Personal accident insurance premiums are usually calculated on a per-mille basis, meaning a fixed rate applies for every ₹1,000 of sum insured. For ₹10 lakh of accidental death cover, published rates for low-risk occupations can range from roughly ₹300 to ₹800 annually. Broader cover that includes permanent or temporary disability may cost around ₹1,250 to ₹1,750 or more.

Factors Affecting Premiums

Occupation: Desk-based professionals usually pay less than drivers, mechanics, or construction workers.

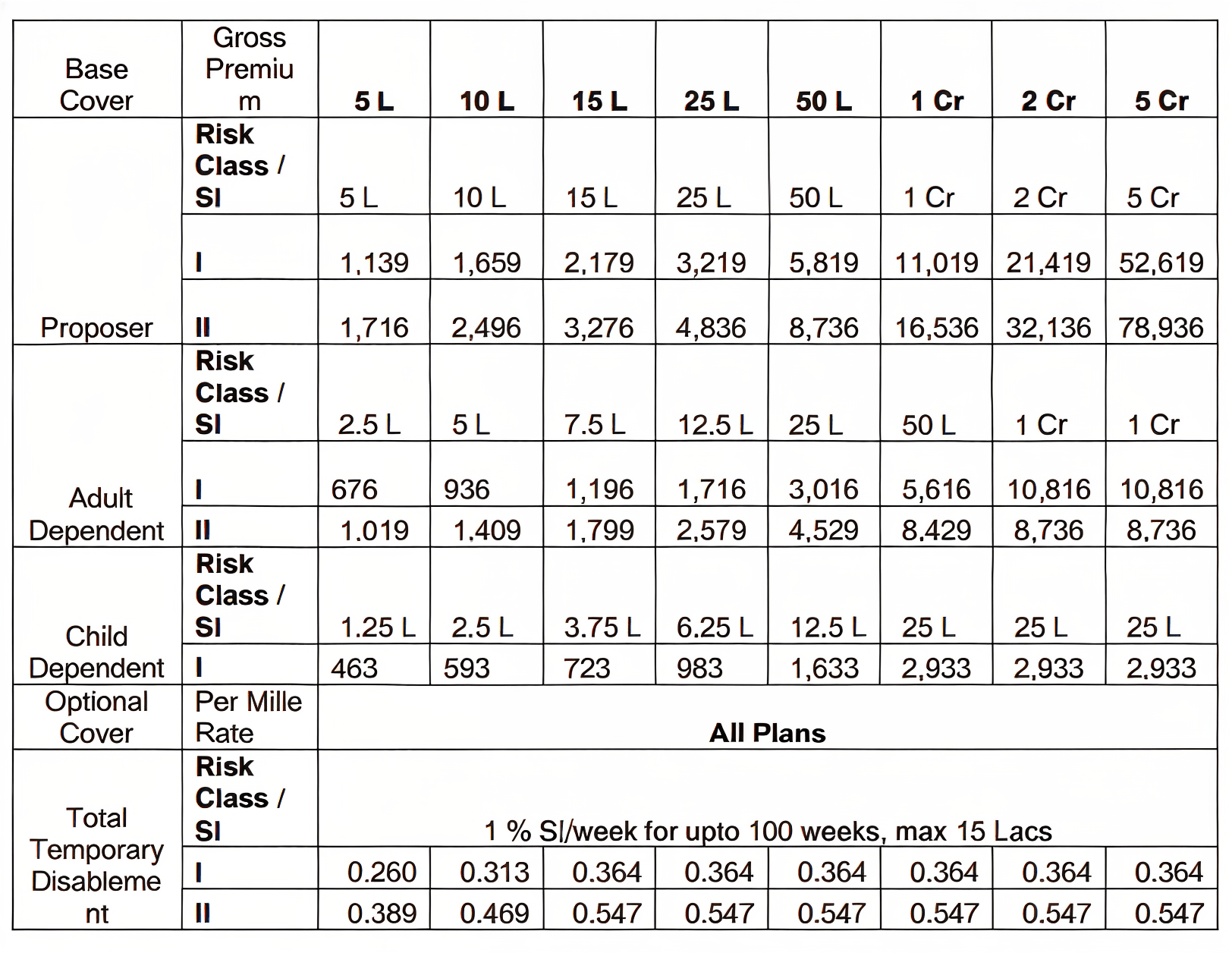

Sum Insured: HDFC ERGO’s published premium rises from ₹1,139 for ₹5 lakh to ₹11,019 for ₹1 crore under Risk Class I.

Lifestyle: Adventure sports and hazardous hobbies may attract exclusions, restrictions, or additional premiums.

For a personalized estimate, compare insurer premium charts based on your occupation, age, sum insured, and selected benefits.

In 2024, India recorded 4,87,705 road accidents, resulting in 1,77,177 deaths, roughly 484 lives lost every day, according to the Ministry of Road Transport and Highways. While there is no way to prevent an accident, personal accident insurance can provide financial support if an injury results in death, disability, or loss of income.

Despite this, many people are unsure about how much a personal accident insurance policy actually costs. This is where a personal accident insurance premium chart can make the comparison easier.

In this article, we look at sample premiums across different ages and sum insured amounts, compare individual and group pricing, explain the factors that influence premiums, and show how popular insurers, including SBI, compare on cost.

Personal accident insurance is only one part of financial protection. Book a free call or chat on WhatsApp with a Ditto advisor to choose the right health or term insurance plan.

What Is the Personal Accident Insurance Premium Chart?

A personal accident insurance premium chart shows an estimate of your annual premium against your sum insured, and sometimes your occupation category or city.

Insurers publish these in their prospectuses or rate charts, showing how premiums vary with cover amount, occupation risk, and whether pricing is for individual or group insurance.

It lets you compare per-lakh pricing across slabs, so you pick a cover amount that fits your budget.

Sample Personal Accident Insurance Premiums by Age and Sum Insured

Personal accident premiums do not increase substantially with age, unlike health insurance. Therefore, in personal accident premium charts, age is not listed as a separate pricing slab.

Age can still affect eligibility, underwriting, benefit limits, or final pricing, depending on the insurer.

Instead, the premium varies primarily based on the chosen sum insured, the insured member’s occupational risk class, and whether the covered person is the proposer, an adult dependent, or a child.

This means a 25-year-old and a 45-year-old selecting the same cover under the same risk class may see a similar listed base premium.

This chart shows the indicative annual premiums for HDFC ERGO’s Individual Personal Accident Premium variant, based on the sum insured, the insured member, and their occupational risk class.

For the proposer, a ₹5 lakh base cover costs ₹1,139 per year under Risk Class I and ₹1,716 under Risk Class II. At a ₹1 crore sum insured, the respective premiums rise to ₹11,019 and ₹16,536.

Risk Class I generally includes office-based, non-hazardous occupations, while Risk Class II includes jobs involving regular travel, site visits, supervision, or some manual work.

Adult dependents can receive up to 50% of the proposer’s sum insured, and children up to 25%.

The Total Temporary Disablement benefit is optional and is priced using a per mille rate, meaning the stated rate applies to every ₹1,000 of the selected benefit sum insured.

These figures are illustrative and exclude applicable taxes. The final premium may also change based on the applicant’s occupation, health condition, selected benefits, policy tenure, underwriting, and applicable discounts.

Popular Insurers and Personal Accident Insurance Premium Range

Plan

Key Benefits

Key Drawbacks

Sum Insured Range

Premium Chart

IRDAI-Standardized Saral Suraksha Bima

Covers accidental death, total and partial disability. Optional benefits include temporary disability, hospitalization, and an education grant. Offers up to 50% cumulative bonus.

Less customizable than flagship plans. Pricing and service vary by insurer.

Covers accidental death and disability. Higher variants may include hospitalization, ambulance services, burns, fractures, educational support, adventure sports, and home or vehicle modifications.

Benefits vary by variant. Some covers apply only to earning members, while adult and child dependents receive lower limits.

Includes death, disability, education benefit, and cumulative bonus. Optional covers include weekly income, loan or EMI protection, fractures, burns, and adventure sports.

Coverage differs by variant. Several useful benefits cost extra. Entry age is capped at 65, and temporary disability cover ends after age 70.

Covers accidental death and disability, with optional TTD, hospital cash, and ambulance cover. PTD includes education and home or vehicle adaptation benefits.

Benefits depend on the option selected. Adventure sports are excluded. TTD has a one-week deductible, and premiums vary by occupation and location.

Note: In the above table, TTD stands for Temporary Total Disability, while PTD stands for Permanent Total Disability.

CTA

Pro Tip: Start With PMSBY

Eligible bank account holders aged 18–70 can enroll in the Pradhan Mantri Suraksha Bima Yojana (PMSBY) for just ₹20 per year. It pays ₹2 lakh for accidental death or permanent total disability and ₹1 lakh for permanent partial disability.

However, the cover is modest and does not include hospitalization expenses or temporary loss of income. Treat PMSBY as a basic first layer of protection, not a replacement for broader personal accident insurance.

Factors That Affect Your Personal Accident Insurance Premium

Occupation and Job Responsibilities

Insurers classify occupations according to their exposure to accidents. Desk-based roles generally fall into lower-risk classes, while construction, driving, mining, machinery-related work, and similar occupations attract higher rates.

Selected Sum Insured

Your premium increases as you choose a higher sum insured. Some slab-based plans become cheaper per lakh at higher coverage levels, whereas percentage-based plans increase in almost the same proportion.

Benefits and Optional Covers

A policy covering accidental death and permanent disability usually costs less than one with broader benefits. Adding temporary disability income, accidental hospitalization, hospital cash, loan protection, education benefits, broken-bone cover, or air ambulance benefits increases the scope of protection and the premium payable.

Lifestyle and High-Risk Hobbies

Regular participation in activities such as mountaineering, scuba diving, racing, professional sports, or adventure sports can affect your premium. Depending on the policy, insurers may apply a loading, exclude the activity, limit related claims, or require an optional adventure-sports cover. Always disclose these activities accurately.

GST Treatment: Individual personal accident insurance policies have been exempt from GST since September 22, 2025. However, group personal accident policies, including employer-sponsored covers, continue to attract 18% GST. Older premium charts may still show GST separately, so check the chart’s publication date before calculating the final premium.

Individual vs. Group Personal Accident Insurance Premium Comparison

Individual personal accident insurance is purchased directly by the insured member, offering greater control over the sum insured, benefits, and policy tenure.

Group personal accident insurance, meanwhile, is arranged by an employer, bank, or another organization for multiple members. Since the risk is spread across a larger pool, group cover can be more affordable per person.

ICICI Lombard’s rates illustrate this difference. Under its individual Personal Protect policy, accidental death cover for Risk Category 1 is priced at 0.080% of the sum insured. This means ₹10 lakh of cover would cost approximately ₹800 a year before taxes.

Under ICICI Lombard’s group plan, accidental death cover for Risk Group I has an indicative rate of ₹0.45 per ₹1,000 of sum insured. At this rate, ₹10 lakh of cover would cost approximately ₹450 before GST.

However, these figures are not directly comparable in every case. Individual and group policies may have different benefits, limits, and underwriting conditions. Group rates are also indicative and may change based on factors such as the employer’s industry, group size, location, past claims, and selected add-ons.

Moreover, group coverage is linked to your membership or employment, whereas an individual policy remains with you as long as you continue to renew it.

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 25,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or chat on WhatsApp with us now!

Conclusion

A premium chart is a useful starting point, but it shouldn't be the only thing you check. Match your sum insured to your income and liabilities, confirm your occupation category up front to avoid claim rejections later, and read the exclusions closely, especially those around hazardous hobbies.

If your health and term cover are already solid, a personal accident policy is a low-cost way to fill the income-loss gap that neither fully covers. Compare at least two or three insurers' rate charts before you commit.

Disclaimer: Ditto assists customers only with retail term insurance and health insurance plans. Standalone personal accident insurance policies are not part of our offerings or advisory services.

Frequently Asked Questions

Is personal accident insurance worth buying separately from health insurance?

Yes, particularly for earning adults who lack adequate disability protection through their employer. Health insurance pays eligible treatment expenses, whereas personal accident insurance can pay a fixed amount for accidental death or permanent disability. It may also replace part of your income during temporary disability, but only when that benefit is included.

Does personal accident insurance attract 18% GST?

Individual personal accident policies do not currently attract GST at 18%. From September 22, 2025, the GST exemption for individual and family health insurance was extended to personal accident cover. Group personal accident policies, including employer-sponsored plans, remain taxable at 18%. Therefore, older insurer rate charts may show tax calculations that no longer apply to individual policies.

Is SBI personal accident insurance cheaper than other insurers for the same sum insured?

Not in every case. SBI General’s published chart prices ₹10 lakh death-only cover for a Category I applicant at about ₹300 to ₹400, depending on location. ICICI Lombard’s corresponding Category I rate works out to ₹800. However, this comparison changes once permanent disability, temporary disability, hospitalization, or other benefits are added.

Does a risky occupation increase personal accident insurance premiums?

Yes. Insurers treat occupation as a core pricing factor because accident exposure differs by job. Drivers, construction workers, mechanics, miners, and people operating heavy machinery generally pay more than office-based applicants and may face lower sum insured limits. Disclose your actual daily duties, since an inaccurate occupation declaration can affect claim admissibility.

Should I enroll in PMSBY before buying private personal accident insurance?

Yes, enroll if you are eligible, but do not treat it as sufficient cover. PMSBY costs ₹20 annually and pays ₹2 lakh for accidental death or permanent total disability and ₹1 lakh for permanent partial disability. Most earning adults need additional private cover because these amounts are too low to replace income or clear major liabilities.

Can self-employed individuals or freelancers buy group personal accident insurance?

A freelancer cannot buy a group policy as a group of one. However, self-employed people can receive group personal accident cover through a genuine professional association, bank, platform, lender, or other organization they already belong to. Otherwise, they must purchase an individual policy. A group cannot be formed primarily to obtain discounted insurance. Insurers generally require the group to have a genuine relationship or common purpose beyond purchasing insurance.

Does personal accident insurance cover permanent disability or only accidental death?

Most comprehensive personal accident policies cover accidental death, permanent total disability, and permanent partial disability. Temporary total disability is commonly optional rather than automatic. Some inexpensive bank-linked or bundled covers may provide only death protection or limited disability benefits. The policy schedule is decisive: the insurer pays only the benefits and limits specifically listed there.

What is the average personal accident insurance premium in India?

India has no official national average premium for personal accident insurance. Published insurer charts indicate that ₹10 lakh death-only cover for a low-risk occupation may cost roughly ₹300 to ₹800 annually. Broader packages cost more. Your actual premium depends on occupation, location, sum insured, selected disability benefits, add-ons, discounts, and current insurer rates.

Does a personal accident insurance premium increase with age?

Not necessarily. Age typically has less effect on personal accident premiums than occupation and sum insured. Several published individual rate charts do not use separate age-based slabs, so adults in the same risk category may receive similar base rates. However, insurers impose entry-age limits and may consider age during underwriting, so identical pricing cannot be guaranteed.

Can I claim health and personal accident insurance for the same accident?

Yes. Health and personal accident claims can both be filed for the same accident because they cover different losses. Health insurance reimburses admissible treatment expenses, while fixed-benefit personal accident cover pays the scheduled death or disability amount independently. However, the same medical bill cannot be reimbursed twice under two expense-based covers.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.

![Personal Accident Insurance Premium Chart [2026]](https://stat.joinditto.in/images/2026/07/Personal-Accident-Insurance-Premium-Chart@2x.webp)