A ₹1 crore health insurance provides high-value coverage to manage expensive medical treatments, especially for critical illnesses and treatments in private hospitals. These plans have become essential in India due to rising medical inflation (12.9% annually) and the high cost of lifestyle-related critical illnesses.

For anyone looking for a ₹1 crore cover, Ditto’s top recommendation is HDFC Ergo Optima Secure. A 25-year-old individual in Delhi will pay ₹17,820 for a ₹1 crore cover (with unlimited restoration) under this plan.

This guide discusses whether ₹1 crore health insurance is worth it and whether there are better alternatives.

Medical costs in India are rising, and serious treatments can quickly run into several lakhs. But does that mean ₹1 crore health insurance is the best solution for everyone? Not necessarily.

That said, a ₹1 crore health insurance policy is less about routine claims and more about peace of mind during worst-case scenarios like cancer treatment, organ transplants, or prolonged intensive care unit (ICU) stays. There is very little chance that the entire amount will be exhausted during your policy tenure.

To understand this better, let’s discuss when a ₹1 crore cover makes sense and when it may be unnecessary.

Is a ₹1 Crore Health Insurance Enough for You in 2026?

A ₹1 crore sum insured offers comprehensive coverage against sudden emergencies, long-term illnesses, or black swan events like COVID-19 (an unpredictable occurrence that has a massive impact) without creating a significant financial burden.

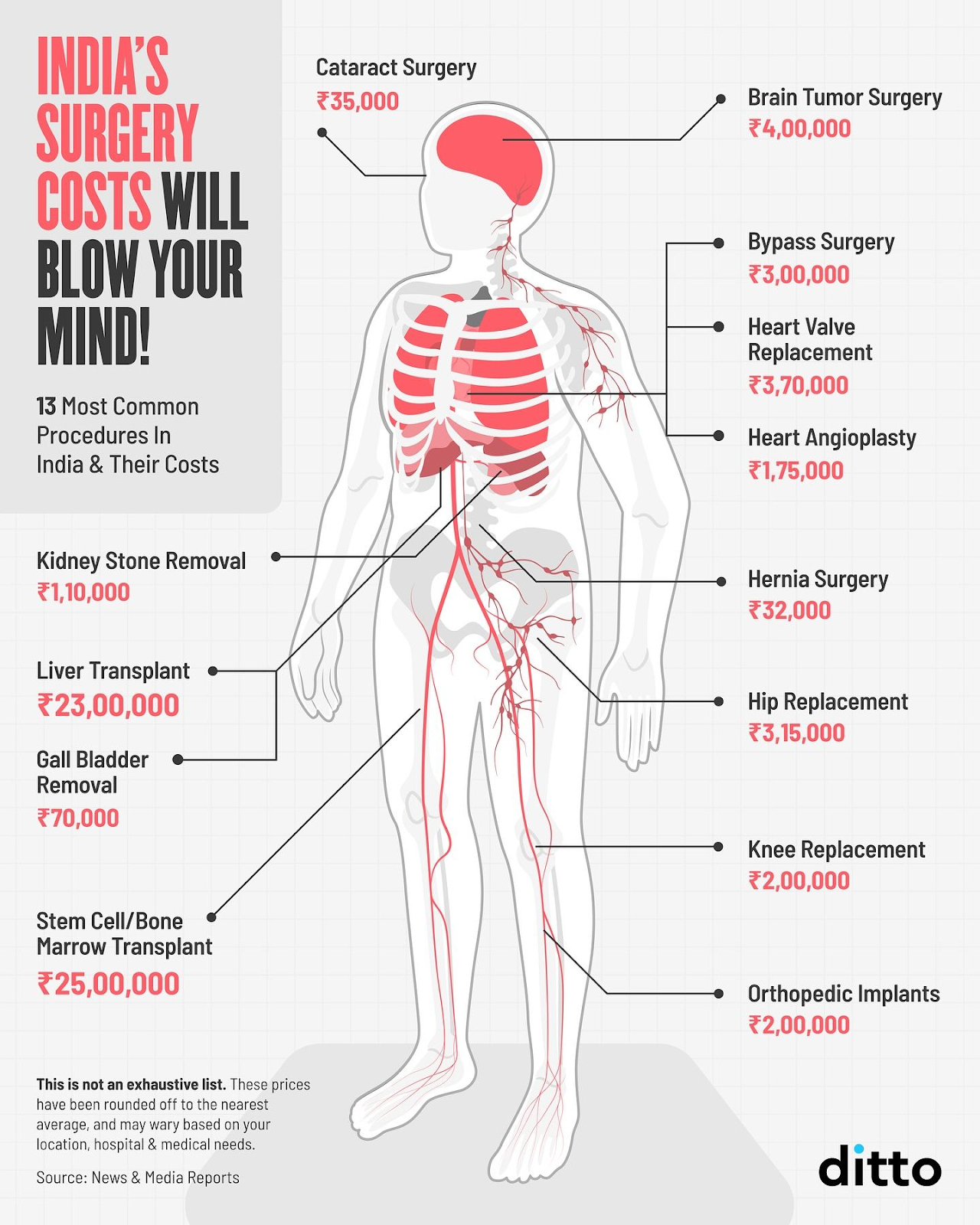

The infographic below show current surgical costs in India to help you assess whether ₹1 crore in health insurance actually makes sense.

CTA

What is Included in a ₹1 Crore Health Insurance Policy?

Medically necessary hospitalization for critical illnesses like cancer, heart disease, diabetes-related complications, and other conditions.

Bonus on top of the ₹1 crore base sum insured.

Restoration benefits are available to recharge the sum insured if it is exhausted during multiple hospitalizations in the same year.

Daycare procedures include hernia repair, cataract surgery, and knee replacement surgeries.

2x coverage from day 1, inbuilt consumables coverage, a bonus of 50% PA up to 100% given irrespective of claims, 100% restoration available on partial exhaustion once (unlimited with add-on).

Inbuilt bonus of 50% PA up to 100% (up to 500% or unlimited accumulation with add-ons), given irrespective of claims, pre and post-hospitalization: 60-180 days, unlimited restoration.

Built-in unlimited restoration, a bonus of 100% PA up to 500% given irrespective of claims, and consumables are covered by default. Wellness-linked premium discounts of up to 100%.

60-180 days pre- and post-hospitalization, Booster+ (Carry forward unutilized cover as per entry age, up to 5x as per Platinum+ variant), ReAssure Forever offers restoration (after first claim).

50% bonus up to 100% every year, regardless of claims, unlimited restoration by default up to 200%, 60-180 days pre- and post-hospitalization.

Here, CSR stands for claim settlement ratio, ICR denotes incurred claim ratio, and PA denotes per annum.

Premiums For ₹1 Crore Sum Insured

Profiles

HDFC Ergo Optima Secure

Care Supreme

Aditya Birla Activ One Max

Individual Plan, Age 25

₹17,820

₹24,999

₹16,883

Family Floater (2A), Ages (31, 32)

₹27,494

₹38,486

₹27,511

Family Floater (2A 1C), Ages (35, 34, 5)

₹34,761

₹48,724

₹36,376

Family Floater (2A), Ages (62, 63)

₹1,63,280

₹1,45,617

₹1,18,324

Note: A stands for adults and C denotes children. The above comparison is a sample of ₹1 crore health insurance premiums for a tier-1 city (New Delhi, 110010). The profiles considered are healthy and have no pre-existing diseases.

Common Mistakes To Avoid While Choosing a ₹1 Crore Sum Insured

01

Ignoring the Insurer Metrics

A high sum insured is not useful if the insurer does not settle claims easily. A CSR above 90% is generally a good sign, as is an ICR between 50% and 80%. Make sure that the volume of complaints per 10,000 claims is low.

02

Not Reviewing Your Cover With Changes in Circumstances

The adequacy of your sum insured should be reassessed whenever your family composition changes, when a parent is added to your coverage responsibility, or at a minimum every 3 to 5 years. A ₹1 crore cover for a 30-year-old individual without dependents is a different decision than a ₹1 crore cover for the same person at 40 with a family and aging parents.

03

Choosing Plans with Sub-Limits

A ₹1 crore sum insured will be meaningless if the plan has disease-wise sub-limits, copay clauses, or room rent restrictions, as actual claim payouts will always be capped.

04

Misunderstanding Restoration Benefits

Restoration usually applies only to the base sum insured and not to any accumulated bonus. It also comes into effect only after the base cover is used, either partially or fully.

05

Assuming a Family Floater Is Always Better

In a family floater plan, all members share the same sum insured. For families with older members or existing health conditions, individual policies can be a more suitable option.

06

Not Disclosing Pre-existing Conditions at the Time of Purchase

If you have diabetes, hypertension, thyroid conditions, or any other pre-existing disease, disclose it honestly at the time of application. Withholding this information to avoid a higher premium or a waiting period is not a viable strategy. It may lead to claim rejection or policy termination at precisely the moment you need the coverage most.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

100% Free Consultation

Dedicated Claim Support Team

Backed by Zerodha

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

No-Spam & No Salesmen

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or chat on WhatsApp with us now!

Ditto’s Take on ₹1 Crore Health Insurance

A ₹1 crore health insurance policy is ideal if you:

Live in a metro city like Mumbai, Delhi, or Bengaluru, where hospital costs are significantly higher.

Want to cover your family, especially your elderly parents.

Have a pre-existing disease like hypertension, diabetes, or a heart ailment.

Want long-term peace of mind and stable protection against medical emergencies.

If you want a ₹1 crore cover or can comfortably afford one, that’s great. However, based on current hospitalization costs, medical inflation, and practical claim scenarios, we usually recommend a base cover of around ₹15 lakh to ₹25 lakh, since bonuses and restoration benefits can push your usable coverage much higher over time.

The interesting part is that premiums do not rise in proportion to the sum insured. To set context, the premium for a ₹1 crore sum insured is not 4x that of a ₹25 lakh cover. So, the increase is hardly 20-40%.

If you’ve just begun with your search and need more guidance on coverage, check our guide on how to choose health insurance.

Frequently Asked Questions

Is ₹1 crore health insurance worth it in India in 2025–26?

A ₹1 crore health insurance plan is worth it if you live in a metro city, have a family history of critical illness, or want long-term protection against rising medical costs. India's medical inflation runs at roughly 12.9% annually, meaning a treatment costing ₹10 lakh today could cost ₹20 lakh or more in a decade. For most healthy people under 40, a ₹15–25 lakh base plan with restoration benefits can be equally effective and far more affordable. The right choice depends on your age, city, family size, and existing health conditions.

How do I estimate my cost with a ₹1 crore health insurance premium calculator?

You can use a ₹1 crore health insurance premium calculator to estimate the premium you need to pay for your chosen plan. Enter your age, city, number of members, and any pre-existing conditions to get an instant quote. Key factors that affect your premium include age (the single biggest driver), medical history, plan type (individual vs. family floater), and add-ons selected. For instance, a 35-year-old couple with one child in Delhi can expect to pay around ₹34,000–₹49,000 per year for ₹1 crore coverage, depending on the insurer.

What does ₹1 crore health insurance actually cover?

A ₹1 crore health insurance policy covers inpatient hospitalization, ICU charges, daycare procedures such as cataract surgery and hernia repair, pre- and post-hospitalization expenses (usually 60 days before and up to 180 days after discharge), domiciliary treatment, AYUSH treatments, and consumables such as gloves and PPE kits. Most plans also include restoration benefits that recharge the sum insured if exhausted. Exact inclusions vary by insurer, so it's important to read the policy document for sub-limits, waiting periods, and exclusions before purchasing.

Which is the best ₹1 crore health insurance plan in India right now?

HDFC Ergo Optima Secureis widely regarded as one of the best ₹1 crore health insurance plans in India, offering 2x coverage from day one, inbuilt consumables cover, and a 50–100% bonus, regardless of claims. Other strong contenders include Aditya Birla Activ One Max, which offers unlimited restoration and up to 500% cumulative bonus, and Care Supreme, known for flexible bonus structures.When choosing, compare the claim settlement ratio (look for above 90%), the incurred claim ratio, the network hospital count, and restoration terms.

Is a family floater better than individual plans for a ₹1 crore cover?

A family floater plan lets all members share one ₹1 crore sum insured, which is more cost-effective for young, healthy families. For example, a floater for a couple aged 31 and 32 under HDFC Ergo Optima Secure costs around ₹27,511 per year. However, if your family includes older members or individuals with pre-existing conditions, individual policies are often a better fit. A single major claim can exhaust the entire shared pool, leaving other members unprotected. Families with parents aged 55 and above are generally better served by separate individual policies.

Can I get ₹1 crore health insurance with a pre-existing disease?

Yes, you can get ₹1 crore health insurance with a pre-existing disease, but the insurer will typically impose a waiting period before covering those conditions. Three years is the maximum permitted timeline under current IRDAI regulations. Your premium may also be higher based on the nature and severity of the illness. Additionally, the insurer may apply loading charges, cover restrictions, exclusions, or in severe cases, reject the application altogether. Conditions like diabetes, hypertension, and heart disease are among the most common pre-existing ailments that affect underwriting. It's essential to fully disclose your medical history at the time of application because withholding this information can result in claim rejection at a critical time.

What is the difference between a super top-up and a ₹1 crore base health insurance plan?

A base ₹1 crore health insurance plan covers all hospitalization costs up to ₹1 crore per policy year from the first rupee of a claim. A super top-up plan, on the other hand, only kicks in once a deductible threshold is crossed, typically ₹3–10 lakh. Pairing a ₹5–10 lakh base plan with a super top-up to achieve ₹1 crore effective coverage, ideally from the same insurer) is cheaper than a standalone ₹1 crore base plan. This combination is ideal for budget-conscious buyers who want high coverage without paying steep premiums upfront.

Does ₹1 crore health insurance cover cancer treatment in India?

Yes, ₹1 crore health insurance typically covers cancer treatment, including chemotherapy, radiation therapy, surgery, and associated hospitalization costs, provided the diagnosis is made after the policy purchase. Given that advanced cancer treatment in India can cost ₹20–50 lakh or more, depending on the stage and type, a ₹1 crore sum insured offers meaningful financial protection. Some plans also include organ donor expenses and post-treatment recovery costs. Always verify whether the policy covers targeted therapy or immunotherapy, as these newer treatments can be expensive and are sometimes excluded.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.