![Aditya Birla Health Insurance Premium Chart [2026]](https://stat.joinditto.in/images/2026/07/Aditya-Birla-Health-Insurance-Premium-Chart-@2x.webp)

Overview

Aditya Birla Capital Health Insurance, officially Aditya Birla Health Insurance, is a joint venture between Aditya Birla Capital Ltd. and Momentum Group Ltd. of South Africa. The insurer offers individual, family floater, senior citizen, and super top-up health insurance plans with wellness-focused features such as HealthReturns and Chronic Care. When comparing plans, people often get stuck focusing on premiums. The Aditya Birla Health Insurance premium chart helps provide a starting idea of premiums.

In this guide, we'll explain how to read the premium chart, compare popular plans, understand the factors that affect your premium, and calculate your premium online.

What Is the Aditya Birla Health Insurance Premium Chart?

The Aditya Birla Health Insurance premium chart is a pricing table that provides indicative premiums for different health insurance plans based on various customer and policy details. It helps you compare plans and estimate coverage costs before purchasing or renewing a policy.

A premium chart includes:

- Age of the Insured: Premiums generally increase with age.

- Sum Insured: Higher coverage amounts typically lead to higher premiums.

- Plan Type: Individual and family floaters have different pricing structures.

- Plan Variant: Plans such as Activ One, Activ Health, Activ Fit, and Activ Care differ in features and benefits, which affects premiums.

- Number of Members Covered: For family floater plans, the premium depends on the number and age of the members covered.

- City or Zone: Premiums may vary across locations because healthcare costs differ from one city to another.

The health insurance premium shown in the chart is usually a base or indicative number. Your final premium may vary depending on:

- Medical history and Pre-Existing Diseases (PEDs).

- Selected optional covers and add-on benefits.

- Policy tenure.

- The insurer's underwriting assessment.

- Applicable discounts on eligible multi-year policies.

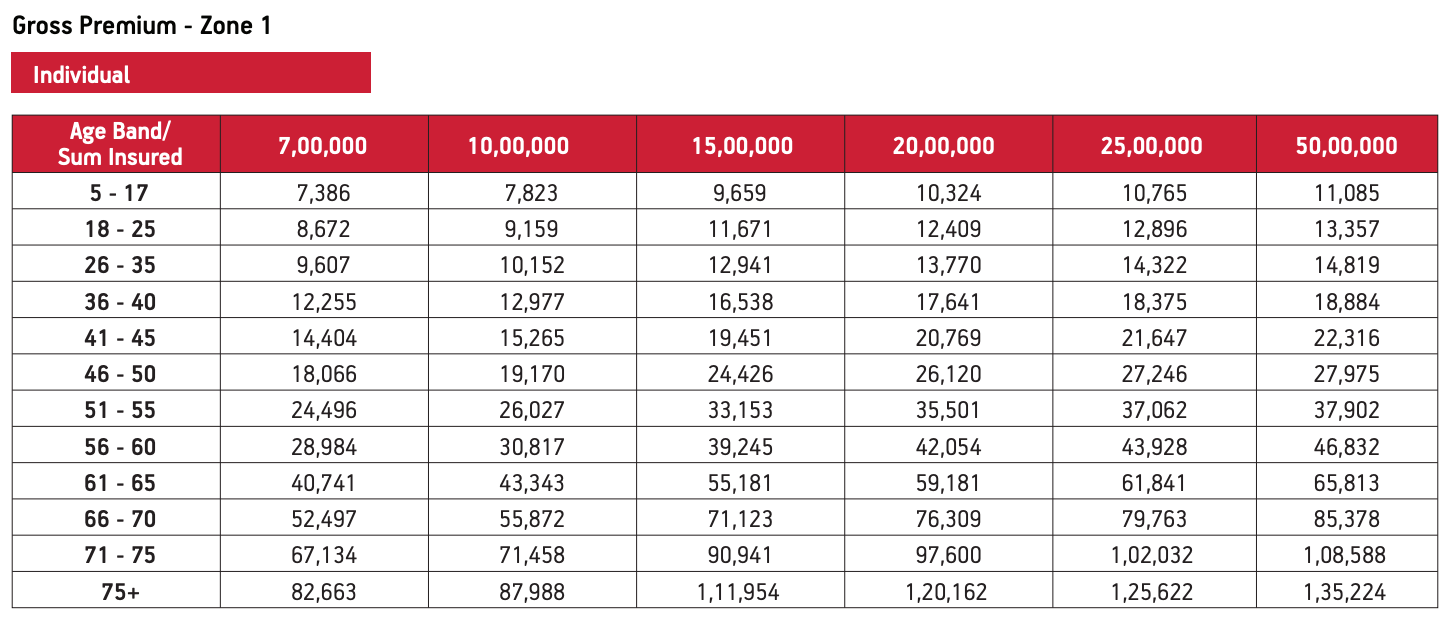

Sample Premiums by Age and Sum Insured

The table below is based on the Activ One MAX rate chart for an individual policy in Zone 1. It is intended to illustrate how premiums vary across age bands and sum-insured options.

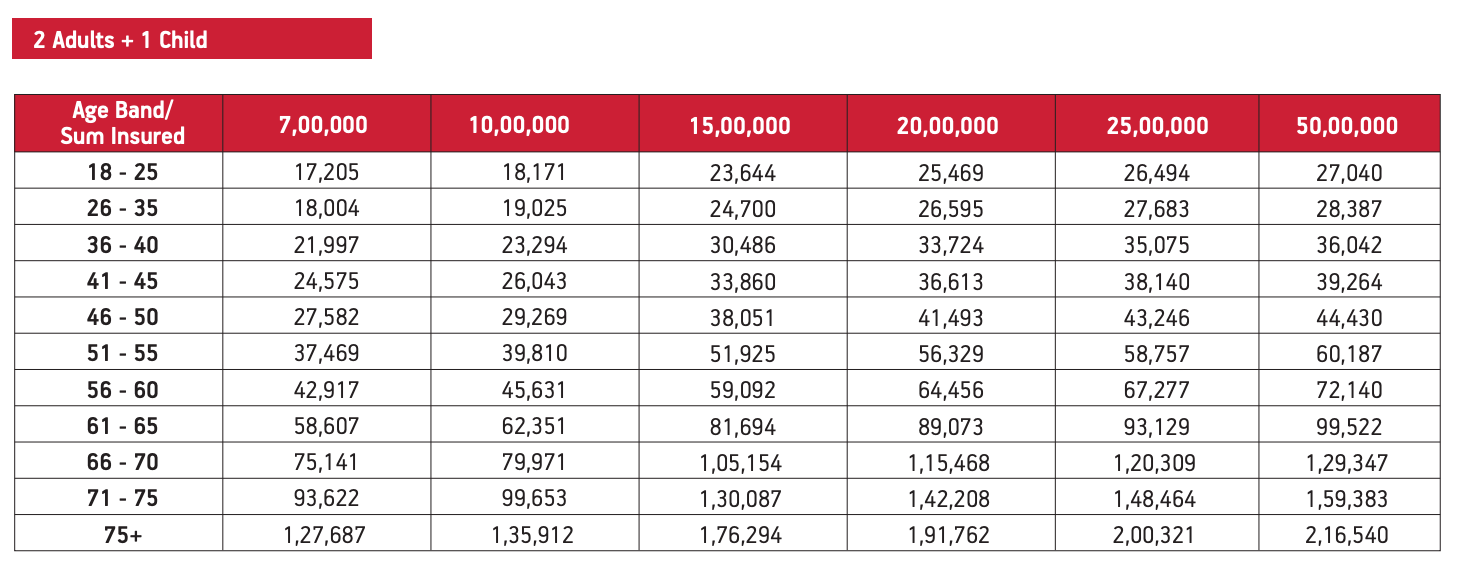

The chart below compares indicative annual premiums for a family floater policy (2 adults + 1 child) across different age bands and sum insured options.

Note: These figures are indicative and rounded for illustration. Your actual premium may vary based on factors such as your city, age, gender, medical history, selected policy variant, optional covers, and underwriting.

If you're looking for an Aditya Birla Health Insurance Premium Chart PDF download, refer to the product-specific brochure, which includes indicative premium tables, eligibility criteria, and policy benefits.

Premium Chart for Activ One vs. Activ Health Plans

The table below shows who each plan is best suited for and where you can access its premium chart for detailed pricing.

Factors That Affect Your Aditya Birla Health Insurance Premium

- Age: For individual policies, the premium is based on the insured member's age at the time of purchase. For family floater plans, the age of the eldest insured member is generally taken into account. As age increases, the likelihood of hospitalization and medical treatment rises, leading to higher premiums.

- Sum Insured: The sum insured is the maximum amount the insurer will pay for covered medical expenses during a policy year. Choosing a higher sum insured generally increases the premium, although the increase is not always proportional.

- Policy Structure: Aditya Birla Health Insurance offers individual, family floater, senior citizen, and super top-up plans. Family floater plans cover multiple members under a single sum insured, while individual plans provide separate coverage for each insured member, which may affect the premium.

- City or Zone: Premiums may vary by city or zone because healthcare and hospitalization costs differ across locations.

- Plan Variant: Different plan variants, such as Activ One, Activ Health, Activ Fit, and Activ Care, offer different levels of coverage and benefits, which can influence the premium.

- Medical History and Underwriting: If you have pre-existing diseases (PEDs), lifestyle-related conditions, or a significant medical history, the insurer may apply premium loading, waiting periods, exclusions, or other underwriting conditions based on the risk involved.

- Optional Covers: Adding optional covers such as Outpatient Department (OPD) cover, maternity benefits, Critical Illness (CI) cover, Personal Accident (PA) cover, or waiting period reduction options increases the premium while enhancing the scope of coverage.

- Policy Tenure: Choosing a multi-year policy may qualify you for long-term discounts, depending on the plan's terms and conditions.

- HealthReturns: Eligible policyholders can earn wellness rewards through Aditya Birla's HealthReturns program, which may help reduce renewal costs, subject to the policy terms and conditions.

Note: From 22 September 2025, GST on individual health insurance policies, including family floater and senior citizen policies, is nil. This does not automatically mean every health-related insurance arrangement or group policy has the same GST treatment.

How to Calculate Your Premium Online?

- Visit Aditya Birla Health Insurance’s official website and choose the health insurance plan you want to explore.

- Enter your basic details, including your age, city, family members, and preferred sum insured.

- Select the plan variant and add any optional covers or riders, if needed.

- Declare your medical history accurately, including any pre-existing conditions, such as diabetes, hypertension, or asthma, as well as any previous surgeries.

- Review the estimated premium, waiting periods, exclusions, and policy terms before purchasing. You can also download the relevant product brochure, where available, to compare plan features and indicative pricing before making a decision.

Tip: Always declare your medical history truthfully. Incorrect or incomplete disclosures can lead to claim rejection, policy cancellation, or disputes during hospitalization.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 25,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or chat with our advisors on WhatsApp.

Ditto's Take

The Aditya Birla Health Insurance premium chart is a useful starting point for estimating policy costs and comparing plans. However, your decision should not be based on premiums alone. Review the Aditya Birla Health Insurance claim settlement ratio, hospital network, waiting periods, exclusions, and overall coverage before purchasing a policy.

Aditya Birla Health Insurance has maintained a strong average claim settlement ratio of 96.25% during FY 2024–26. However, when comparing insurers, it's equally important to consider factors such as complaint volume, hospital network, waiting periods, policy exclusions, and overall coverage instead of relying on premium alone. Compare these metrics alongside the plan's benefits before making your final decision.

The right policy ultimately depends on your age, health profile, budget, and coverage requirements. For a broader comparison, refer to our guide on the best health insurance companies in India before making your final choice.

Frequently Asked Questions

Last updated on: