Overview

Accidents are unpredictable, and even a minor mishap can lead to medical expenses, temporary loss of income, or long-term financial stress for your family. Saral Suraksha Bima is a simple, IRDAI-standardized personal accident policy that offers financial protection against these incidents.

In this guide, we’ll walk you through what the policy covers, its eligibility criteria, key features, and how to buy it.

What is Saral Suraksha Bima?

Saral Suraksha Bima is a standardized personal accident insurance plan introduced by the Insurance Regulatory and Development Authority of India (IRDAI) to simplify and standardize accident coverage across all insurers. The idea is simple: no matter which insurer you choose, the benefits, features, and terms remain the same. Only the premiums may vary.

This plan provides financial protection in case of accidental injuries or death, ensuring that families are not left burdened during difficult times.

Did You Know?

Coverage, Benefits, and Key Features

Mandatory Base Covers

- Accidental Death: Pays 100% of the sum insured if the policyholder dies within 12 months of an accident.

- Permanent Total Disablement (PTD): Provides a full payout for severe, life-altering disabilities such as loss of both eyes, both hands, both feet, or a combination of one eye and one limb. It also covers permanent inability to work.

- Permanent Partial Disablement (PPD): Pays a proportionate percentage of the sum insured depending on the body part affected. Examples include a 50% payout for loss of a hand, foot, or eye.

Additional Benefits and Key Features

- Cumulative Bonus: For each claim-free year, the sum insured increases by 5%, up to a maximum of 50%. In the event of a claim, the accumulated cumulative bonus is reduced by 5% of the base sum insured.

- Optional Add-ons: You can enhance your protection with optional covers that cater to specific needs:

- Temporary Total Disablement (TTD): Provides a weekly income of 0.2% of the sum insured for up to 100 weeks if you are temporarily unable to work due to an accident. The benefit applies only if the disability continues for more than four consecutive weeks, but once eligible, it is paid from the date of the accident, not just from the fifth week onward.

- Accidental Hospitalization Expenses: Reimburses up to 10% of the sum insured, covering room rent, ICU charges, doctor fees, surgery, medicines, prosthetics, Ayurveda, Yoga & Naturopathy, Unani, Siddha, and Homeopathy (AYUSH) treatments, daycare procedures, dental care, plastic surgery, and ambulance charges up to ₹2,000 per hospitalization.

- Education Grant: Offers a one-time payment of 10% of the base sum insured per dependent child, up to 25 years of age, if the policyholder suffers accidental death or Permanent Total Disablement (PTD). This ensures your child’s education is not disrupted in challenging times.

Premium, Eligibility, and How to Buy

Premiums (Illustrative)

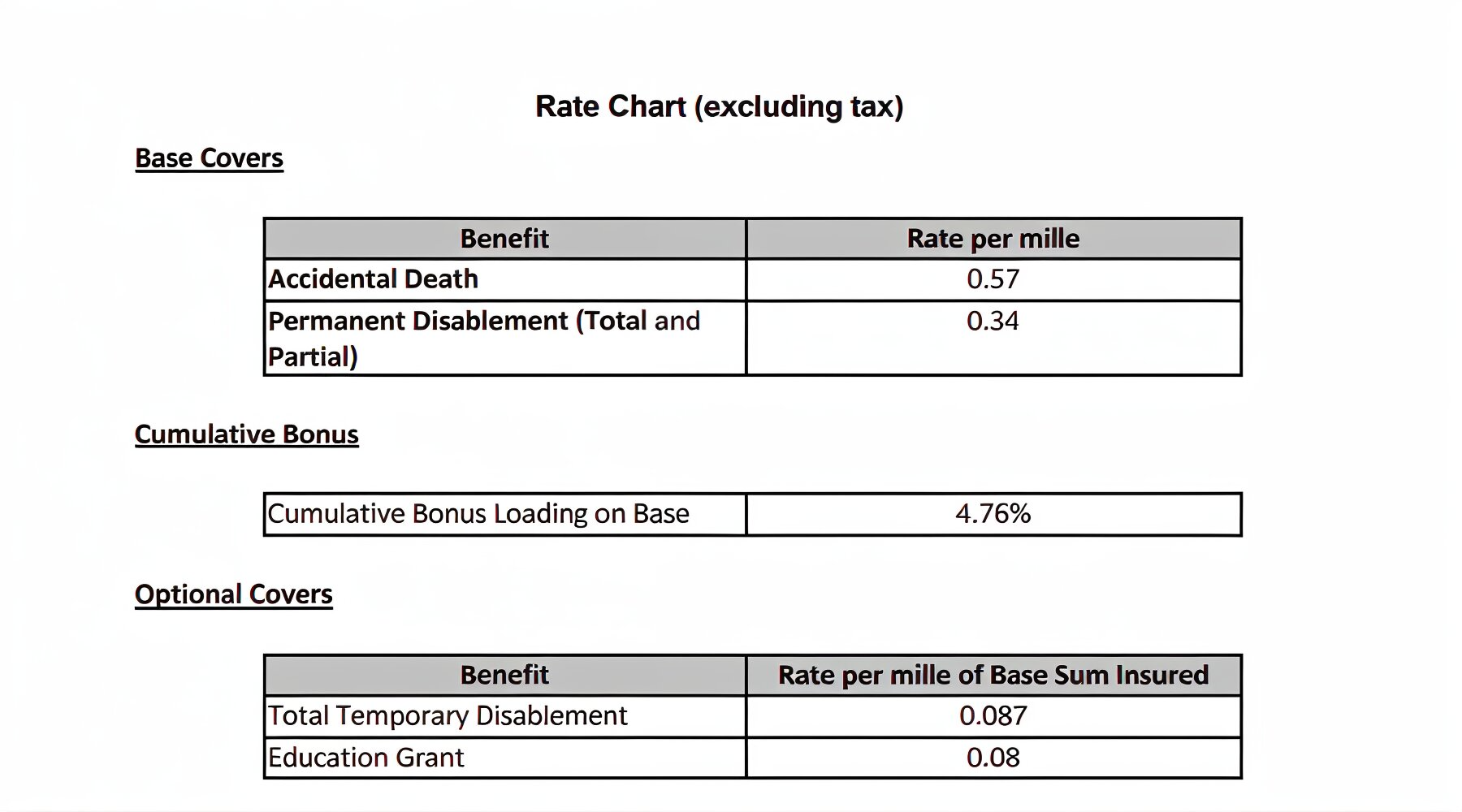

Here is the rate chart for HDFC Ergo’s Saral Suraksha Bima.

"Per mille" = per ₹1,000 of sum insured. So, here’s the calculation:

Premium = (Sum Insured ÷ 1,000) × Rate

Now, let’s consider two profiles with full premium breakdowns (excluding GST):

Profile 1: Age 28, IT Professional

Base Sum Insured: ₹25,00,000 | Hospitalization Sum Insured: ₹5,00,000

Profile 2: Age 40, Small Business Owner

Base Sum Insured: ₹50,00,000 | Hospitalization Sum Insured: ₹8,00,000

Note: The loading added in the calculation covers HDFC Ergo's cost of providing the cumulative bonus benefit. This increases your sum insured each year you remain claim-free at no additional charge.

Eligibility Criteria for Saral Suraksha Bima

- Age of Policyholder: Individuals aged 18 to 70 years can buy Saral Suraksha Bima. Some insurers may extend the upper age limit if required.

- Dependent Children: Dependent children aged 3 months to 25 years can be covered, provided they are full-time students.

- Family Members Covered: The policy can cover the proposer, spouse, parents, parents-in-law, and dependent children.

- Policy Tenure: The policy is valid for 1 year and can be renewed annually for continued protection.

- Sum Insured: The sum insured ranges from ₹2.5 lakh to ₹1 crore and is available in multiples of ₹50,000.

- Premium Payment Options: Premiums can be paid annually, half-yearly, quarterly, or monthly. Some insurers may also allow electronic clearing service (ECS) or auto-debit payments.

- Grace Period: A grace period of 15 days is available for monthly premium payments, while 30 days is available for all other premium payment modes.

- Suitable For: Families looking for standard personal accident cover with protection for key family members under a single policy.

How to Buy Saral Suraksha Bima

You can buy the policy through all general and standalone health insurers in the following ways:

The buying process is straightforward:

- Submit your personal details to the insurer.

- Choose your sum insured and any optional add-ons, such as TTD, hospitalization, or an education grant.

- Make the premium payment, either digitally or offline.

- Receive your policy document immediately, either in digital or physical format.

Note: These premiums are publicly disclosed, allowing you to compare different insurers and select the plan that best meets your needs.

Key Points to Remember

Saral Suraksha Bima vs Other Accident Plans: Is It Enough?

Takeaway: Saral Suraksha Bima is a good entry-level personal accident policy if you want simple and standardized coverage. However, if your income, loans, or family responsibilities are high, you may need a more comprehensive accident plan with stronger add-ons and higher coverage.

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat with us on WhatsApp!

Conclusion

Saral Suraksha Bima remains a simple, easy-to-understand, and accessible choice that provides financial stability in the event of unforeseen accidents. But before buying a personal accident policy, you should ideally secure the basics first:

- Term insurance already covers accidental deaths.

- Health insurance also covers hospitalization expenses related to accidents.

However, these two products may not fully cover accident-related financial gaps such as loss of income, ongoing EMIs, lifestyle expenses, or the financial impact of temporary or partial permanent disability. That is where a personal accident policy like Saral Suraksha Bima comes in.

Our take? Always treat it as a secondary cover, taken after you understand what your term and health insurance plans do not cover.

Frequently Asked Questions

Last updated on: