Quick Overview

Health insurance is supposed to give peace of mind, yet most people feel lost the moment they see premium tables and rate charts. Why does the price jump at age 36 and then again at 41? Why isn’t the premium for a ₹10 lakh cover exactly double the premium for ₹5 lakh? These questions confuse even the smartest buyers.

All insurers are required to submit their premium structures and rate charts to IRDAI as part of the product approval process. These filings ensure transparency and create a reliable, standardized reference for customers evaluating price differences.

This article simplifies everything about using the United India health insurance premium chart, calculating your premium online, downloading the United India health insurance premium chart pdf, and interpreting the numbers clearly to make an informed decision.

How to Download the United India Health Insurance Premium Chart?

- Go to United India Health Insurance’s official website and click on the download links section on the main page.

- Navigate to the premium chart tab under the download center section.

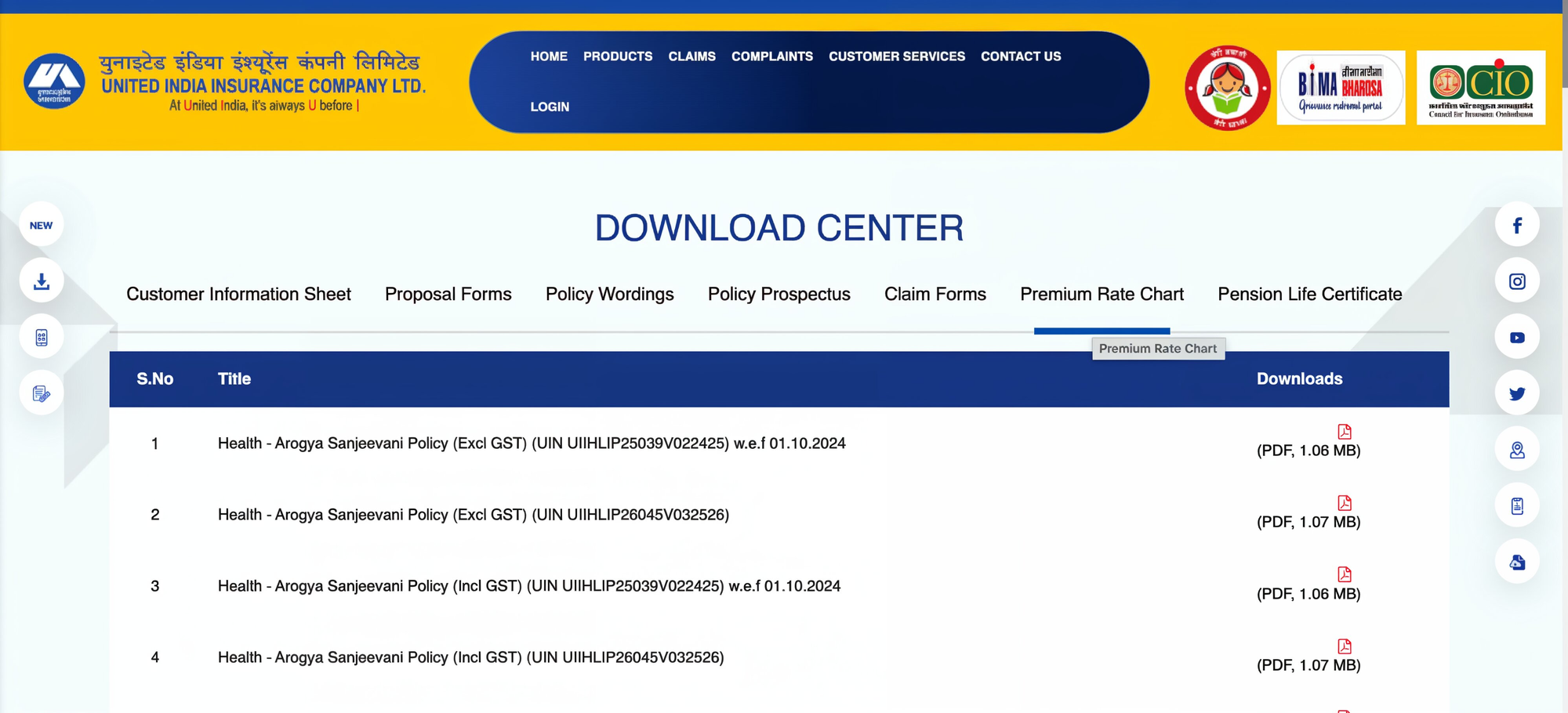

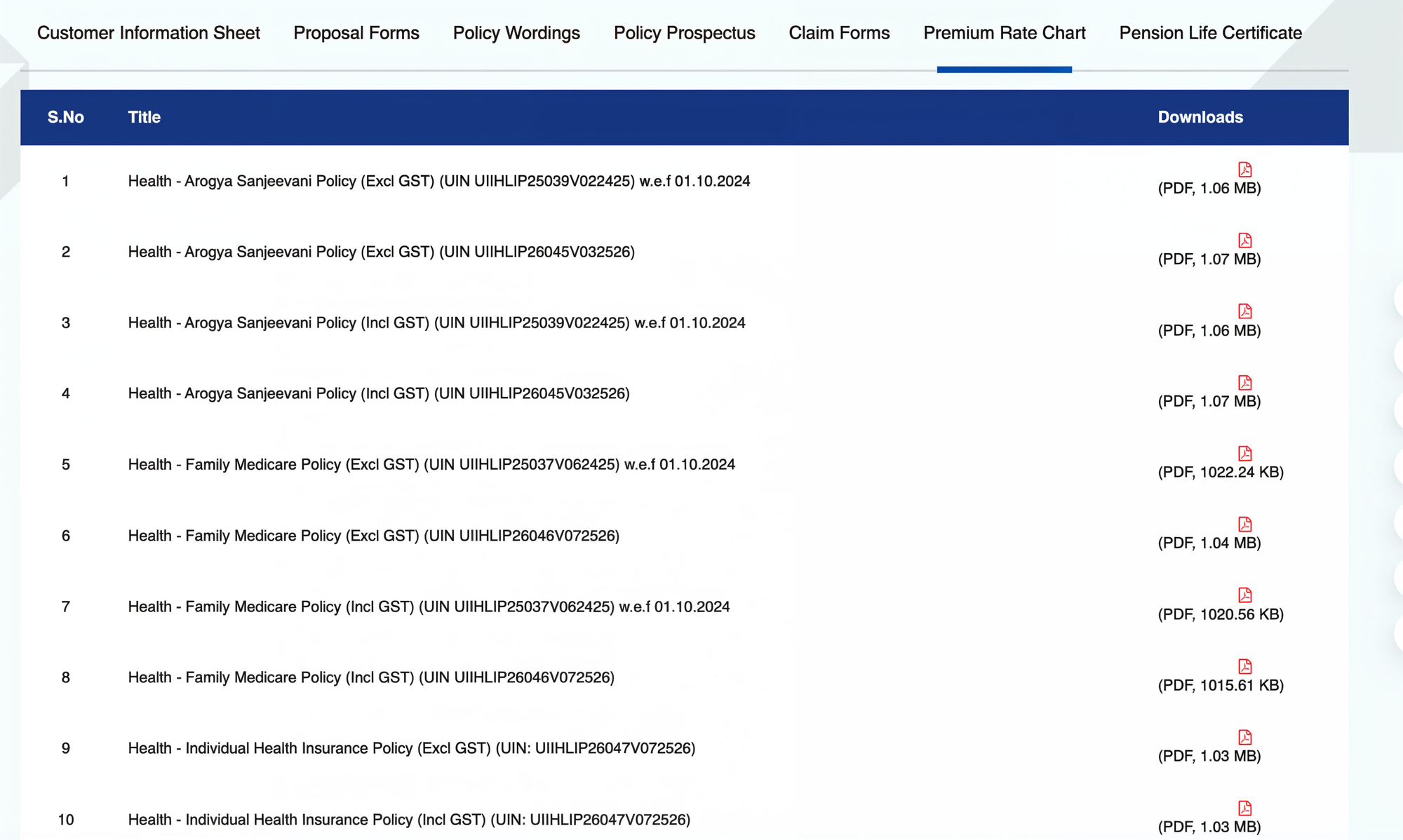

- A list of all of United India’s available plans will be displayed as follows:

- Click on the plan name to open its premium chart. You can download the PDF or view it online. For reference, here’s what a typical United India Health Insurance premium chart PDF looks like:

Note: Always download the premium chart from the insurer’s official website, as third-party information can be outdated or inaccurate.

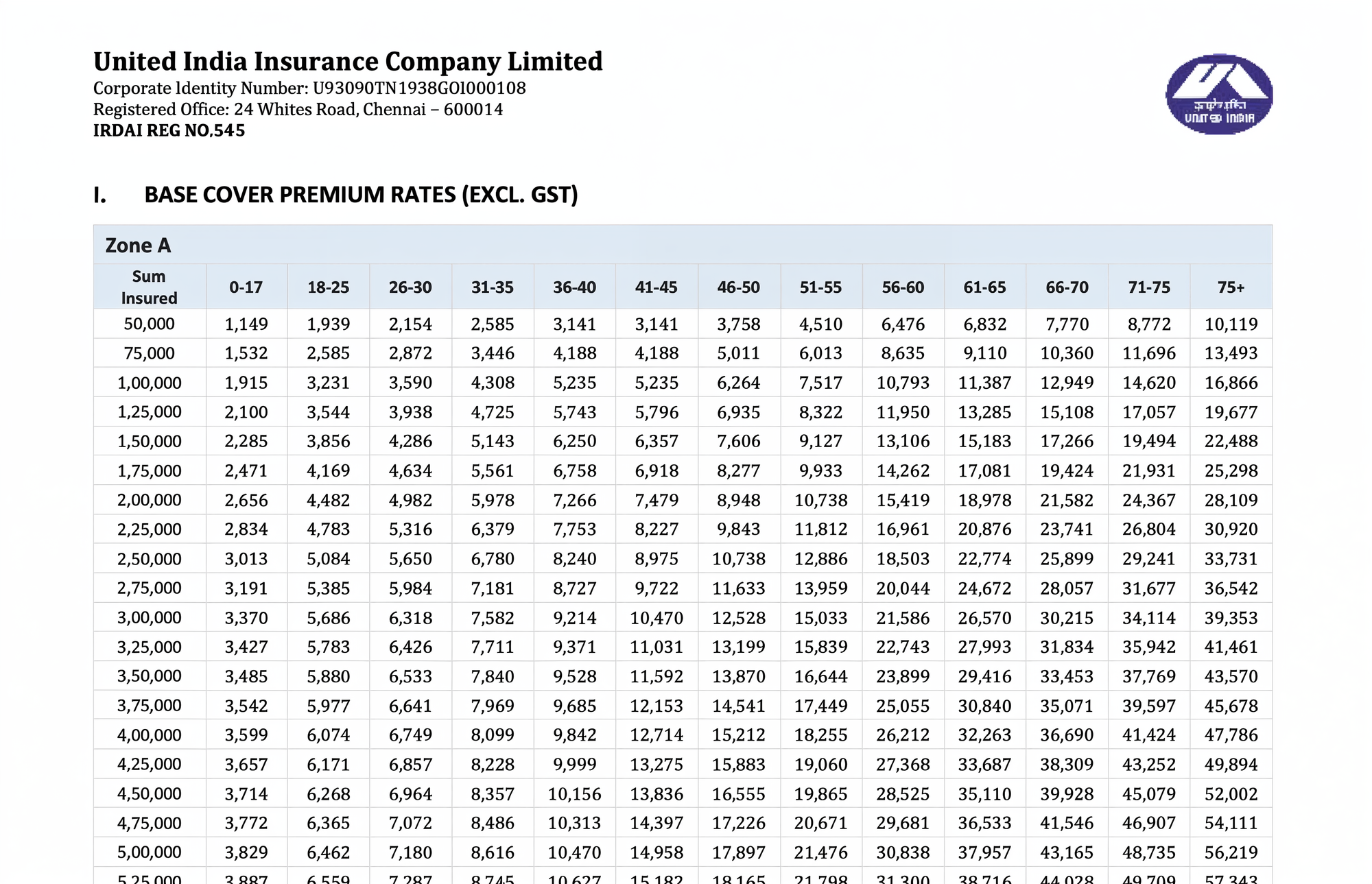

What the United India Health Insurance Premium Chart Shows

Age Group

Sum Insured

Floater vs Individual Premiums

Zone-Based Pricing

Note: Your premium may change if you move to a new city. Premiums can increase or decrease depending on your zone. Always keep your current or permanent address up to date with the insurer to ensure seamless service and claim processing.

How to Calculate United India Health Insurance Premiums Online?

- Go to https://uiic.co.in/ and choose your preferred language.

- Navigate to the customer services tab on the home page and choose the health premium calculator option.

- Enter the required details, such as plan type, family members, sum insured, pincode/city, age, and mobile/email (if asked).

- View premium results and available plan options.

Factors Affecting United India Health Insurance Premium

Age of Insured Members

Premiums increase with age because the likelihood of illness, hospitalization, and claims rises. Older age brackets always carry higher base rates.

Sum Insured Selected

Higher sum insured levels mean greater financial protection, but they also increase premiums since the insurer’s potential payout is higher.

Policy Type (Individual vs. Floater)

Individual plans charge a premium per person, while floater plans price coverage based on the eldest member’s age, making them cost-effective for young families.

Zonal Pricing

Premiums vary depending on whether you live in Zone A, B, or C. Metro and high-cost cities typically have higher premiums due to higher healthcare costs.

Medical History and Add-Ons

Pre-existing conditions or high-risk medical profiles may lead to underwriting loadings. Adding optional covers (consumables, bonus, restoration, etc) also increases the overall premium.

Popular United India Health Insurance Plans With Premium Charts

How Premium Differs by Plan Type

Premiums vary significantly across United India’s health plans because each product is structured differently in terms of coverage type, entry age, deductibles, and how the sum insured is shared.

Individual Sum Insured vs. Family Floater

Individual plans charge premiums per insured member, since each person has their own sum insured. Whereas choosing a family floater allows shared coverage for the entire family, making premiums more economical for younger families. Floater discounts may also apply.

Base Health Plans vs Super Top-Up Plans

Super top-up premiums depend on both the sum insured and the deductible. Higher deductibles mean lower premiums because the insurer pays only after total expenses exceed the deductible.

Age-Based Pricing

Every United India premium chart uses an age-bracketed structure. Each band has its own rate, making it easy to see how premiums step up as you enter a higher age bracket.

Zonal Pricing (Zones A/B/C)

In most plans, metro cities (Zone A) typically have higher premiums than Tier-2/3 cities (Zones B/C). Here is an illustration showing the zones for the Family Medicare policy.

For your reference, we’ve illustrated Family Health Medicare plan premiums below for a few common customer profiles to make comparisons easier.

Note: These premiums are based on a ₹15 lakh sum insured, for healthy profiles. Values are indicative and may vary after underwriting.

Why Choose Ditto for Your Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Here’s why customers like Abhinav love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation with us. Slots are filling up quickly, so be sure to book a call now or chat with us on WhatsApp!

Conclusion: Once you understand the United India health insurance premium chart, it becomes easier to see how age, sum insured, zone, and plan type impact your premium. Learning to read the United India health insurance premium chart PDF also makes comparing plans more straightforward. And if the process still feels confusing, we’re here to guide you.

Disclosure: United India Insurance is not a partner insurer of Ditto. Our assessment here is completely independent and based solely on publicly available data and the evaluation framework we use for all insurers. If you want to understand how Ditto reviews insurers across claims, complaints, business strength, and product suitability, read our methodology here. Please check the insurer’s official website for the latest available information.

Frequently Asked Questions

Last updated on: