For most parents, planning a child’s education means budgeting for fees, housing, and even overseas studies. What often gets overlooked is the financial impact of a medical emergency during the student years. With healthcare costs rising sharply, even a single hospitalization can disrupt long-term education plans and family savings.

Health insurance plans for students exist to prevent exactly this risk. This guide explains how student health insurance works in India and abroad, the coverage options, and the best plans to consider in 2026.

What Are Health Insurance Plans for Students?

Health insurance plans for students provide a financial safety net for medical emergencies and hospitalizations during their academic years.

In India, students access coverage as dependents on a family floater plan or through an individual retail policy.

For those studying abroad, coverage comes via university-mandated group plans or specialized international student insurance from Indian providers.

These policies also cover costs for surgeries, accidents, and illnesses.

Who Are These Plans For?

How Do Students Get Health Insurance in India?

In India, students below 25 usually get health cover in one of these ways:

- Family Floater Plans: The student is covered under a parent’s policy and shares the sum insured. This is the most cost-effective option for minor students.

- Individual Health Insurance Plans: The student has a separate policy with a dedicated sum insured. This is useful when coverage needs are higher or when nearing the exit age.

- Group Student Health Insurance: Some schools and colleges offer group policies to enrolled students. These are affordable but usually come with lower coverage and more limits.

What About Students Studying Abroad?

Students going overseas for studies usually need separate insurance. This is common for countries like the U.S., U.K., Canada, Australia, and Europe.

Coverage is typically arranged through:

- University-Sponsored Health Plans: Often mandatory and bundled with tuition fees.

- International Student Insurance Plans: Issued by Indian or global insurers. These are designed to meet visa and university requirements.

In most cases, insurance is compulsory for enrollment or visa approval. The right option depends on age, location, and university rules.

Looking for coverage for younger kids? Check out our guide on health insurance plans for children to see how early-age coverage works.

Top 5 Health Insurance Plans for Students in 2026 (Ditto’s Cut)

Note: To know the methodology behind why these plans are recommended for students, refer to Ditto’s cut and framework.

Inclusions and Exclusions in Health Insurance Plans for Students

Health insurance plans for students cover many essential healthcare needs, but they also have limitations that should be understood before purchasing a policy.

What’s Covered (Standard Inclusions)

- In-patient Hospitalization: Covers room rent, ICU charges, doctor fees, surgeries, medicines, and other hospital expenses.

- Pre-hospitalization Expenses: Pays for tests and consultations before hospital admission.

- Post-hospitalization Expenses: Covers follow-up treatment and medicines after discharge.

- Day-care Procedures: Includes treatments that don’t need 24-hour hospitalization.

- Organ Donor Expenses: Covers medical costs related to the organ donor during transplantation.

- Modern Treatments: Includes advanced procedures like robotic surgery, subject to policy terms.

- AYUSH Therapies: Covers approved Ayurveda, Yoga, Unani, Siddha, and Homeopathy treatments.

- Road Ambulance Charges: Pays for emergency ambulance transportation to the hospital.

- Domiciliary Treatment: Covers treatment taken at home when hospitalization is not possible.

Note: These inclusions are based on IRDAI guidelines and are typically part of most health insurance plans for students. However, the exact coverage, limits, and terms can vary across insurers and policies. Always read the policy wording carefully to analyze these considerations.

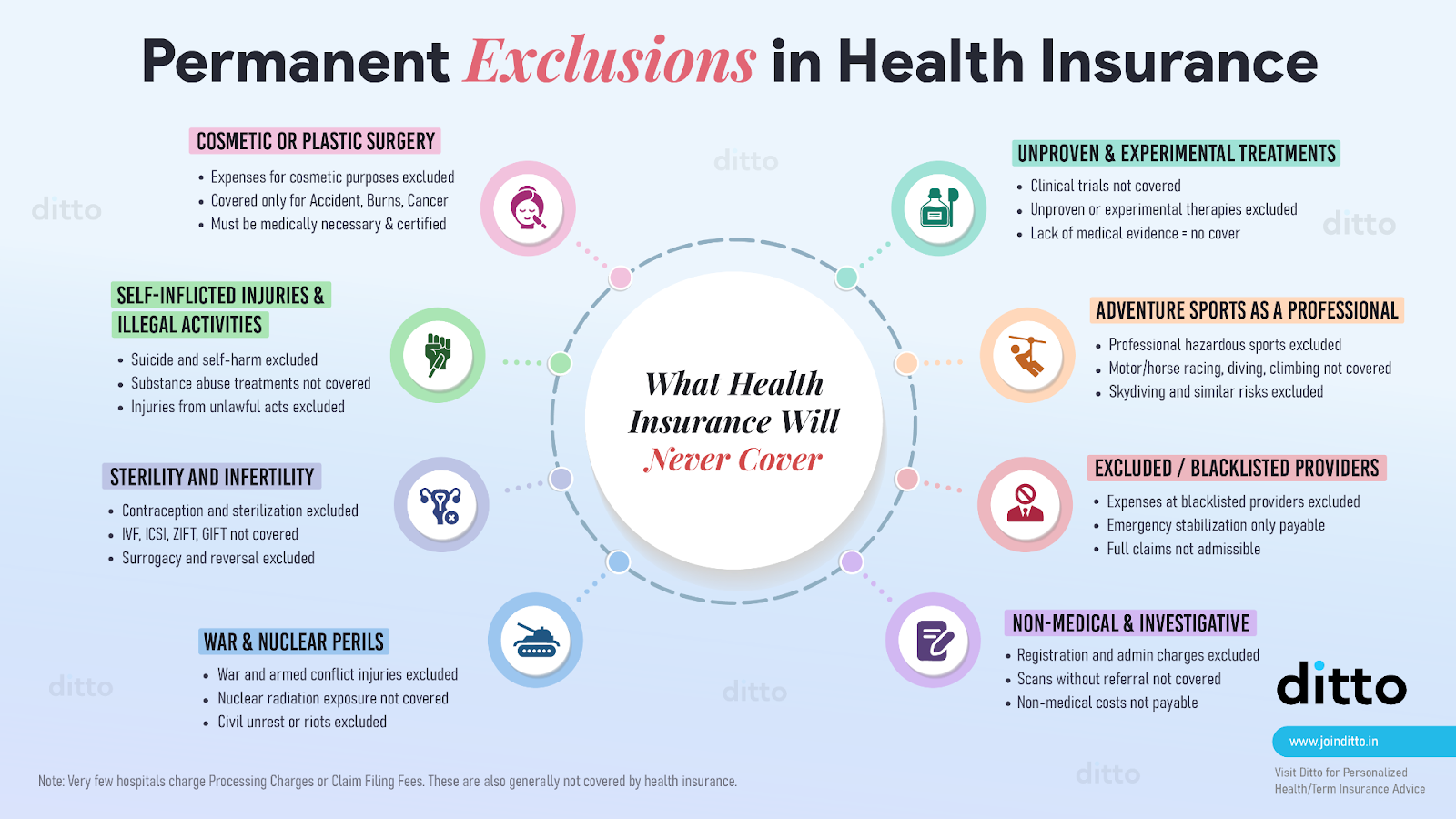

What’s Not Covered (Exclusions)

There are certain treatments, conditions, or situations that a health insurance policy for students does not cover, irrespective of its type.

Refer to this infographic to get a detailed understanding of the permanent exclusions in health insurance plans for students.

Types of Health Insurance Plans for Students

Choosing health insurance for students isn't a "one-size-fits-all" decision. A 12-year-old school student in Delhi has vastly different medical needs and legal requirements than a 24-year-old PhD candidate in London. To make the best choice, you must understand the four primary avenues of coverage.

Personal Health Insurance (Individual or Family Floater)

Who Needs it: Students in India and those planning for long-term health security.

