offs, like lower life cover and reduced net returns due to multiple charges. Because of this, many people prefer separating insurance and investments for better flexibility and outcomes. For a detailed breakdown, check out our guide on ULIPs vs term insurance.

Numerical Illustration based on Aditya Birla Sun Life ULIP plans

Consider a 35-year-old individual investing ₹1,00,000 annually for 20 years to build a retirement corpus while also ensuring financial protection.

Option A: ABSLI ULIP

Here, P.A. refers to per annum.

Option B: Term Insurance + Direct Mutual Fund Systematic Investment Plans (SIP)

The Difference

Note: Figures are illustrative and based on assumed returns. Actual outcomes will vary.

At lower effective returns (after charges), ABSLI ULIP outcomes can be modest. For instance, in the example above, a total investment of ₹5 lakh grows to around ₹15.7 lakh over 20 years, reflecting the impact of charges and capped return assumptions.

Check out the infographic below to understand the difference between a term insurance policy and ULIP.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp!

Conclusion

Aditya Birla Sun Life Insurance ULIPs offer a range of options with flexible investment strategies, decent fund choices, and added features like charge refunds and loyalty additions. However, like most ULIPs, they come with multiple embedded costs and relatively lower life cover. If your goal is disciplined, long-term investing with bundled insurance, these plans can work.

That said, if you specifically prefer the Aditya Birla group, it may be more efficient to consider the Aditya Birla Super Term Plan, which is among the top term insurance plans recommended by Ditto, and pair it with mutual fund SIPs for investing.

Overall, for higher returns and stronger protection, a combination of term insurance and mutual fund SIPs is often a more effective approach.

Disclaimer: Aditya Birla Sun Life Insurance is not a partner insurer. The information presented in the article is taken from publicly available sources like the insurer’s website and is for educational purposes only.

Frequently Asked Questions

Last updated on: