Quick Overview

Health insurance renewal is not just about paying the premium. It is a decision point. This is when you need to pause and ask whether sticking with your current insurer still makes sense. Should I renew my existing health insurance, or is it time to move to a better insurer?

In this article, we will walk you through whether to renew your existing health insurance, the signs of a weak insurer, renewing versus porting, how portability works, and how to compare insurers.

Signs Your Health Insurer Has Weak Metrics

Low Claim Settlement Ratio (CSR)

- The CSR tells you what percentage of claims your insurer settled. A CSR below 85% is a clear red flag.

- Do not rely on the insurer's brochures, as those numbers may reflect data for a specific quarter or month and can mislead you.

High Complaint Volume

- IRDAI publishes complaint data for every registered insurer, measured as the number of complaints per 10,000 claims, and it can also be checked in the insurer's NL-45 filings.

- The industry average sits at 27.06 complaints per 10,000 claims, so anything above this is a warning sign.

- A high complaint volume means delays in claims processing, excessive documentation demands, or disputes over what is covered.

Limited Network Hospitals

- A low hospital network means fewer cashless options when an emergency strikes.

- What also matters is whether the hospitals in your city, your area, or the places you travel to frequently are in that network.

- If there are no good empaneled hospitals in your locality, you might end up paying out of pocket first and claiming reimbursement later.

Did You Know?

Solvency Concerns

- IRDAI requires insurers to maintain a minimum solvency ratio of 1.50.

- If an insurer's solvency ratio is close to or below this level, it signals financial strain that could affect its ability to honor future claims.

Frequent Claim Rejections

- Some health insurance claim rejection reasons are fair. For example, not disclosing a pre-existing condition, filing a claim during the waiting period, using a non-network hospital for a cashless claim, or letting the policy lapse.

- But if your insurer is consistently finding reasons to reject or partially settle claims that should clearly be covered, that is a different story.

- Things like questioning the necessity of the procedure, citing vague clauses, or demanding excessive documentation are red flags. A good insurer settles valid claims without making you fight for them.

Should You Renew or Port Your Health Insurance?

When to Renew and Stay

- Strong Insurer Metrics: CSR above 90%, low complaints, and no solvency concerns.

- Waiting Periods Served: If you have completed 2 or 3 years of a 3-year pre-existing disease waiting period, staying puts you close to full coverage.

- High Bonus Accumulated: A substantial bonus increases your effective sum insured. Losing it by switching may not make financial sense.

- Moratorium Period Crossed: After 5 consecutive years with the same insurer, they can no longer reject a claim on the grounds of non-disclosure, except in cases of proven fraud. If you have crossed this threshold, you have built real loyalty benefits, and the claims process tends to be smoother.

- Decent Plan Features: If your policy already covers what you need, there is no strong reason to move.

- Migration: If you are satisfied with the insurer but need better features, a higher sum insured, or fewer restrictions, migrating to another plan within the same insurer can be a smarter move than switching insurers entirely.

When to Port

- Consistent Claim Rejections: If your insurer has a consistent track record of rejecting claims and you have also faced similar issues, it's recommended to port since that record is unlikely to improve.

- Poor Plan Features: Restrictive sub-limits on modern treatments, no restoration benefits, or tight room-rent caps most affect your hospital bill coverage.

- New Policy with No History: A 1- to 2-year-old policy whose features do not match your needs is a good reason to port before you are too far into the waiting periods.

- Suspected Non-Disclosure: If there was an undisclosed pre-existing condition when the policy was bought, it creates a risk of claim rejection. Always disclose your full health history while porting.

- No Good Advisor: If you bought the plan without proper guidance and are not sure it suits your needs, renewal is a good time to review it with an expert like Ditto.

Ditto Claim Story: A Switch at Renewal that Paid Off

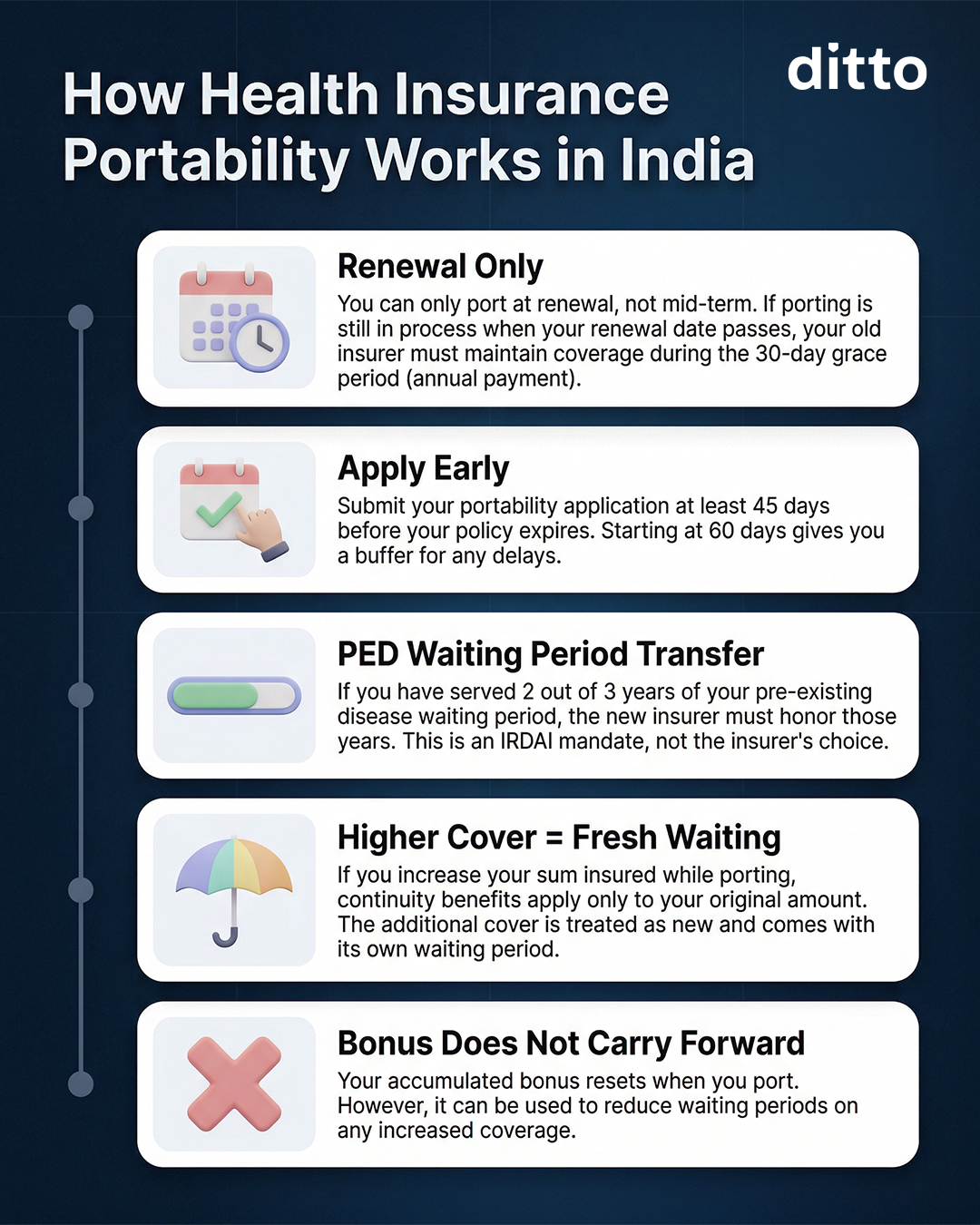

How Health Insurance Portability Works in India?

Health insurance portability is an IRDAI-mandated option available to all policyholders. Check out the infographic below for what you need to know.

Note: The new insurer may reject your porting application due to underwriting based on your existing medical history.

Ditto’s Industry Take

How to Compare Insurers Before Renewing or Switching?

Use these metrics as your checklist before making a decision.

At Ditto, we look at 3-year average performance metrics. That’s because one good year can be a coincidence, but three consistent years show how the insurer actually performs.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or chat on WhatsApp with us now!

Ditto's Take

Renewing your health insurance is an annual decision that directly affects your financial safety net. Here is our honest guidance:

- If your insurer has a CSR above 90%, the PED waiting period is over, and you have crossed the moratorium period, then renewing is almost always the right call.

- If you have had claims rejected for unfair reasons, your plan has sub-limits, the insurer has solvency concerns, or you bought the plan without proper advice, then the next renewal is your window to course-correct.

If you’re exploring other insurers to port your policy, refer to our guide to the best health insurance companies in India for a clear comparison.

Frequently Asked Questions

Last updated on: