Quick Overview

Launched on January 1, 2019, the scheme is designed to provide cashless health coverage to families left out of Ayushman Bharat, which was based on Socio-Economic and Caste Census(SECC) 2011 and Rashtriya Swasthya Bima Yojana (RSBY) data.

This guide explains the features, eligibility, application process, benefits, and limitations of Himcare to help you understand how it works and whether it meets your healthcare needs.

Did You Know?

Key Features of Himcare

- Under Himcare, beneficiaries can avail cashless hospitalization at empanelled hospitals without any upfront payment.

- The scheme provides coverage of up to ₹5 lakh per family per year on a family floater basis.

- Treatment is available at over 250 hospitals already empanelled under national or state health schemes.

- Depending on the beneficiary category, a nominal premium or contribution may be required under the scheme rules.

Take Note: Under Himcare, new registrations are open only for four months in a year: March, June, September, and December. The policy period for all new registrations and renewals is one year.

Inclusions and Exclusions of Himcare

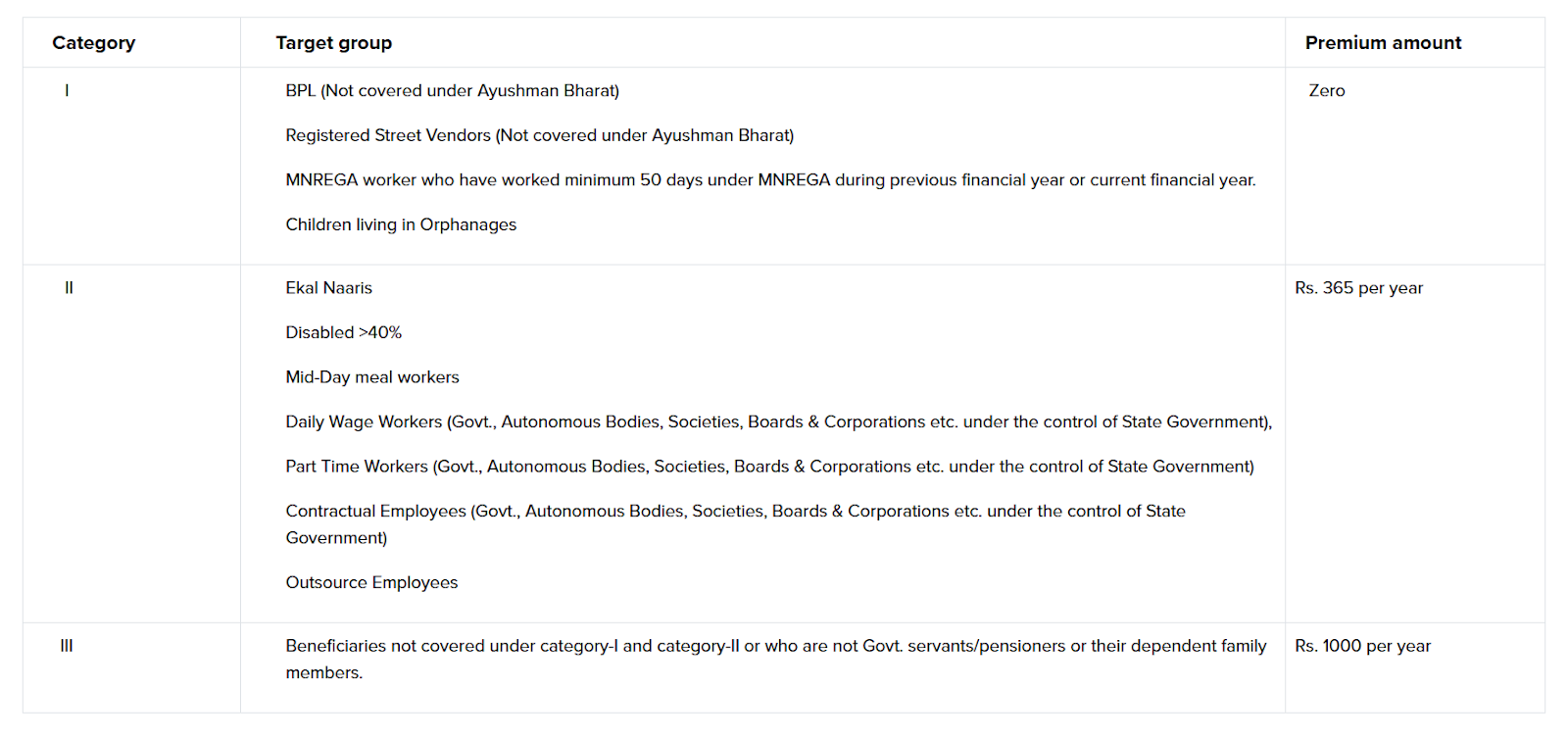

Premium Category for Himcare

Under Himcare, the scheme is implemented on a co-payment basis. Premium amounts vary depending on the beneficiary category, with differential premium rates prescribed as per eligibility and classification under the scheme.

Source: Himcare Website

Note: Hospitals empanelled under Ayushman Bharat within the State are also empanelled for Himcare. The beneficiaries can also take treatment under the scheme in Postgraduate Institute of Medical Education & Research (PGIMER) Chandigarh and Government Medical College & Hospital (GMCH) Sector 32 Chandigarh.

Eligibility Criteria and Application Process for Himcare

Eligibility Criteria

- Below Poverty Line (BPL) families who are not covered under Ayushman Bharat

- Registered street vendors who are not covered under Ayushman Bharat

- Mahatma Gandhi National Rural Employment Guarantee Act (MNREGA) workers who have worked at least 50 days in the current or previous financial year

- Children living in orphanages

- Ekal Naaris (single women)

- Persons with more than 40% disability

- Mid-day meal workers

- Daily wage workers under the State Government departments, boards, corporations, or autonomous bodies

- Part-time workers under State Government bodies

- Contractual and outsourced employees under State Government bodies

- Individuals who are not government servants, pensioners, or their dependent family members.

Take Note: Before applying or renewing your Himcare plan, you must submit a written undertaking confirming that the Head of Family and dependents are not covered under any Government medical reimbursement scheme meant for employees or pensioners.

How to Apply for Himcare?

Step 1: Visit the official portal of Himachal Pradesh Swasthya Bima Yojana Society and select the “Apply for Himcare” option.

Step 2: Check if the enrolment window is open.

Step 3: Fill in the online application form with personal and family details, Aadhaar information, category documents, and required certificates.

Step 4: Pay the nominal fee (if applicable), either online or through a Common Service Center (CSC) / Lok Mitra Kendra (LMK).

Step 5: Submit the form for verification. Upon approval, your Himcare e-card will be issued for cashless treatment at empanelled hospitals.

Note: Under the scheme, family details cannot be edited for 30 days before the policy expiry date. Additionally, beneficiaries are allowed to update or edit family details a maximum of two times during a single policy period. You can refer to the scheme guide for further application assistance.

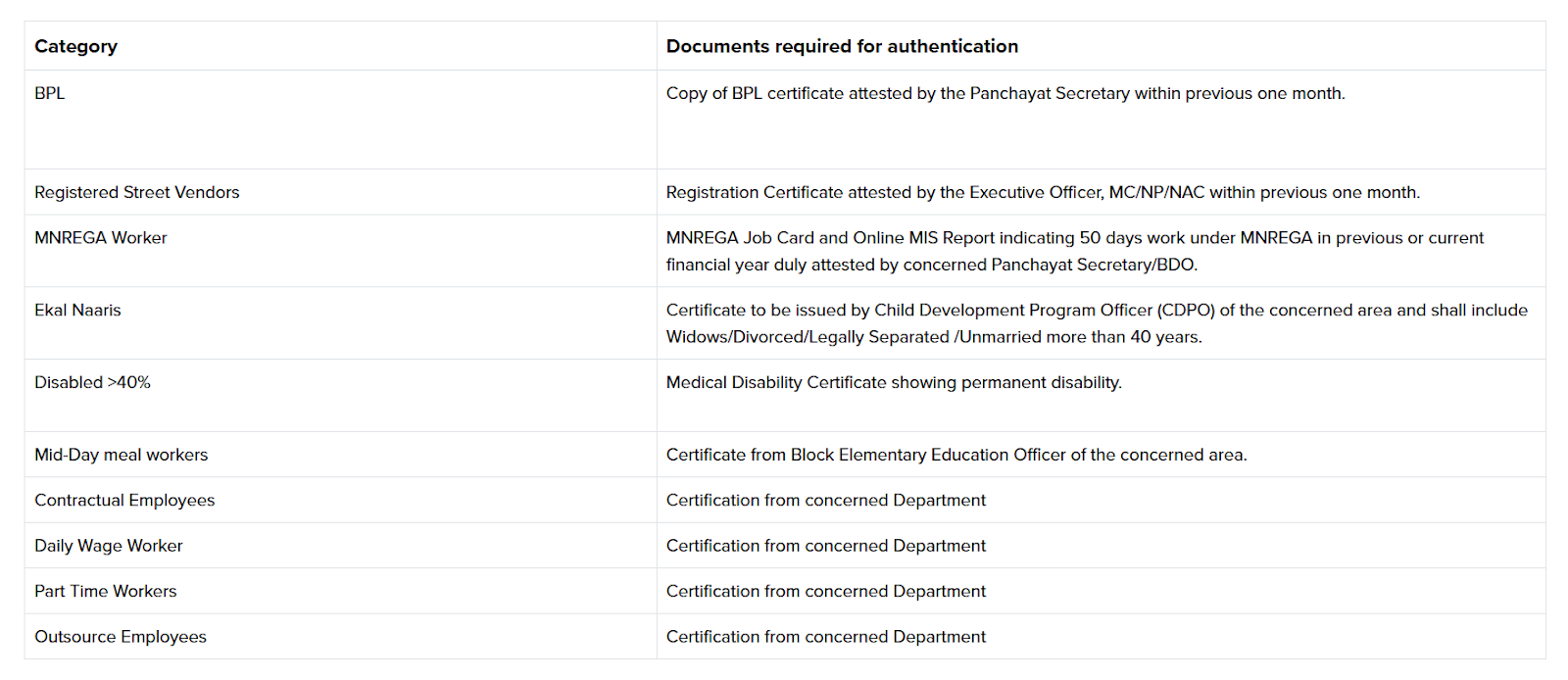

Documents Required To Apply For Himcare

Source: Himcare Website

Himcare vs Private Insurance: Is It Enough on Its Own?

Himcare offers cashless treatment at affordable or nominal contributions (depending on category), which helps reduce the burden of major hospital expenses. However, public healthcare infrastructure may not always be adequate and does not guarantee continuity, which can limit hospital options and accessibility in some areas.

For instance, with rising medical costs, a ₹5 lakh cover may not always be sufficient. For example, a complex cardiac bypass or cancer treatment in a metro hospital can easily exceed ₹6–₹10 lakh, leading to out-of-pocket expenses.

On the other hand, private health insurers like HDFC Ergo and Care Health provide comprehensive coverage and continuity independent of government policy changes.

Contact Details for Himcare

Why Choose Ditto for Your Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Here’s why customers like Abhinav love us:

- No Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Conclusion

Himcare acts as an important financial safeguard for families in Himachal Pradesh, offering affordable access to cashless hospitalization. While it provides meaningful protection against major medical expenses, some families may still consider additional private coverage for broader benefits and higher limits.

If you are looking for a health plan from insurers with established track records, we recommend comprehensive plans, which align with your long-term goals.

Note: Ditto has no affiliation with this scheme. Our assessment here is completely independent and based solely on publicly available data and the evaluation framework we use for all insurers. If you want to understand how Ditto reviews insurers across claims, complaints, business strength, and product suitability, you can read our methodology here. The information provided is for general awareness and should not be used for financial or legal decisions. Please refer to the official website of Himcare for the latest details.

Frequently Asked Questions

Last updated on: