Quick Overview

Health Insurance premiums aren’t the same for everyone. The cost of the same plan can vary based on multiple factors, which makes checking the premiums upfront essential.

If you're looking for the IndusInd Health Insurance premium chart, note that there's no single downloadable chart. Premiums are user-specific, calculated based on your individual profile.

In this article, we break down what the IndusInd health insurance premium chart shows, which factors affect your premium, and how to use their online calculator to get an accurate quote.

What the IndusInd Health Insurance Premium Chart Shows?

IndusInd General Insurance doesn't publish a one-size-fits-all premium chart PDF. What they do offer instead are sample premium illustrations that give you a ballpark idea, along with an online calculator to provide your exact quote.

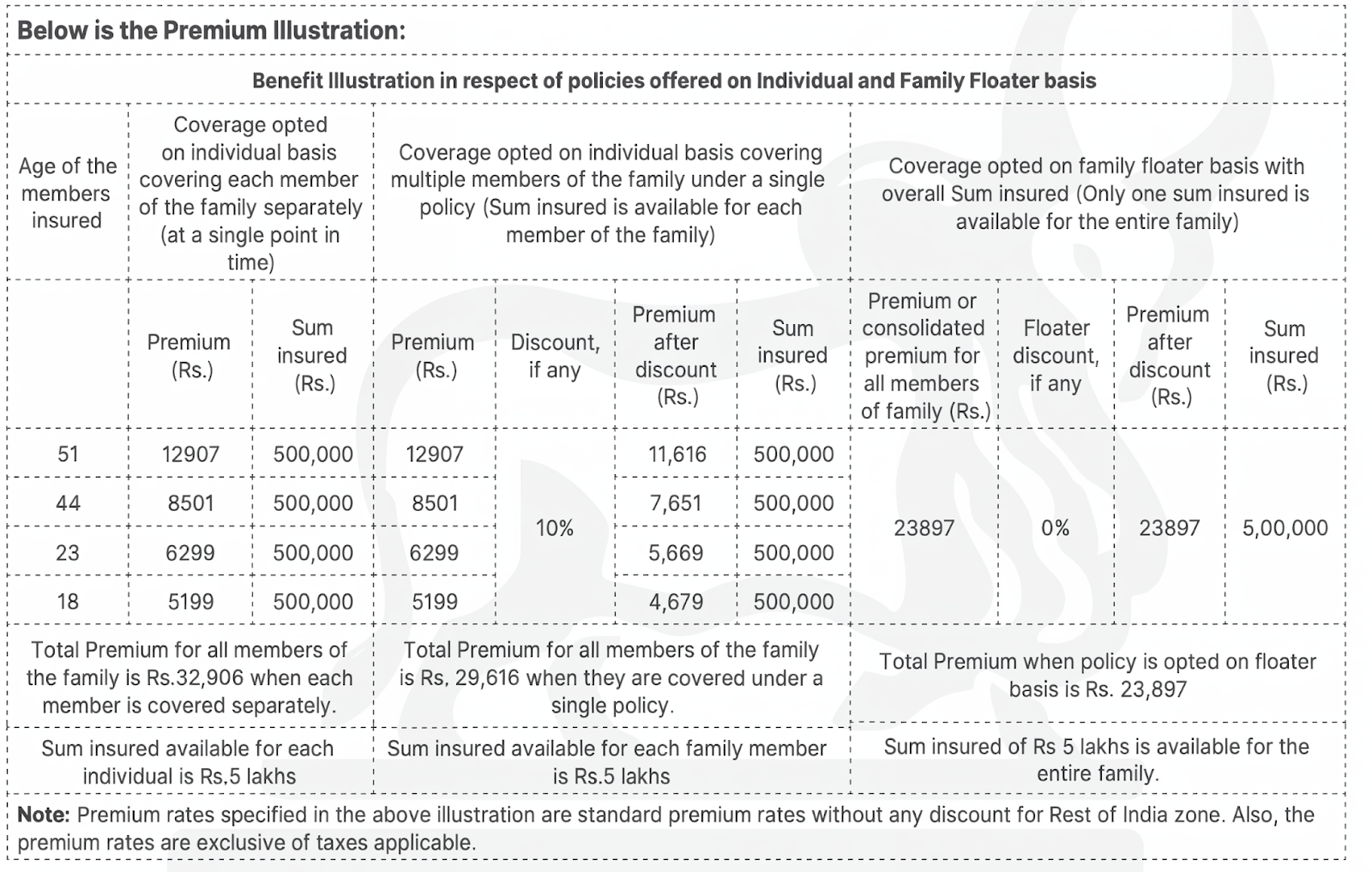

Here's a sample illustration from the Health Infinity plan:

Age-Wise Premiums

Premiums increase with age due to higher health risks. The increase from age 44 to 51 alone is around ₹4,000, underscoring how premiums can rise as you age.

Zone-Wise Premiums

Some policies are divided into zones, and premiums vary by location. The premium illustrated above is for Zone B. The policy is divided into the following zones:

- Zone A: Delhi, New Delhi & NCR including Faridabad, Noida, Ghaziabad, Gurugram, Gautam Buddha Nagar, Mumbai & Suburbs, MMR (Mumbai Metropolitan Region), Navi Mumbai & Suburbs, Thane City & Suburbs, Mira Road, Bhayandar, Panvel, Kalyan & Dombivali, State of Gujarat, Kolkata & Suburbs.

- Zone B: Rest of India

It also has a zone-wise copayment, which is applicable as follows:

Individual vs Family Floater Premiums

The example compares the cost of covering a four-member family (ages 18, 23, 44, 51) under different plan types. A family floater is the most affordable at ₹23,897, about ₹9,000 cheaper than individual plans. However, the coverage is shared among all members, unlike individual or multi-individual plans, where each member gets a separate sum insured.

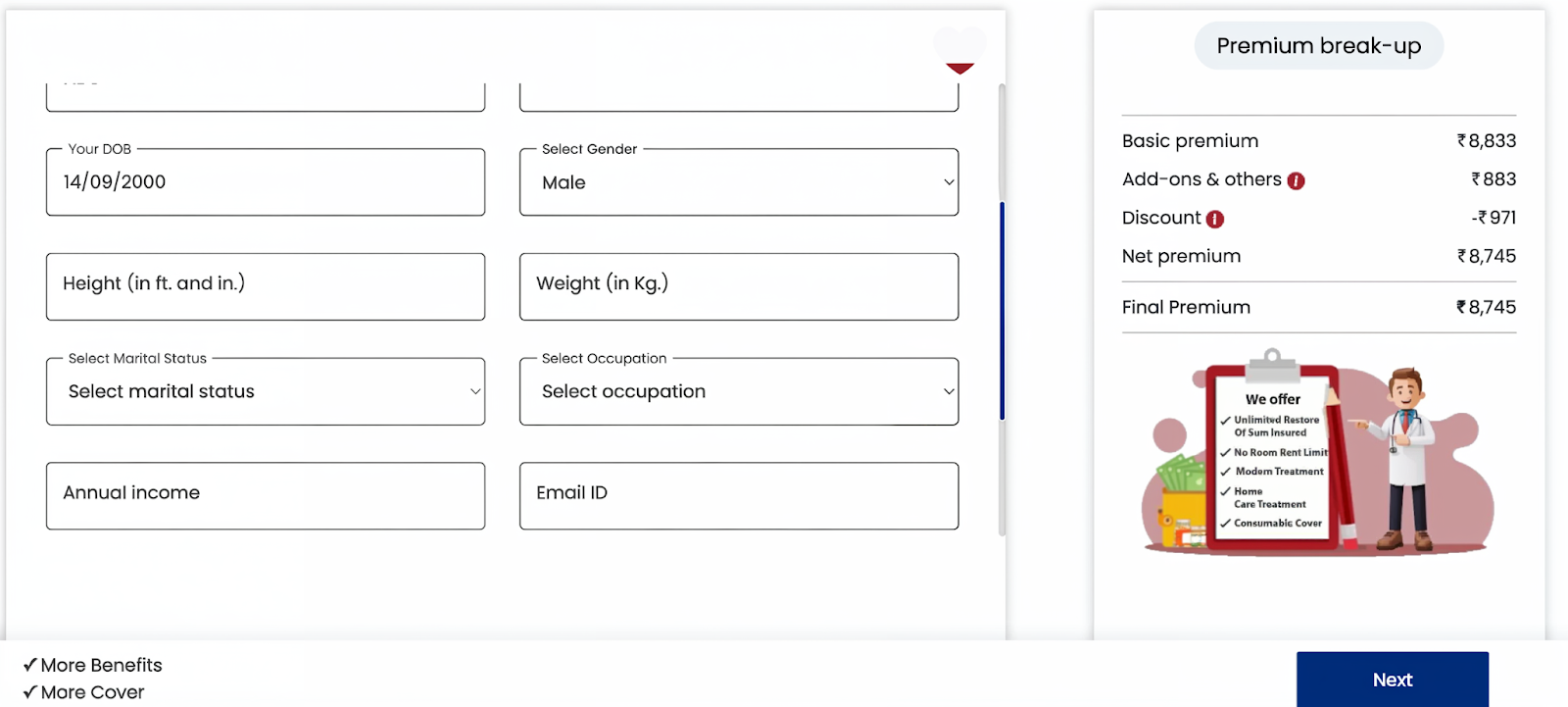

How to Calculate IndusInd Health Insurance Premium?

Induslnd Health Insurance premiums can be calculated online by following the steps mentioned below.

How to Calculate IndusInd Health Insurance Premiums Online?

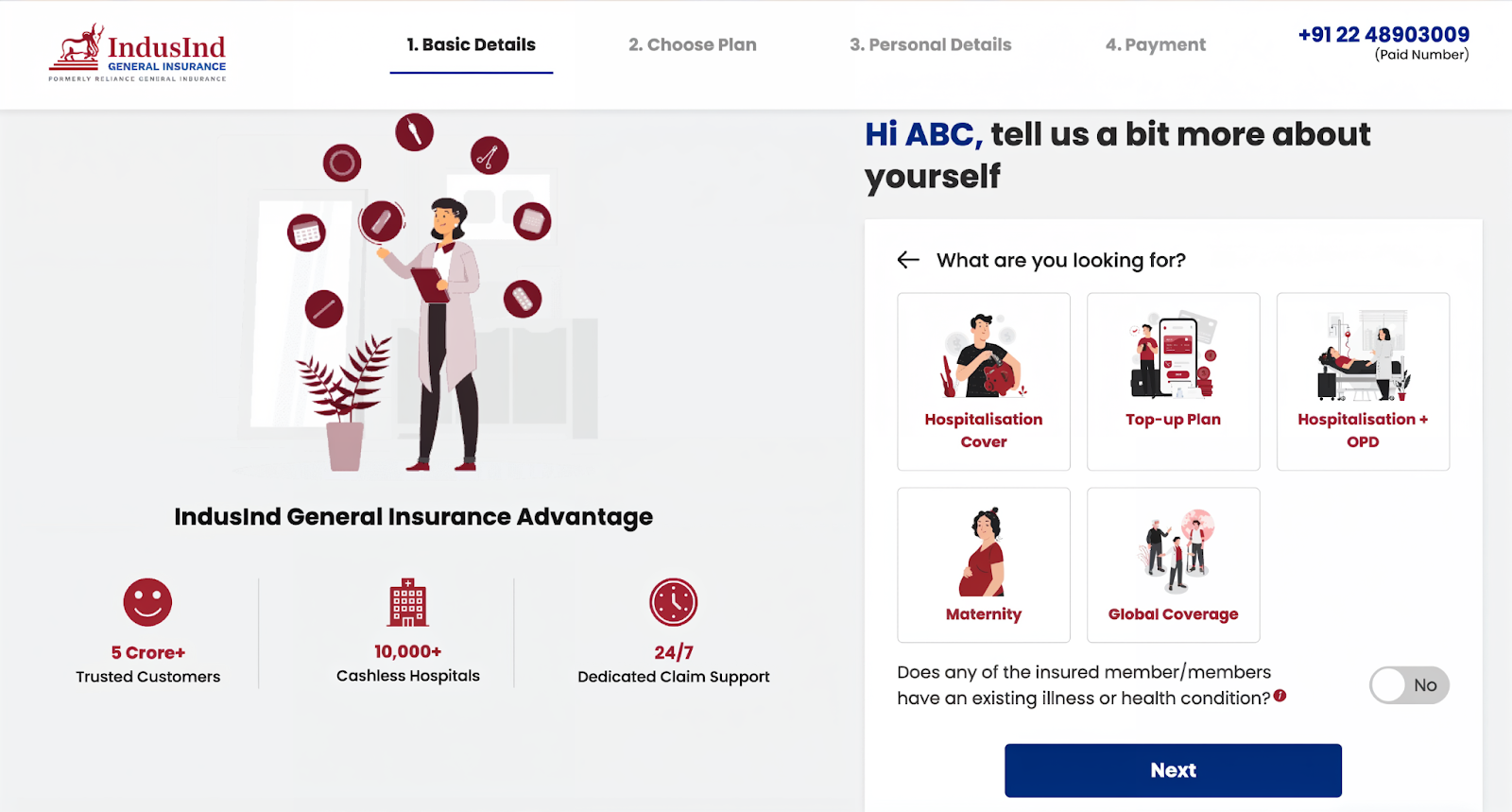

Step 1: Visit the official website and navigate to the health insurance section.

Step 2: Enter basic details, including your name, mobile number, pincode, and preferred policy start date. Accept the terms and verify your OTP.

Step 3: Choose your policy type: individual, family floater, or a plan for parents/in-laws.

Step 4: Add member details, such as dates of birth and relationships, for all members to be covered.

Step 5: Select coverage preferences: hospitalization cover, pre-existing conditions (toggle yes if applicable), and your preferred sum insured.

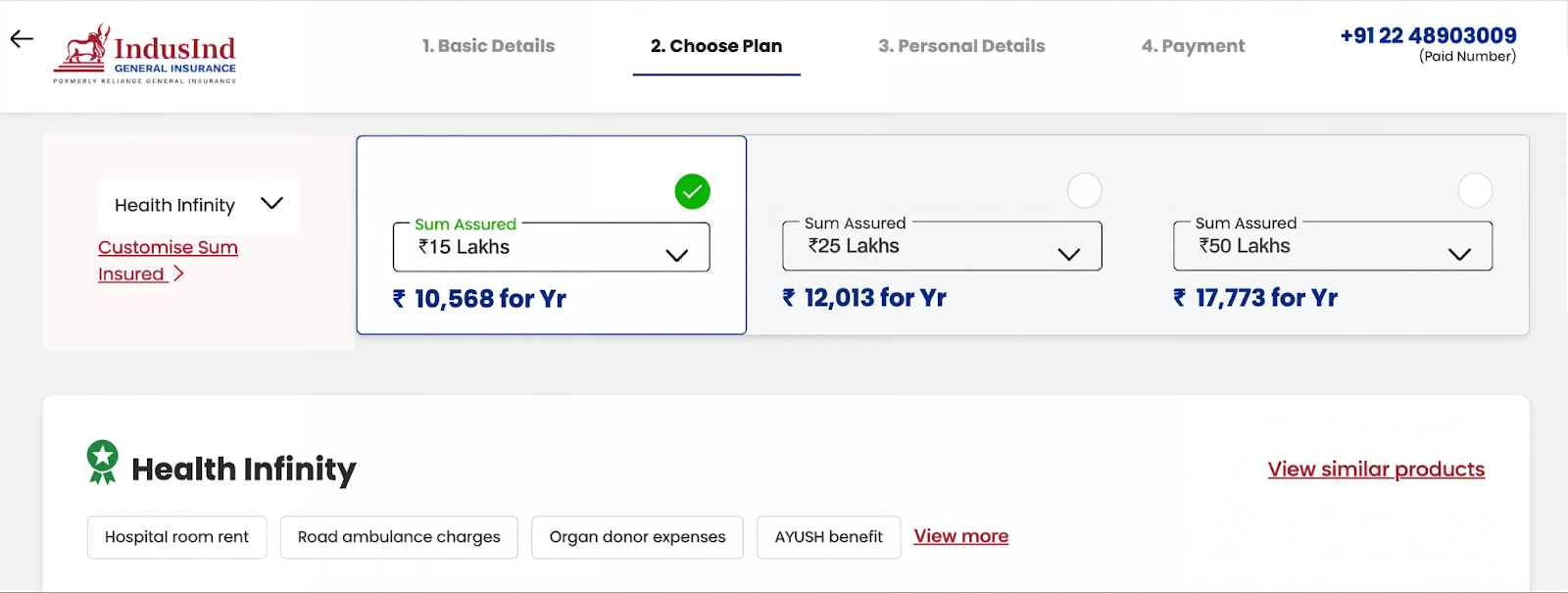

Step 6: The calculator will show recommended policies, coverage, and premiums based on your inputs. You can modify your selection by adding or removing riders, changing the sum insured, or tweaking other options, such as discounts.

Step 7: To proceed, add details like family size, date of birth, gender, basic lifestyle questions, and current coverage and annual income. Once everything checks out, make the premium payment to buy your new health insurance policy.

Factors That Affect IndusInd Health Insurance Premiums

Age

For individual policies, the insured member's completed age is used to calculate the premium. For family floater plans, the eldest member's age is considered. As age increases, so does the likelihood of claims, which is why premiums increase as you grow older.

Sum Insured

Higher coverage increases premiums, but not proportionately. For instance, the premium difference between ₹10 lakh and ₹20 lakh coverage is marginal, even though coverage doubles.

Policy Structure

IndusInd Insurance offers individual, multi-individual, and family floater plans. Individual plans are the most expensive since each member has separate coverage. Multi-individual plans cover everyone under a single policy but provide an individual sum insured for each member. Family floater plans offer a single policy with a shared sum insured for the entire family.

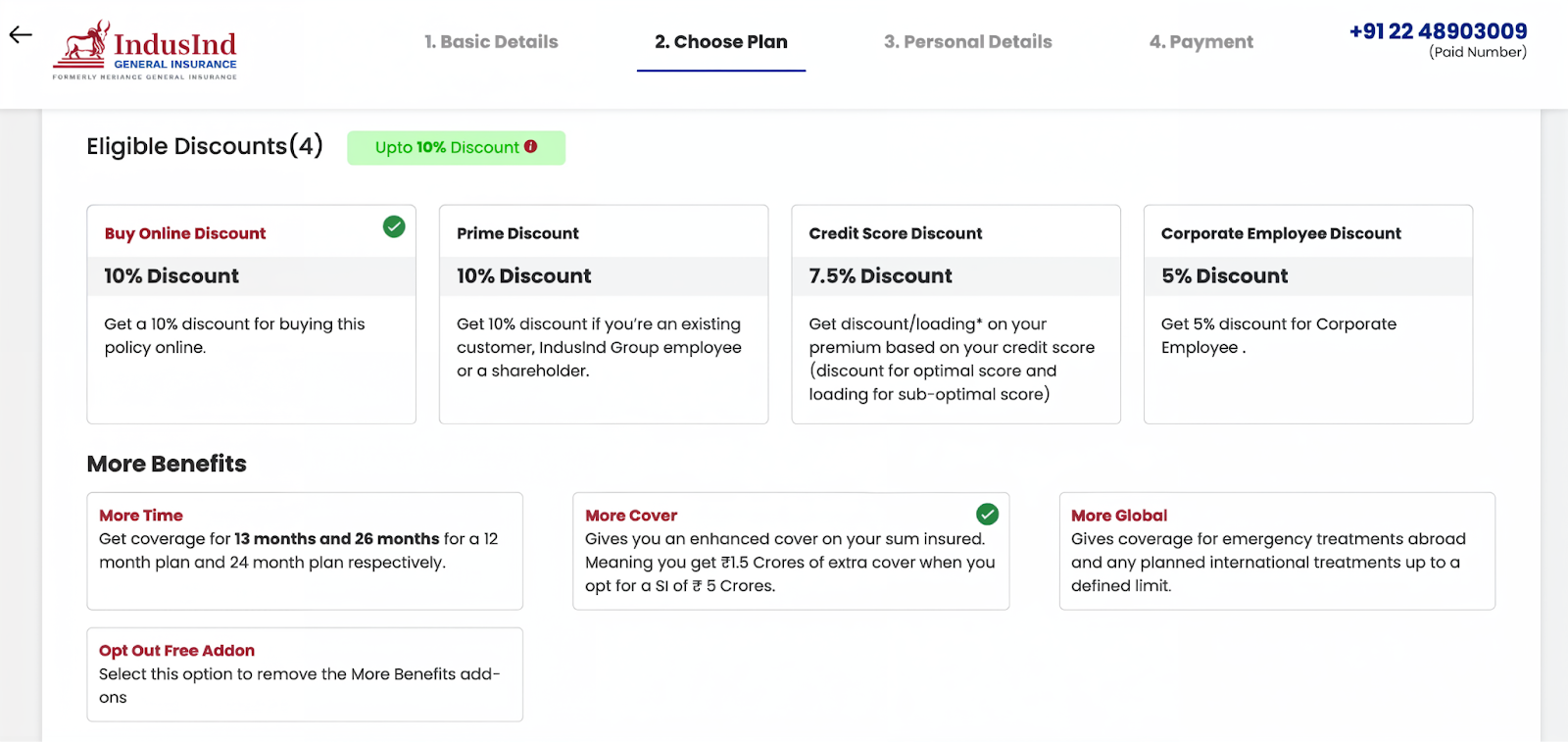

Discounts

IndusInd General Insurance offers discounts that can reduce your premium. Under the Health Infinity Policy, healthy and existing Reliance customers can get up to 10% off, and a good credit score can qualify you for an additional 7.5% discount. These reward consistent renewals and a healthy lifestyle.

Medical History and Underwriting

If any member on the policy has pre-existing conditions, lifestyle risk factors, or a notable medical history, the insurer may apply a loading charge to account for the higher risk. This is standard practice across most health insurers.

Popular IndusInd Plans With Their Premium Chart

To give you a clearer idea of how premiums vary across plans, here’s a quick comparison between two popular IndusInd health insurance plans: IndusInd Health Infinity Insurance and Health Gain Power policy.

Note: The premiums are calculated for healthy individuals living in Delhi (110010). These are illustrative premiums, and the final premium can vary based on channel discounts, opted add-ons, and insurer underwriting.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or chat on WhatsApp with us now!

Conclusion

IndusInd General Insurance keeps things simple with no rigid premium charts, just a flexible calculator that gives you a number based on your actual profile. Before you buy a policy, make sure the plan actually works for you, check the room rent limits, co-payment clauses, pre-existing disease waiting periods, and network hospitals.

Choosing the right plan can become overwhelming. As a first step, you can refer to our comprehensive guide on how to choose health insurance.

Disclosure: IndusInd Health Insurance is not a partner insurer of Ditto. Our assessment is independent and based only on publicly available information and the evaluation framework we apply to all insurers. For the most recent updates, we recommend checking the insurer’s official website.

Frequently Asked Questions

Last updated on: