Overview

Care Health Insurance is a standalone health insurer in India. Care Freedom is one of its products designed for customers with higher-risk medical histories. As of March 31, 2025, Care Health has a solvency ratio of 1.68x, above the IRDAI-mandated minimum of 1.5x, indicating the company has the financial strength to pay claims when it matters.

That makes Care Freedom worth considering if you have critical conditions and have been rejected elsewhere. But an accessible plan does not automatically mean a great plan.

So the real question is whether Care Freedom actually delivers the coverage high-risk individuals expect.

This article covers its features, waiting periods, copayments, sub-limits, premiums, insurer performance, and whether it is worth choosing.

What Is Care Freedom Health Insurance?

Here's the basic structure of the plan:

You can refer to the Care Freedom brochure for more details.

What Does Care Freedom Cover?

Inpatient Hospitalization

Covered up to the SI for treatments requiring 24+ hours of hospitalization.

Consumables

Coverage for consumables kicks in only after the third day of hospitalization and applies for up to 7 days per hospitalization. The daily limit depends on your SI. For a ₹3 lakh cover, the cap is ₹750 per day. Whereas, for ₹5 lakh, ₹7 lakh, and ₹10 lakh cover, it is ₹1,000 per day.

Restoration Benefit

If you exhaust your cover during a hospitalization, the full sum insured is restored for a different illness once in the same policy year.

Pre- and Post-Hospitalization Expenses

The expenses are covered up to limits based on your sum insured. For a ₹3 lakh SI, the coverage is up to 7.5% of the payable hospitalization expenses. For ₹5 lakh, ₹7 lakh, and ₹10 lakh, the cap is up to 10% of the payable hospitalization expenses.

Daycare Procedures, Modern and AYUSH Treatments

The plan covers treatments that take less than 24 hours, enabled by technical and medical advancements. Both daycare and modern treatments are covered up to SI for select treatments. Alternative treatments like Ayurveda, Siddha, and modern treatments are also covered up to the SI.

Annual Health Checkup

A free annual checkup is included every year. It is available on a cashless basis from Care's partner facilities. The list of tests is predefined.

Ambulance Coverage

Ambulance expenses are covered up to ₹1,000 only per hospitalization.

Unique Features of the Care Freedom Plan

Domiciliary Coverage

Accessible for Individuals with Chronic Conditions

Flexible Discounts

OPD Add-on Available

Waiting Periods, Copayments, and Sub-Limits

This is where you need to pay close attention. Care Freedom comes with several conditions that can significantly reduce what you actually receive at claim time.

Waiting Periods

- Initial Waiting Period: 30 days (except for accidents)

- Specific Illness Waiting Period: 2 years (Cancer falls under this list)

- Pre-Existing Disease (PED) Waiting Period: 2 years

Key Insight: There is a chance of permanent exclusions under the Care Freedom plan. This means that if someone, let’s say, has a history of diabetic foot, the company may decide to permanently exclude any complications arising from diabetes and offer coverage for the remaining conditions.

Copayment

This is a major limitation of the plan. Copayment here is mandatory, not optional.

- Less than or equal to 70 years: You pay 20% of every hospital bill

- 71 years and above: You pay 30% of every hospital bill

That means on a ₹2 lakh hospital bill, you're paying ₹40,000 out of pocket if you're under 70. That's significant, and it doesn't go away as you age.

Room Rent Restrictions

- SI of ₹3 lakh: Twin-sharing room, up to 1% of the SI per day (ICU up to 2% of the SI per day)

- SI of ₹5 lakh: You're limited to a twin-sharing room

- SI of ₹7 lakh and above: You get a single private room

If you pick a room that exceeds your category, the insurer pays only proportionally, which means your bill could increase considerably.