Health insurance for students is most commonly accessed through a parent’s family floater policy in India. This is the most economical route because the premiums for a "child" dependent are significantly lower than those for an adult.

However, there is a catch: the exit age. Most insurers remove students from the family floater once they reach 25 or 26 years of age.

Note: If a student has been continuously covered under a family floater and migrates to an individual policy with the same insurer at the exit age (often 25 or 26), the waiting period already served is carried forward. This is commonly referred to as continuity benefit or waiting period credit.

Key Insights

University-Sponsored Health Insurance (Domestic and Abroad)

Who Needs it: Indian students enrolled in premier Indian institutes (IITs/IIMs) or universities in the USA, Canada, and Australia.

What Does it Mean for Students: University-sponsored health insurance offers basic, ready-made medical cover that meets institutional or visa requirements, both in India and abroad. It is convenient and often compulsory, but the coverage is usually limited by room rent caps, sub-limits, or course duration.

Students and parents should treat these plans as a minimum safety net, not a complete solution, and review whether additional personal health insurance is needed for stronger, long-term protection.

The Reality of College Health Insurance Plans: Take the case of IIT Bhubaneswar for the 2025–26 academic year. Students are covered for ₹2 lakh, which sounds reasonable for a young adult. However, the policy caps room rent at 1% of the sum insured (₹2,000 per day).

If a student is hospitalized in a private hospital where a room costs ₹5,000 per day, the issue goes beyond paying the ₹3,000 difference. Hospitals charge higher fees for doctors, surgeries, and nursing based on room type.

As a result, insurers apply a proportionate deduction. Since the room is 2.5 times more expensive than the limit, the insurer may pay only 40% of most hospital expenses, not just the room rent.

Even if the total bill is within the ₹2 lakh cover, a significant portion of the expenses can still fall on the student’s family.

This is the hidden risk of room rent caps. It explains why relying solely on university-provided health insurance plans for students can be a high-stakes gamble, especially during serious medical emergencies.

Abroad

International Student Health Insurance (Indian Insurers)

Who Needs it: Indian students going abroad who want to save money without compromising on visa-required coverage.

What Does it Mean for Students: International student health insurance from Indian insurers can significantly reduce costs while still meeting visa and university requirements. These plans work best for students who want flexible, short- to medium-term coverage with added protections, such as study interruption and sponsor protection.

However, they may have limits on home-country stays and coverage duration. Hence, students should align the policy term with their course length and travel plans.

Plans like HDFC ERGO Student Suraksha or Tata AIG Student Travel are specifically designed as health insurance for students crossing borders.

- The Cost Factor: These plans can often be cheaper than university-mandated plans in the US or the UK.

- Student-Specific Perks: They include "Study Interruption" cover (reimbursing fees if you fall ill and miss a semester) and "Sponsor Protection" (paying your fees if your parent/sponsor meets with a fatal accident).

Government-Provided Health Cover (Public Healthcare Abroad)

Who Needs it: Students in the UK, France, or Germany.

In some countries, health insurance for students is linked to the national social security system. This provides access to essential and low-cost medical care, but coverage is usually limited. Private hospitals, faster treatment, and certain services may also not be fully covered.

What Does it Mean for Students: Government healthcare works well for basics, but many students still need a private top-up plan to manage co-payments, long wait times, or uncovered treatments, especially for non-emergency or specialized care.

- UK (NHS): Students pay an "Immigration Health Surcharge" (IHS) during their visa application, which gives them access to the National Health Service.

- France (CPAM/PUMa): Registration is mandatory and free, but it only covers about 70% of costs. Most students buy a "Mutuelle" (top-up insurance) to cover the rest.

Pro-Tips for Maximizing Coverage

Best Health Insurance Plans for Students 2026

Let’s now see how the top plans stack up for students studying and residing in India. We review them one by one. We highlight what works well for students. We also flag fine print that can impact coverage.

We also explain how each insurer’s design affects real claims. This gives context beyond rankings. It helps families choose plans that support students today and adults tomorrow. This matters when selecting long-term health insurance plans for students.

HDFC Ergo Optima Secure

Care Supreme

Aditya Birla Activ One MAX

Niva Bupa ReAssure 2.0 Platinum+

SBI Super Health Platinum Infinite

Sample Premiums for Student Health Insurance

Note: Premiums are for a ₹15 lakh sum insured. Location is Delhi (110010). Prices include base premium only.

Below, we illustrate the indicative cost of an individual health insurance policy once a student exits a family floater plan.

Premium Comparison for Individual Health Plans

Note: The premiums shown above are based on a ₹15 lakh sum insured for a 26-year-old individual residing in Delhi.

For students aged 25 or 26 who need to transition to an individual policy, refer to our comprehensive guide on health insurance plans for those over 26. It covers the best options available and highlights common pitfalls to avoid.

Things to Remember When Buying Health Insurance Plans for Students

Buying health insurance plans for students is a strategic move to protect your academic journey from medical debt. You must look beyond the premium to find real value. Small mistakes in the fine print can also lead to massive out-of-pocket costs during a crisis.

Here are the critical factors you should verify before signing up:

- Check the "Exit Age" Early: If you are on a family plan, know when the insurer will ask you to leave. Most health insurance plans for students transition at age 25. Planning this move ensures you don't lose your waiting period credits.

Good to Know

- Prioritize Zero Room Rent Caps: Avoid plans that limit your room rent to 1% of the sum insured. This triggers "proportionate deduction," which can slash your entire claim payout.

- Disclose Every Detail: Never hide a past surgery or a chronic condition like asthma. Non-disclosure is the top reason for claim rejection in India.

Quick Note

- Avoid Co-payments and Disease-wise Sub-limits: A co-payment means you must pay a fixed percentage of every claim, regardless of the bill size. Disease-wise sub-limits cap how much the insurer will pay for specific conditions like asthma, hernia, cataract, etc., even if your overall sum insured is much higher.

- Evaluate Restoration Benefits: Restoration adds back the sum insured if it gets used up during a claim year. Some plans restore cover for the same illness only, while others restore for both same and different illnesses.

Example

- No-Claim Bonus (NCB) or Cumulative Bonus: This is a reward for claim-free years that increases your sum insured without a proportionate increase in premium. For every year you do not make a claim, insurers add a fixed percentage to your base sum insured, up to a defined cap.

Example

- Look for Consumables Cover: Hospital bills often include thousands of rupees for non-medical items like gloves, masks, and PPE. Standard health insurance plans for students might exclude these.

Tip

- Verify the Hospital Network: Ensure the insurer has cashless tie-ups near the university, hostel, or place of stay. Easy access to nearby network hospitals reduces stress during emergencies.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Rajan below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a free call now!

Ditto’s Take

There is no single “perfect” health insurance plan for students. The right choice depends on age, location, and how long the coverage needs to last. For most students in India, starting on a parent’s family floater early makes practical sense. It keeps premiums low and builds continuity that becomes valuable later.

As students move to higher studies or start living independently, it’s important to review the cover. University-sponsored group plans are useful, but are limited to the course duration. They often come with room rent caps and restricted benefits. This makes them risky as a standalone option for serious medical events.

For students studying abroad, the decision needs more care. University SHIP plans offer convenience and broad access, but they can be expensive. Indian student health insurance plans can be cost-effective, but they are useful only if the policy meets the destination country’s visa requirements and is accepted by local healthcare providers.

Employer or university health cover should be treated as a backup, not a replacement. A basic, portable health insurance plan for students offers long-term security that short-term group policies cannot.

In simple terms: secure a dependable base cover early and review it as academic and life stages change.

If you need help choosing the right health insurance plans for students, you can book a call with a Ditto advisor or reach us on WhatsApp.

Quick Note

Frequently Asked Questions

Customer Reviews

Last updated on: