As of September 22, 2025, Goods and Services Tax (GST) on health insurance has been removed entirely. The rate was reduced from 18% to 0%, making individual plans, family floater plans, and senior citizen policies completely tax-free. Group health insurance, such as employer-provided policies or bank-offered plans, still attracts 18% GST.

A 60-year-old in Delhi now pays ₹49,168 without GST instead of ₹58,018 including GST for a ₹15 lakh HDFC Ergo Optima Secure policy. This is a meaningful saving, specifically for older folks.

This guide is for anyone buying or renewing a health insurance plan and looking to understand the impact of GST on their premiums.

Till recently, one of the biggest hurdles to buying personal health insurance was the price. At Ditto, we’ve heard this concern often while helping customers choose the right health insurance cover. Even though health insurance is a necessity, it was subject to a 18% GST because IRDAI considered insurance a service provided to policyholders.

To address this imbalance, the central and state governments agreed to remove GST from retail health insurance products while continuing to levy it on group health insurance plans.

This article breaks down the current GST rate on health insurance, what it means for you, why group insurance is still taxed differently, and whether any further changes are coming.

Planning to buy insurance and confused about how GST impacts your premiums? Book a free call or WhatsApp us for clarity.

What Is the GST Rate on Health Insurance?

As of September 22, 2025, the GST on health insurance premium is 0%. This applies to:

Individual health insurance policies

Family floater plans

Senior citizen health insurance policies

Critical illness policies sold as individual plans

This decision was announced at the 56th GST Council meeting held on September 3, 2025, chaired by Finance Minister Nirmala Sitharaman. The official notification confirmed that the exemption will take effect on September 22, 2025.

Note: The exemption applies based on the date of premium payment, not the policy start date. If your renewal is after September 22, 2025, and you pay on or after that date, you automatically receive the 0% benefit.

CTA

How Does GST Affect Your Health Insurance Premium?

Earlier, GST on health insurance premiums in India stood at 18%. This hit senior citizens the hardest, with GST alone running into tens of thousands of rupees for some family floater plans. With the change in the GST component, the premiums have become affordable and accessible.

Let’s have a look at an illustrative example to see the impact of GST on premiums.

Profiles

Premium (including 18% GST)

Premium (excluding 18% GST)

Individual Plan (Age 25)

₹15,843

₹13,426

Family Floater, 2A, Ages (31, 32)

₹24,871

₹21,077

Family Floater, 2A 1C, Ages (35, 34, 5)

₹30,627

₹25,955

Senior Citizen, 2A, Ages (62, 63)

₹1,02,737

₹87,065

Note: A stands for adult and C stands for child. The premiums are calculated for the HDFC Ergo Optima Secure plan for a ₹15 lakh sum insured for individuals residing in Delhi (pincode 110010). These numbers are illustrative and may vary based on age, location, medical conditions, and chosen add-ons.

Key Insight

When a service such as health insurance becomes GST-exempt, insurers lose the ability to claim input tax credit (ITC) on their business expenses. This could force insurers to reduce agent commissions and nudge some of them to slightly increase base premiums to offset this loss. A few major insurers have begun imposing premium revisions.

Why This Reform Is a Win for You

Instant Savings

Your premium drops from the very next payment, no waiting around, no paperwork required.

Better Value for Families and Senior Citizens

Higher base premiums mean greater savings on floater and senior-citizen plans every year.

Room to Upgrade

Use the savings to add riders you skipped earlier, such as Outpatient Department (OPD) cover and non-medical expenses cover.

Higher Sum Insured, Same Budget

You can now consider moving to a larger cover without paying more than before, subject to medical underwriting.

GST on Group Health Insurance: Is It Different?

If your employer provides you with a group health insurance policy (also called corporate health insurance) or has a bank-provided policy, that still attracts 18% GST. The exemption announced in September 2025 is only for individual policies.

This means:

Your employer-sponsored health cover continues to have 18% GST built into the group premium.

The company pays this, but it does flow into the overall cost of employee benefits.

Employers that are GST-registered businesses may claim input tax credit for this expense, depending on whether group cover is mandated by law.

From your side as an employee, you don't pay the GST directly. But it does affect how much coverage your company can afford to offer within a given budget.

Note: If you rely only on your employer's group cover, this is also a good reminder to buy an individual plan for yourself. Group covers typically lapse the moment you switch jobs, and there's no GST component anymore for your own policy.

Latest Updates: Is GST on Health Insurance Being Reduced?

The GST exemption was the first of its kind since the comprehensive tax was introduced in India in 2017. For context, insurance penetration in India stood at roughly 3.7% of GDP in 2025, and the government's target is to take it to 8%. This change is part of a broader push that IRDAI calls "Insurance for All by 2047", aimed at making individual coverage more affordable and accessible across the country.

Is there anything more to expect? Group health insurance is still at 18% GST. As of now, there is no official announcement from the GST Council regarding a reduction in GST for group policies. For individual policyholders, the new GST rate on health insurance is 0%, which is already in effect and applies to all new purchases and renewals from September 22, 2025, onward.

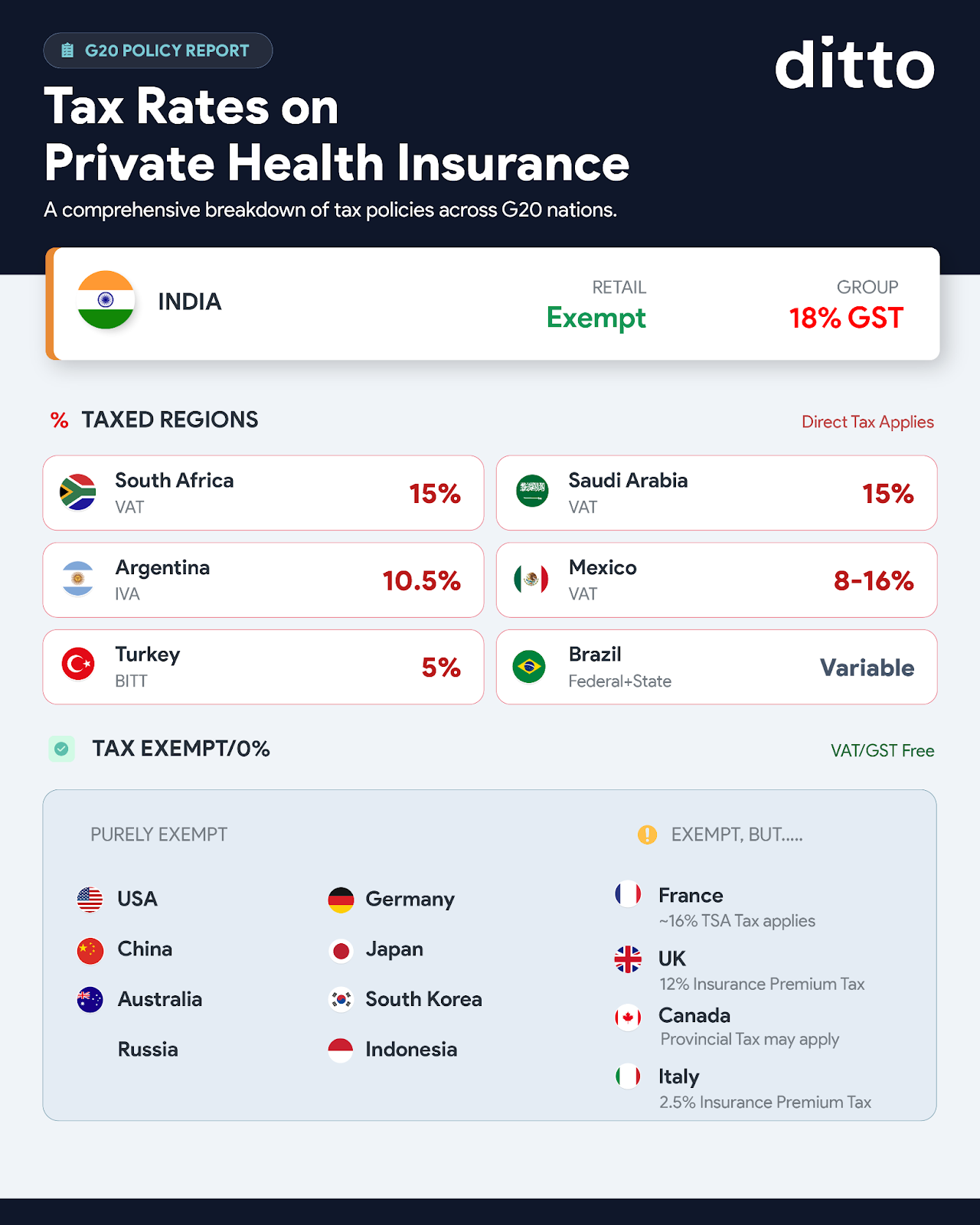

The following infographic shows the tax rates on private health insurance across G20 countries, including India.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Ditto’s Take on Removal of GST in Health Insurance

With insurers losing ITC benefits, we expect base premiums to revise over time. Locking in a multi-year health insurance policy today would lead to meaningful savings if that happens.

If your budget allows, consider using the GST savings to opt for a higher sum insured. At Ditto, we generally recommend a ₹15- ₹25 lakh cover to provide a buffer against rising medical costs.

The GST exemption does not apply to certain group health insurance policies. So, always confirm whether you’re buying an individual or group plan.

If you have a renewal coming up, double-check that your insurer has reflected the 0% GST in your updated premium quote. But if you haven't bought a policy yet, there's no better time to start. As a first step, you can refer to our complete guide on the best health insurance companies in India.

Frequently Asked Questions

What is the current GST rate on health insurance in India?

As of late 2025, the GST rate on individual health insurance premiums is 0%. This historic exemption was announced during the 56th GST Council meeting to make healthcare more affordable for the general public. However, it is important to note that this zero-tax benefit applies only to retail policies such as family floater and senior citizen plans.

Conversely, group health insurance provided by employers still carries a standard GST rate of 18%. This distinction ensures that individual taxpayers save significantly while corporate insurance costs remain subject to the regular service tax bracket.

Do I have to pay GST on senior citizen health insurance?

You no longer have to pay GST on health insurance for senior citizens, as the rate was slashed to 0% in September 2025. This change provides significant relief for older adults, who often face higher premiums due to age-related risks. For instance, a ₹15 lakh policy for a 60-year-old in Delhi that previously cost ₹58,018 now only costs ₹49,168 after the tax removal.

This reduction of nearly ₹9,000 makes comprehensive healthcare much more viable for older policyholders. It specifically targets those paying high retail premiums for personal or family floater health insurance.

Can I get a GST refund for policies bought before September 2025?

The 0% GST benefit applies only to premium payments made on or after September 22, 2025. If you purchased or renewed your policy before this official cut-off date, you would have already paid the then-applicable 18% tax, which is not refundable.

The GST Council has clarified that the date of premium payment is the determining factor, regardless of when the policy coverage period actually begins. Consequently, policyholders with renewals falling after the effective date are the primary beneficiaries of the new zero-tax regulation for their next payment cycle.

How can I claim section 80D tax benefits with 0% GST?

Even with the removal of GST, you can still claim tax deductions on the full premium paid under Section 80D (old regime) of the Income Tax Act. The deduction limit remains at ₹25,000 for individuals and families, and ₹50,000 for senior citizens.

Since the GST component was previously part of the total deductible amount, your actual deduction might be slightly lower now because your total out-of-pocket spending has decreased. However, the core benefit of reducing your taxable income remains unchanged.

Will health insurance base premiums be revised after the GST removal?

There is a strong possibility that base premiums might see a slight revision due to the loss of the input tax credit (ITC) for insurance companies. When a service like health insurance becomes GST-exempt at 0%, the insurer can no longer claim tax credits on its own operational business expenses.

To manage these increased costs, some major insurers have already begun implementing premium revisions. While the removal of the 18% tax still results in a net saving for you, these gradual adjustments in base rates are expected as the industry aligns with the new GST 2.0 regulatory environment.

Is GST removed on top-up and super top-up health plans?

Yes, the 0% GST rate officially applies to all retail top-up and super top-up health insurance plans effective from September 2025. These plans are treated as individual health insurance products under the new GST 2.0 framework, allowing you to increase your coverage without the 18% tax burden.

This change encourages policyholders to secure higher protection against medical inflation without worrying about the high tax markup that previously existed.

Does the GST exemption apply to health insurance renewals?

The GST exemption applies equally to both new purchases and policy renewals, provided the payment is made on or after September 22, 2025. If your policy is up for renewal in 2026, your insurer must automatically calculate your premium at the 0% tax rate.

You should verify your renewal notice to ensure that the previously standard 18% GST has been removed from the total amount due. This automatic transition ensures that existing policyholders benefit from the new tax regime without needing to submit any additional applications or paperwork to the insurance company or tax authorities.

How does the loss of input tax credit affect health insurance prices?

While the GST on premiums is now 0%, insurance companies can no longer claim input tax credit (ITC) on their business expenses, like office rent or software services. To offset this loss, some major insurers are revising their base premiums in 2026.

Despite these minor base rate revisions, you still see a significant net saving on your total bill compared to the old 18% tax rate. It remains a massive financial win for consumers, as the overall cost of individual health insurance has dropped substantially.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.