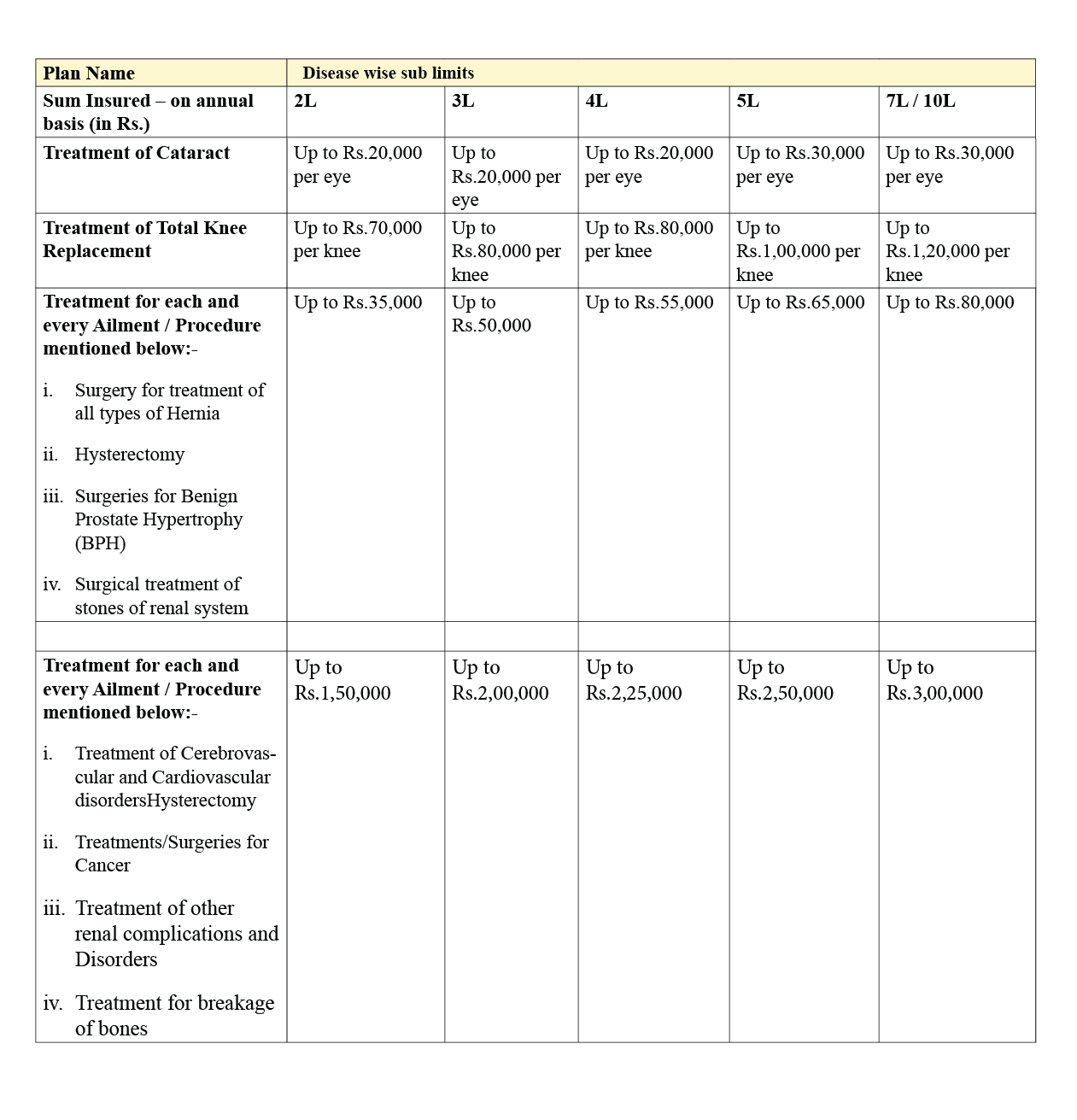

Disease Wise Sub-Limits

This is perhaps the biggest red flag. Care Freedom puts specific caps on high-cost treatments. Have a look at the infographic below to check the disease-wise sub-limits:

Before we get into the premiums, let’s have a look at the insurer's performance.

Care Health Insurance: Performance Metrics

Source: IRDAI annual reports and Care Health’s public disclosures.

Key Insights

- CSR: Care Health’s CSR indicates long-term reliability. When you file a claim, the odds of it being paid out are in your favor.

- ICR: The ICR falls within the healthy 50-80% range. This means the insurer is settling claims without overextending financially.

- GWP: The consistent growth in Care's business volume is a healthy sign for long-term stability.

- Complaint Volume: The number of complaints is high. But Care is a standalone health insurer, so all complaints come from the complex health segment alone, unlike general insurers, where complaints are spread across multiple lines.

- Network Hospitals: Coverage spans both metro cities and smaller towns, so finding a network hospital should not be a problem for most policyholders.

For complete details about the insurer, refer to our detailed Care Health Insurance review.

Premium for Care Freedom: What to Expect

Note: A stands for adult. The premiums are calculated for individuals residing in Delhi (pin code: 110010). These numbers may vary based on age, medical history, location, and selected add-ons.

Should You Buy Care Freedom?

Consider Care Freedom if You:

- Have applied to standard insurers and been rejected because of your health history.

- Don't have access to a group plan from your employer or bank.

- Checked Ayushman Bharat and Pradhan Mantri Jan Arogya Yojana (PM-JAY) eligibility, but don't qualify.

Skip Care Freedom if You:

- Are healthy and can qualify for a standard comprehensive plan.

- Want a plan without mandatory copayments and sub-limits.

- Want your sum insured to grow over claim-free years.

- Have a corporate/group policy.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 22,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or chat with our advisors on WhatsApp.

Conclusion

Before settling on the Care Freedom plan, work through this checklist first. At Ditto, we strongly recommend that having some coverage is better than having no coverage at all.

- Start with standard comprehensive plans like HDFC ERGO Optima Secure/Secure+, Care Supreme, and Aditya Birla Activ One Max. Some may still accept you with a pre-existing condition, depending on underwriting.

- Next, check if your employer offers a group health plan. These usually cover pre-existing diseases from day one with no copayment (depending on the plan). Also, check if your bank offers a group plan for account holders.

- Finally, see if you qualify for Ayushman Bharat PM-JAY, which offers up to ₹5 lakh cashless coverage per family with no copayment and no PED exclusions.

Only if all of the above have been exhausted should you consider Care Freedom. However, the mandatory copay, room rent restrictions, sub-limits, and no bonus are not minor trade-offs. If you have genuinely run out of options, Care Freedom gives you a path to coverage.

Frequently Asked Questions

Last updated on: