LIC Jeevan Utsav is a non-linked, non-participating, whole life insurance plan designed to provide guaranteed lifetime income rather than market-linked growth. Policyholders can choose between a Regular Income Benefit, which pays 10% of the basic sum assured annually after the premium-paying term, and a Flexi Income Benefit, where payouts can be deferred and accumulated at a guaranteed interest rate of 5.5% per annum.

The plan also offers guaranteed additions of ₹40 per ₹1,000 of basic sum assured during the premium-paying term. While it offers income certainty and life cover, its long-term Internal Rate of Return (IRR) is generally modest (under 6%) and may struggle to outpace inflation. This LIC Jeevan Utsav review suits those who wish to understand the policy's features and drawbacks.

What if your retirement income could continue long after your salary stops? LIC Jeevan Utsav promises a stream of guaranteed payouts for life, but the real question is whether that certainty justifies the return you give up along the way.

In the next few minutes, this guide will break down LIC Jeevan Utsav plan details, including features, premiums, and suitability, to help you decide whether it deserves a place in your portfolio.

LIC Jeevan Utsav is a non-participating, non-linked, individual whole life savings insurance plan. It can be purchased offline through LIC agents, corporate agents, brokers, and insurance marketing firms, or online directly from LIC's official website.

LIC: Performance Metrics

Metrics (Average FY 2024-26)

LIC

Industry Average

Claim Settlement Ratio (CSR)

98.16%

99.00% (Mean)

Amount Settlement Ratio (ASR) (Average FY 2023-25)

Note: The above metrics reflect the overall performance of LIC and are not limited to any particular product. The data is sourced from IRDAI Annual Reports and LIC’s public disclosure.

Key Insights:

LIC continues to demonstrate strong claims-paying reliability, with claim settlement performance remaining broadly in line with the industry benchmark and above Ditto’s 97%+ mark.

The insurer performs particularly well in the value of claims settled, indicating that it handles both small and large payouts reasonably well.

LIC is the biggest life insurer in terms of business volume and remains significantly larger than the average insurer, reflecting its dominant position and extensive customer reach across India.

Customer grievance levels are substantially lower than the industry average, suggesting relatively smoother claims servicing and a more positive policyholder experience.

The company maintains a healthy solvency position above IRDAI regulatory requirements of 1.5x, providing an additional layer of financial strength and long-term stability.

LIC Jeevan Utsav Plan Details

Eligibility Criteria of LIC Jeevan Utsav Plan

Eligibility

Criteria

Premium Payment Term (PPT)

5 to 16 years

Premium Payment Mode

Yearly, half-yearly, quarterly, or monthly

Entry Age

30 days to 65 years (depends on PPT)

Sum Assured

₹5 lakh with no upper limit (depends on insurer underwriting)

Key Features of LIC Jeevan Utsav Plan

Income Benefit Options: Jeevan Utsav offers two income payout choices: Regular Income and Flexi Income. Once the income phase begins, the policy provides a guaranteed annual payout equal to 10% of the basic sum assured, helping to create a predictable long-term income stream.

Death Benefit: On the life assured's death, the nominee receives the higher of the basic sum assured or 7 times the annualized premium, along with applicable policy benefits. Importantly, the total death benefit will never be less than 105% of all premiums paid up to the date of death, ensuring a minimum protection floor for beneficiaries.

Maturity Benefit: Unlike traditional endowment plans, Jeevan Utsav does not focus on a lump-sum maturity payout. Instead, it is structured primarily as a guaranteed income plan, with the emphasis placed on regular cash flows and lifelong benefits.

Loan and Surrender Facilities: The policy offers flexibility through both loan and surrender options. A policy loan can be availed after completion of the first policy year, provided at least one full year's premium has been paid. Similarly, surrender is allowed after the first policy year if one full year's premium has been paid, although early exit may significantly affect overall returns.

CTA

Sample Premiums

Premium Payment Term

10 Years

30 Years

50 Years

5 Years

₹1,09,575

₹1,10,150

₹1,18,625

8 Years

₹72,600

₹72,600

₹72,600

12 Years

₹44,250

₹44,275

₹45,225

16 Years

₹29,900

₹30,025

₹33,475

Note: The premium figures shown are purely illustrative and are based on a basic sum assured of ₹5 lakh for different entry ages, excluding applicable taxes. Actual premiums may vary depending on age, policy term, underwriting factors, and insurer pricing. The illustration is derived from the official LIC New Jeevan Utsav Plan brochure.

What Optional Riders Are Available With LIC Jeevan Utsav?

The Accidental Death and Disability Benefit Rider offers an additional payout on accidental death and structured benefits in case of accidental disability, along with premium waiver benefits.

The Accident Benefit Rider provides a simpler lump-sum payout in the event of accidental death.

The New Term Assurance Rider provides additional life cover during the rider term, though a standalone term plan should still be compared for cost efficiency.

The Premium Waiver Benefit Rider is available only when the Life Assured is a minor. If the parent or guardian paying the premiums passes away during the rider term, all future base policy premiums are waived while the policy benefits continue uninterrupted.

Note: LIC restricts the total premium payable toward all life insurance riders to 30% of the base policy premium.

Regular Income vs. Flexi Income: Which Should You Choose?

01

Option I (Regular Income)

You receive 10% of the basic sum assured every year once the income phase begins. For example, a ₹10 lakh basic sum assured generates ₹1 lakh in annual income. This option suits those who want predictable cash flow, retirement income, and a simple, hands-off payout structure.

02

Option II (Flexi Income)

The same 10% income becomes payable each year, but you can defer it and let it accumulate within the policy. This option suits those who do not need immediate income and prefer greater flexibility for future withdrawals.

What Returns Can You Actually Expect?

The most important thing to understand is that the 10% annual income is not a 10% investment return. LIC pays 10% of the basic sum assured, not 10% of the premiums you invest.

LIC Jeevan Utsav is designed primarily for guaranteed lifelong income, not high investment returns.

Based on LIC's illustration, the IRR is typically around 5.4% to 5.7% per year. The exact return depends on how long the policyholder lives and receives income payouts.

Even with a very long lifespan, the return generally does not exceed about 5.75%. You can calculate the IRR from the benefit illustration numbers.

For comparison, a 10-year Government Security (G-Sec) currently offers yields of around 6.8%, which is higher. The trade-off is that Jeevan Utsav provides predictable lifetime income, capital protection, and no reinvestment risk on future payouts.

It may suit conservative investors who value income certainty over maximizing returns.

Note: Early exit can be costly. Although surrender is permitted after meeting minimum conditions, surrender values are relatively low in the initial years, which can significantly reduce overall returns. The plan, therefore, rewards patience and long-term commitment. Its value proposition improves substantially when held for decades rather than treated as a short- or medium-term investment.

Did You Know?

LIC introduced Jeevan Utsav Single Premium on January 6, 2026. It is a non-participating, non-linked, individual whole-life savings plan that requires just one premium payment and offers guaranteed additions for a defined period, making it a unique option for those seeking long-term certainty without recurring premium commitments. Jeevan Utsav Single Premium plan is the single premium version of Jeevan Utsav, but it should be treated as a separate product.

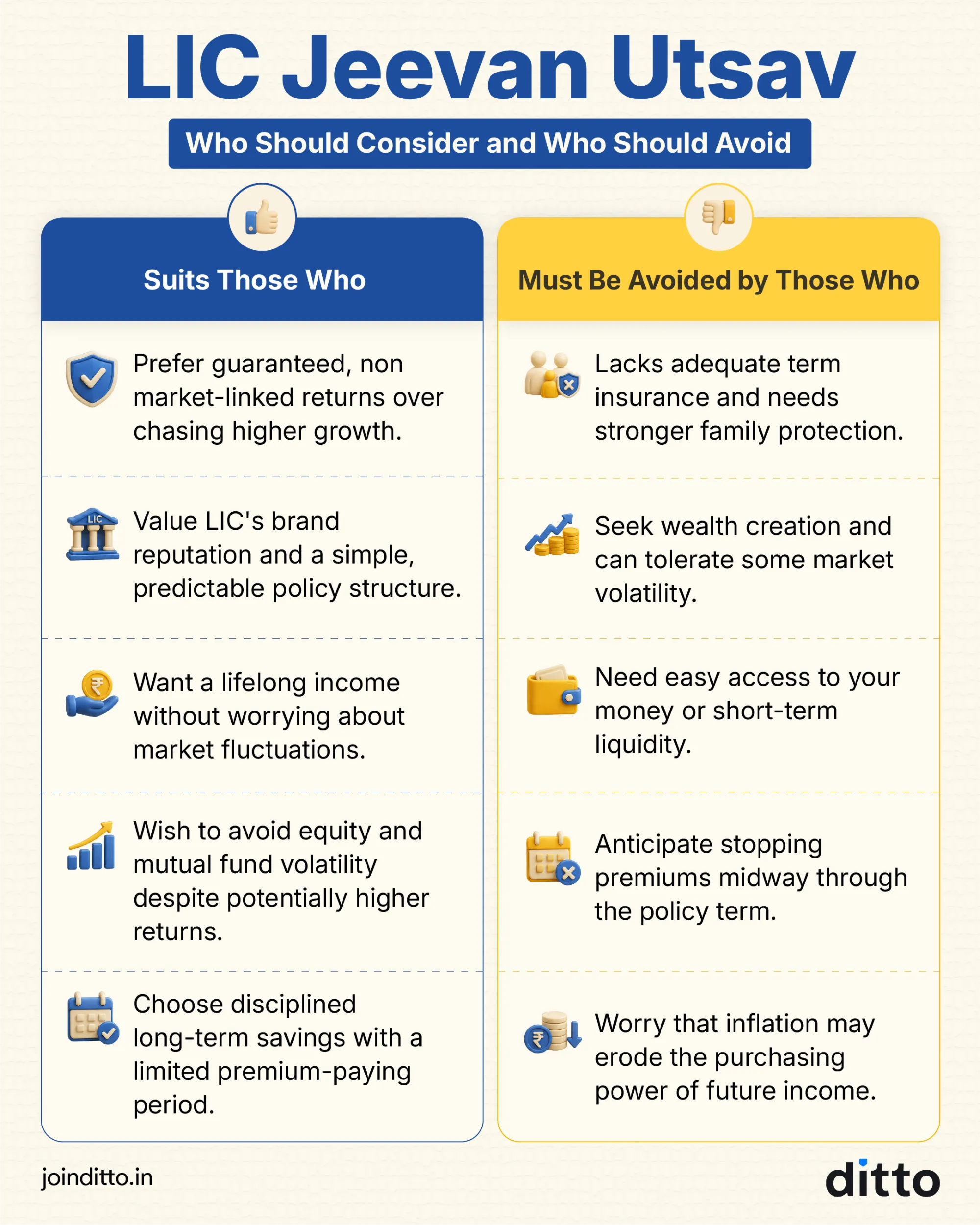

Who Should Buy LIC Jeevan Utsav and Who Should Avoid It?

The policy depends on the specific needs of an individual. Here’s an infographic to help you understand if you need the LIC Jeevan Utsav or not.

LIC Jeevan Utsav vs Term Insurance Plan and Investment

Point

LIC Jeevan Utsav

Term + Investment

Main Purpose

Guaranteed lifetime income

Protection + wealth creation

Life Cover

Usually modest (7x annual premium)

Can be much larger (20x to 30x annual income)

Return Type

Guaranteed

Market-linked / fixed, depending on the instrument

Flexibility

Low

High

Liquidity

Limited

Better, depending on the investment

Risk

Low market risk

Investment comes with market risk

Income

Built into the plan

You create income later from the corpus

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 24,000+ happy customers

LIC Jeevan Utsav works best when viewed as a guaranteed lifetime income and legacy planning product, not as a high-return investment or a substitute for adequate life insurance. For most individuals, life insurance primarily exists to protect income, repay loans, fund children's education, and support dependents. Once these responsibilities are substantially addressed, the need for large life cover often reduces.

While Jeevan Utsav offers lifelong protection and predictable income, many investors may find that a combination of adequate term insurance and disciplined investing in Fixed Deposits (FDs) or mutual funds provides greater flexibility and wealth-creation potential. Term insurance and separate investments work best if your priority is maximizing long-term financial outcomes.

If you are looking for a term plan from established insurers, we recommend the best term insurance plans that align with your long-term goals.

Frequently Asked Questions

What is the LIC Jeevan Utsav Plan 771, and is it a good plan?

LIC Jeevan Utsav (Plan 771) is a non-linked, non-participating whole life insurance plan that focuses on providing guaranteed lifetime income rather than market-linked growth. After completing the premium-paying term, the policy pays 10% of the basic sum assured every year for life. The plan accumulates guaranteed additions during the premium-paying period, which enhance the eventual death benefit. The plan may suit conservative investors who value certainty and predictable cash flows. However, it is not designed for aggressive wealth creation. Buyers should view it primarily as a guaranteed income and protection product rather than a high-return investment.

What is the difference between Regular Income and Flexi Income in Jeevan Utsav?

LIC Jeevan Utsav offers two payout choices once the income phase begins. Under the Regular Income Benefit, the policyholder receives a guaranteed annual payout equal to 10% of the basic sum assured. Under the Flexi Income Benefit, these payouts can be deferred and accumulated with LIC rather than withdrawn immediately. The accumulated amount earns a guaranteed interest rate of 5.5% per annum, compounded as per policy terms. Regular Income suits those who need immediate cash flow, while Flexi Income may appeal to those who want to postpone withdrawals and build a larger future corpus.

What are the eligibility criteria for LIC Jeevan Utsav?

The LIC Jeevan Utsav plan is available to individuals aged 30 days to 65 years, subject to the chosen PPT. Buyers can select a PPT ranging from 5 to 16 years. The minimum basic sum assured is ₹5 lakh, while the maximum depends on underwriting and LIC’s approval. Premiums can be paid annually, half-yearly, quarterly, or monthly. Since entry age limits vary across PPT options, it is important to check the official brochure before purchasing. The policy is designed to accommodate both younger savers and individuals planning for retirement income.

How much is the premium for LIC Jeevan Utsav for a ₹5 lakh basic sum assured?

The premium depends on your age and the PPT you choose. For example, according to LIC’s official illustration, a 30-year-old choosing a 5-year PPT may pay around ₹1.1 lakh annually, whereas a 16-year PPT can substantially reduce the annual premium. Older applicants generally pay slightly higher premiums for the same basic sum assured. These figures are illustrative and exclude applicable taxes and rider charges. Since premiums vary by age, PPT, and underwriting factors, buyers should use LIC’s official premium calculator or request a personalized quote before making a decision.

What guaranteed additions does LIC Jeevan Utsav offer?

LIC Jeevan Utsav provides guaranteed additions of ₹40 for every ₹1,000 of the basic sum assured throughout the premium-paying term. These additions accrue regardless of market performance and are added to the policy’s death benefit. For example, a ₹10 lakh basic sum assured earns ₹40,000 of guaranteed additions every year during the PPT. While these additions enhance the overall value of the policy, they stop once the premium-paying term ends. Buyers should remember that guaranteed additions improve certainty and death benefits, but do not transform the plan into a high-return investment product.

What happens if I surrender LIC Jeevan Utsav early?

Although LIC Jeevan Utsav allows surrender after meeting minimum conditions, exiting early can significantly affect returns. Surrender values during the initial years are relatively low because the policy is designed for long-term holding. The longer the policy remains active, the greater the value derived from lifetime income and accumulated benefits. Early surrender may result in receiving far less than the total premiums paid. This makes the plan unsuitable for investors who may need liquidity or are uncertain about their ability to maintain premium payments. You can also consider converting your plan to paid-up status rather than surrendering it.

Does LIC Jeevan Utsav provide a maturity benefit?

No. LIC Jeevan Utsav does not offer a traditional lump-sum maturity benefit. Instead, it is structured around guaranteed lifetime income and whole-life protection. Once the income phase begins, the policy continues paying annual income for as long as the policyholder survives. Upon death, the nominee receives the applicable death benefit. This differs from endowment or money-back policies, which usually provide a lump-sum maturity payout after a fixed term. Anyone looking specifically for a large maturity corpus at a predetermined age should carefully compare Jeevan Utsav with other LIC savings plans before purchasing.

What are the tax benefits and GST implications of whole life insurance plans in India?

Premiums can qualify for deductions under Section 123 (previously Section 80C), subject to the overall ₹1.5 lakh limit under the old tax regime. Policy proceeds, including guaranteed additions, are generally exempt under Section 11 (previously Section 10(10D)). For non-ULIP life insurance policies issued on or after April 1, 2023, an exemption is not available if the annual premium exceeds ₹5 lakh in any year, except for the death benefit. On the Goods and Services Tax (GST) front, individual life insurance policies, including whole life plans, became exempt from GST from September 22, 2025.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.