If you’re a parent, you’ve already dealt with the late-night doctor visit, the surprise blood test, or the school injury call. Most of the time, it’s manageable, but every once in a while, a hospital bill lands that’s big enough to make you pause.

Child health insurance is simply a way to prepare for those bigger, less predictable expenses, without dipping into long-term savings or compromising on care.

You pay a yearly premium so that when a serious bill shows up, finances don’t become the deciding factor.

In this guide, we’ll walk you through how child health insurance really works in India, how plans are structured, how premiums change as your family grows, and what Ditto recommends in practice.

Think of this as a simple roadmap so you don’t have to decode insurance jargon on your own.

If at any point this feels confusing, you don’t have to figure it out alone. You can book a free call with a Ditto advisor to help you pick a plan that actually fits.

When people talk about “Health Insurance For Children” in India, they are usually referring to one of three structures:

How Child Health Plans Work in India

01

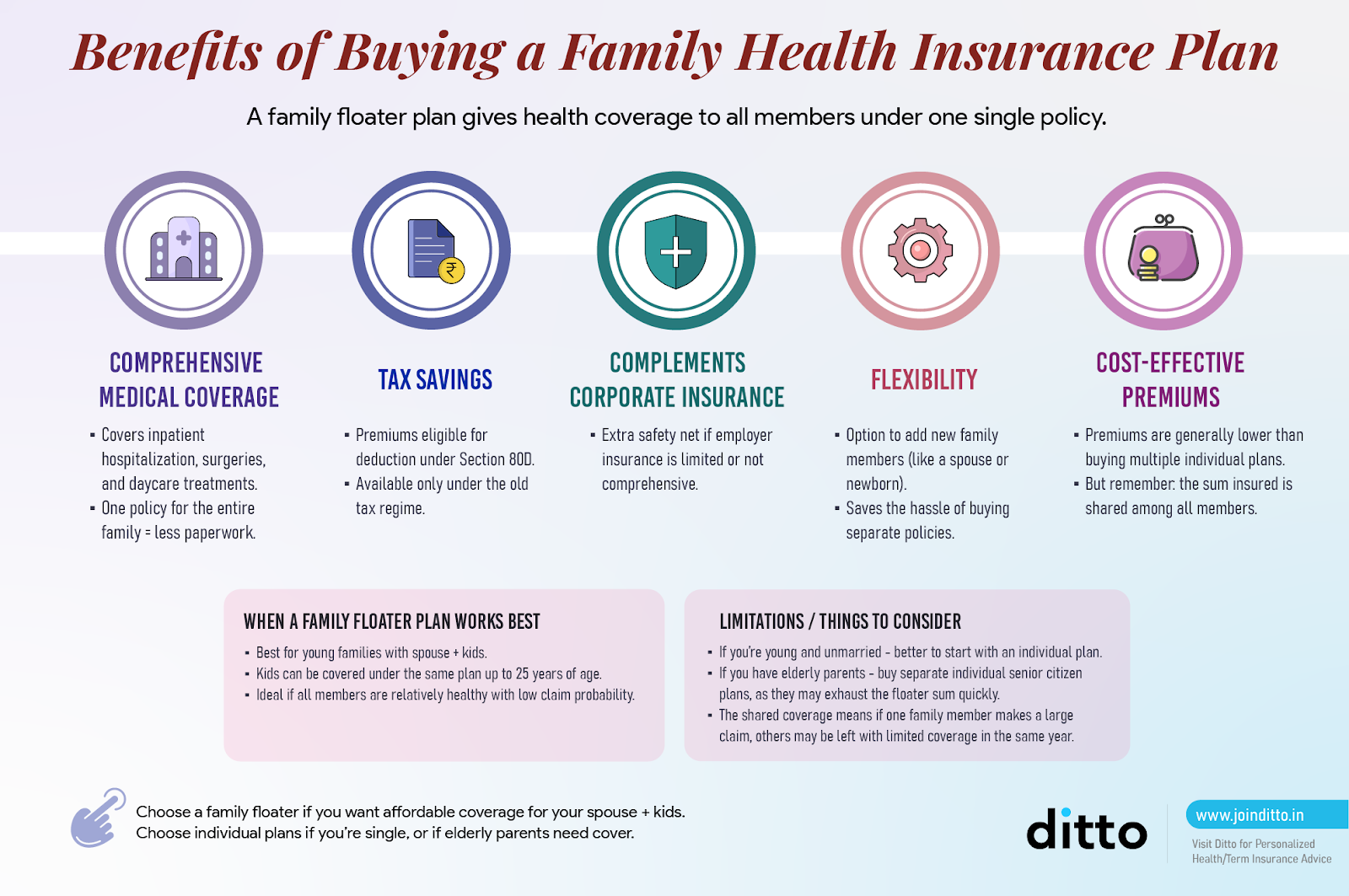

Family Floater

One shared sum insured for the whole family (for example, 2 adults + 1 or 2 children). It’s usually the most affordable way to start by adding the child as a dependent.

02

Individual Child Plan

The child gets an individual policy in their own name with parents as the proposer (applicant). This structure ensures the child’s coverage remains untouched even if parents make large claims. For example, Care’s Care Advantage plan allows individual policies for children starting from the age of 5 year

03

Multi-Individual Setup

Every family member has an individual policy within the same policy with the insurer. Think of it as “individual for everyone”, but easier to manage because all policies can be renewed together. Plans like HDFC ERGO Optima Secure and Aditya Birla Activ One MAX allow for multi-individual set-up.

Here’s what child health plans look like, and how coverage changes across different age groups.

Newborns (0-90 days)

Most retail health plans do not cover a baby from the day of birth. Typically, a child can be added only after 90 days of age. This “3-month rule” is mainly about risk: the first few weeks of life are medically fragile, and insurers want to avoid that risk.

A key exception is maternity with newborn cover. If the parent already has a plan with maternity benefits and the delivery is covered, insurers allow the newborn to be covered from day 1.

Regular-age children (91 days up to 18 years)

This is when most child-related claims happen like fevers, infections, minor surgeries, and injuries from sports or accidents. Health insurance here works much like it does for adults. Hospital bills are paid as per policy terms such as room rent limits, exclusions, and co-pays.

Most insurers allow children to be added to a family floater with an additional premium.

Adult children (usually 18 to 25 years)

Most policies allow children to remain a dependent till a certain age. This differs from plan to plan, but is usually 25 or 26. After that exit age, insurers offer migration to an individual policy, or their own floater, with continuity of benefits intact.

This transition is important to plan for, especially if your child has accumulated bonuses or served waiting periods.

Did You Know?

Under Care Ultimate, if you add your baby within 90 days of birth, the newborn can inherit the waiting periods you’ve already served as the primary insured - they don’t restart from zero.

How To Choose the Best Health Insurance Plan for a Child

Imagine you’re short-listing plans online. Every insurer claims to be the “best” for families, shows happy kids on the banner, and throws around phrases like “comprehensive coverage” and “cashless network”. How do you actually tell which policies are truly strong for children?

Coverage and terms (Features): room rent rules, co-pays, waiting periods (and reduction options), restoration, bonus, consumables, and key exclusions.

Insurer reliability (Insurer): claims and service track record based on IRDAI disclosures, complaint volume, business scale, and hospital network strength.

Cost for a benchmark profile (Premium): whether the plan is meaningfully priced for what it offers.

These are combined into a single Policy Rating, which we standardize into a simple Ditto Policy Score for easy comparison. You can find the full methodology here.

Using this framework, here are the Top 5 Health Insurance Policies for Children in India for 2026.

Talk to an expert today and find the right insurance for you.

Note: Our framework sometimes shows multiple strong products from the same insurer ranking in the top 10. To keep the comparison balanced and unbiased, we follow a “one insurer, one slot” rule in featured lists even though the data may place more than one policy from the same company among the top ranks.

Product-Wise Analysis of the Best Child Health Plans (2026)

Let’s now see how the top plans actually stack up, specifically for children and families. We’ll go one by one, calling out what the policy does well for kids, where the fine print can trip you up (child entry/exit age, maternity and newborn rules, room rent, co-pays), and how the insurer’s design affects real-world child claims.

This way, you’re not just seeing a rank or a number, but also the context behind it: why a plan deserves its spot for child coverage, who it suits best, and what to check before you buy for your family.

01

HDFC Ergo Optima Secure

Optima Secure focuses on what really matters, i.e., insurer reliability, a big hospital network, and core benefits that make a difference when you file a claim. That balance is why it sits at the top of our list.

HDFC Ergo

Optima Secure

4.6

Overall Rating

Premium Rating

3.0/5

Insurer Rating

5.0/5

Feature Rating

4.6/5

Customer Service Rating

5.0/5

Why Optima Secure stands out for children:

Optima Secure lets you insure kids from 91 days of age, and dependent children can stay on the family plan up to 26 years, after which they can be migrated to their own policy with continuity of benefits.

HDFC ERGO reports a 96.71% average claim settlement ratio (FY 2022-25), just 9.28 complaints per 10,000 claims, and a huge 13,000+ hospital network.

Key highlights of HDFC ERGO Optima Secure:

2X cover from day one (Secure Benefit).

Cover doubles again in 2 years, with a bonus given regardless of claims (Plus Benefit).

Consumables covered (gloves, masks, syringes, etc., under Protect Benefit).

Home healthcare, daycare, organ donation, and AYUSH treatments are included.

Unique riders for waiting period reduction for existing diseases, unlimited restoration, OPD coverage (Optima Wellbeing), maternity, and unlimited coverage once or twice during the policy's lifetime.

Things to keep in mind about HDFC ERGO Optima Secure

Premiums are higher than most peers, although you could argue that you’re paying for reliability and bundled extras.

02

Care Supreme

Care Supreme is one of Care Health’s flagship retail plans. As the second-largest standalone health insurer in India, Care Health brings both breadth of benefits and compelling pricing advantages to the table.

Care

Supreme

4.5

Overall Rating

Premium Rating

5.0/5

Insurer Rating

4.2/5

Feature Rating

4.5/5

Customer Service Rating

3.0/5

Why Care Supreme stands out for children:

Care Supreme covers children from 90 days up to 25 years. On the insurer side, Care Health is solid, though not spotless. It has 93.13% average CSR (FY 2022-25) and 42 complaints per 10,000 claims.

It lines up well for families who want unlimited recharge and strong bonuses while keeping premiums in check. Pricing is usually more affordable than HDFC ERGO’s Optima Secure, which makes it appealing for families, balancing cost with robust coverage.

Key highlights of Care Supreme

Unlimited Automatic Recharge for related & unrelated illnesses.

Cumulative Bonus up to 100% (option to extend by 500% or unlimited accumulation through add-ons).

Claim Shield add-on covering consumables. It comes in two variants, the regular and plus, which provide an extended scope for coverage.

Wellness discounts: earn up to 30% off renewals through fitness-linked benefits.

Unique add-ons for comprehensive waiting period reduction for existing diseases, GYM Memberships, OPD Cover, Unlimited Coverage once, and Air Ambulance.

Things to keep in mind about Care Supreme

Servicing can be uneven, and complaint volumes are higher than those of peers.

03

Aditya Birla Activ One MAX

Activ One MAX is built for younger, health-focused families who want rich benefits at a sensible price. The plan leans into wellness without skimping on core protection, which is why it’s become one of Birla’s standout products.

Aditya Birla

Activ One MAX

4.5

Overall Rating

Premium Rating

5.0/5

Insurer Rating

4.5/5

Feature Rating

4.3/5

Customer Service Rating

5.0/5

Why Activ One MAX stands out for children:

Activ One MAX allows children on a floater or multi-individual basis from 91 days, up to 26 years as dependents, and even offers a stand-alone child policy from age 5 onwards with parent as the proposer. Aditya Birla Health is a relatively young insurer that’s made quick progress. It has 95.81% Average CSR (FY 2022-25) and 18.66 complaints per 10,000 claims.

Key highlights of Aditya Birla Activ One MAX

Unlimited restoration (usable for related & unrelated illnesses) available from the 2nd claim of the policy lifetime

Cumulative bonus of 100% p.a up to 500% given regardless of claims made (MAX up to 3cr)

HealthReturns® that reward fitness/healthy living with discounts on renewal premiums up to 100%

Intuitive add-ons for pre-existing disease waiting period reduction

Things to keep in mind about Aditya Birla Activ One MAX

Insurer is newer; servicing isn’t as squeaky-clean as HDFC ERGO/Bajaj (complaints are slightly higher)

Wellness-linked benefits pay off only if you thoroughly engage with the program. We’ll be honest, achieving a 100% discount may be challenging, but savings of 10-50% are achievable through regular fitness activities.

04

Niva Bupa ReAssure 2.0 Platinum+

ReAssure 2.0 Platinum+ is Niva Bupa’s feature-heavy flagship, designed for long-term cover and high utilization. For families with children, its age-flexible design and strong restoration and booster features can be very reassuring over the decades.

Niva Bupa

ReAssure 2.0 Platinum+

4.3

Overall Rating

Premium Rating

5.0/5

Insurer Rating

4.2/5

Feature Rating

4.2/5

Customer Service Rating

3.0/5

Why ReAssure 2.0 Platinum+ stands out for children

ReAssure 2.0 covers dependent children from 91 days till maximum entry age of 30 years, without any exit age. This gives you an option to keep your kids on the family plan as long as you want. After 31 years of age, they can also choose to migrate to an individual policy carrying forward the benefits accumulated. ReAssure+ and Booster+ benefits are powerful when you think about multiple child and parent claims over many years.

Key highlights of Niva Bupa ReAssure 2.0:

ReAssure+: unlimited restoration of cover, every claim up to SI.

Age-lock on premium until first claim.

Booster+: unused SI carried forward up to 5× (up to 10x in the Titanium+ variant).

Safeguard/Safeguard+: covers non-payables + inflation-linked sum insured hikes + No impact on Booster+ if claim in a policy year is up to INR 50,000-1,00,000

Things to keep in mind about Niva Bupa ReAssure 2.0:

Age-lock resets after a claim, and premiums can still be repriced by the insurer due to medical inflation and spikes in operational and claim costs. Post-sales servicing and claims experience is not as uniform as the very top players.

05

SBI Super Health Platinum Infinite

Super Health Platinum Infinite is SBI General’s all-out, high-feature health plan. For families with children, it’s more of a “go big” option: very strong cover, higher sums insured, and benefits designed for serious, complex claims.

SBI

Super Health Platinum Infinite

4.3

Overall Rating

Premium Rating

5.0/5

Insurer Rating

4.2/5

Feature Rating

4.2/5

Customer Service Rating

3.0/5

Why Super Health Platinum Infinite stands out for children:

The plan covers dependent children from 91 days up to 30 years, giving you plenty of time to keep them protected under one large floater before splitting them out. Extended coverage, like OPD cover, can be useful with frequent doctor visits for children.

Key highlights of SBI General Super Health Platinum Infinite:

Unlimited reinstatement; up to 200% SI per claim (ReInsure Benefit).

Health Multiplier: up to 3× cover for 37 listed serious illnesses.

Global cover for 16 conditions + air ambulance ₹10 lakh.

Wellness add-ons: The insurer provides Health Assistance (A.I. Personal Fitness coaching), a Dietitian and Nutrition E-consultation, along with an unlimited gym membership.

Renewal Discount: SBI General offers a renewal discount based on the number of steps walked by the insured members, up to 30%.

Things to keep in mind about Super Health Platinum Infinite

Global cover and Health Multiplier apply only to listed conditions. Premiums are quite expensive due to the over-indulgent nature of the policy and a higher base cover amount (min ₹50L)

Premium Comparison of the Best Child Health Plans

Profiles

HDFC ERGO Optima Secure

Care Supreme

Aditya Birla Activ One MAX

Niva Bupa Reassure 2.0 Platinum +

(Family Floater, 2A): Ages (31, 32)

₹22,272

₹19,038

₹16,299

₹20,183

(Family Floater, 2A 1C): Ages (33, 34, 2)

₹26,687

₹23,976

₹21,478

₹26,343

(Family Floater, 2A 2C): Ages (35, 36, 5, 2)

₹31,430

₹31,434

₹30,259

₹31,142

Note:Premiums for a ₹15L S.I., Residing in Delhi - 110010, including necessary add-ons.

Inclusions and Exclusions of Child Health Insurance Plans

01

What's Included

Most health insurance plans typically cover essential medical expenses, such as inpatient hospitalization, pre- and post-hospitalization costs, day-care procedures, organ donor expenses, modern treatments like robotic surgery, AYUSH therapies, road ambulance charges, and even domiciliary treatments when required.

These inclusions ensure that a wide range of medically necessary treatments are financially protected under your policy.

02

What’s Excluded

Exclusions are fairly standard across insurers. Health plans generally do not cover investigation or evaluation-only admissions, rest or rehabilitation care.

They also do not include obesity or weight-control treatments, gender-change procedures, cosmetic surgeries, hazardous sports injuries, or substance abuse–related treatments. Maternity expenses are also excluded unless specifically covered under your policy.

It’s worth noting that coverage and exclusions may vary slightly across insurers and plans.

Common Mistakes in Children’s Health Insurance

Many parents pick very low coverage just to “have something,” which is quickly exhausted in a private hospital.

Others overlook co-pays or sub-limits and discover them during claims.

Under-reporting medical history, even unintentionally, can also create issues like claim rejections later.

Finally, relying only on employer insurance without a personal backup leaves children exposed if jobs or group policies change.

Even if your child seems healthy today, life is unpredictable. Child health insurance is a simple way to protect your savings while making sure you don’t have to compromise on treatment when something bigger comes up.

Why Should You Buy Health Insurance for Children?

01

Higher Chances of Medical Expenses

A single fracture or minor surgery in a private hospital can cost more than most parents expect. Kids also pick up infections easily at school, daycare, and during seasonal changes. While many illnesses are routine, some need hospitalization and can quickly turn into meaningful bills that insurance can absorb.

02

More Risk Exposure

Urban pollution, crowded spaces, and changing food habits all add to a child’s overall health risk.

You can’t eliminate these factors, but you can make sure that if they lead to serious illness, the financial side is taken care of.

03

Poor Lifestyle Habits

High screen time, junk food, and less physical activity are now common. Over time, this can trigger health issues earlier in life, and having a good health plan means your child can access proper care without long debates about cost.

Why Talk To Ditto For Health Insurance

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 5,000+ happy customers

Backed by Zerodha

100% Free Consultation

You can book a FREE consultation with us. Slots are filling up quickly, so be sure to book a call now!

Ditto’s Take

There is no single “perfect” health insurance for children. For most families, it makes sense to start early with a solid family floater and add your child as soon as they’re eligible.

This keeps premiums reasonably low and builds a history that’s easy to continue later.

If you’re planning a baby, focus on how the plan handles maternity and newborns - the waiting period, what’s covered at birth, and when the baby gets full coverage.

As your child grows older, you can always rethink the structure and move them to an individual or multi-individual policy if it helps protect their coverage.

OPD, fancy riders, or very high covers are worth paying for only when you know you’ll actually use them. Employer cover is best seen as a bonus, not your only plan.

In simple terms: build a solid, reliable base cover you can keep for years, and then fine-tune it as life changes.

If you need any help in deciding which plan is the best for your child, please feel free to book a call with a Ditto advisor or talk to us over WhatsApp.

Quick Note

Ditto currently partners with HDFC ERGO, Care Health, Aditya Birla Health, and Niva Bupa. Some insurers on this list are non-partners, and we’ve still included them here because the rankings are unbiased and based entirely on published data, not on commercial relationships.

For a detailed explanation of our process, partnership policy, and disclaimers, please see our [Editorial Policy & Disclaimers] document.

Finally, this analysis is based on publicly available information and should not be treated as personalized advice. Always read the policy brochure carefully and consult a licensed advisor before purchase.

Frequently Asked Questions

What is a good age to start health insurance for my child?

Once your baby is past 90 days, most retail plans will allow you to add them as a dependent.

The earlier you start, the easier it is to clear waiting periods and maintain continuous cover.

Is a separate child policy better than a family floater?

For many families, a floater is the easiest and most affordable way to start. A separate child policy or multi-individual setup can make sense later if you want to protect their sum insured from frequent adult claims.

Do child health plans cover routine vaccinations and OPD visits?

Most base plans don’t cover routine vaccinations or normal OPD visits. Some insurers offer riders for these, but you should compare the extra premium with what you actually spend in a typical year.

Will I get tax benefits if I buy health insurance for my child?

Yes, premiums paid for your child’s health insurance qualify for tax deductions under Section 80D (Old Regime), within the usual family limits.

Is corporate health insurance applicable for newborns?

In many corporate health plans, you can add your newborn from day 1, which is helpful for immediate basic coverage. But the sum insured is often limited, and the cover only lasts as long as you stay in that job and the company keeps the same policy. So it’s better to treat corporate coverage as a useful bonus and still build a solid retail health plan for your child.

Customer Reviews

4.9

20915 reviews

Ditto is doing really great. Absolutely spam free- that's the best part. They don't talk to you like they are forced to sell the product. It's more like, helping us buy better. Advisor Nuha was very patient and answered all my questions with clarity. Thanks for the service

I

INDHUMATHI M

Loved the service! Maheta Nidhi Hitesh was incredibly helpful and knowledgeable. She guided me through the whole process and made everything super easy to understand. I really appreciated how patient she was with all my questions—there was no pressure at all, just clear and honest advice. Honestly, I'm very happy with my experience at Ditto so far. Highly recommend!

RK

Ragul Kumar

I had a great experience with Ditto while exploring health insurance options. The process was smooth and everything was explained clearly.

A special thanks to Swaroop SK for patiently answering all my questions and guiding me through the policy details without any pressure. The transparency and support made it much easier to understand and choose the right plan.

Really appreciate the assistance!

PS

Pulkit Singh

Had a great experience with Ditto Insurance. Ishita Sudrania was extremely helpful in guiding me through choosing the right term plan. There was no spamming or sales pressure, and all my questions were patiently answered. She also assisted me thoroughly with the entire application process. Highly recommend!

SS

Samil Shah

I had a great experience with Ditto while filing my health insurance claim. Their team guided me clearly through the entire process, helped with the required documents, and promptly answered all my queries. Their support made the claim process much smoother and less stressful. Highly appreciate their assistance.